The water guide: Everything you need to know about water reporting and ESRS E3

A practical guide to understanding water disclosure, and the ESRS E3 reporting framework.

1. Introduction

Water management has become an important business resilience issue. Companies must demonstrate how they protect water resources, manage water security, and navigate physical risks like droughts and floods.

This article isn’t only for companies in scope of the CSRD. It’s for any organization that wants to report credibly on its environmental footprint: EU or non-EU, listed or private, big or small. I use European Sustainability Reporting Standard (ESRS) E3 as a clear and practical blueprint for water disclosure. If CSRD doesn’t apply to you (yet), you can still use this guide to structure your reporting and align with global expectations like corporate water stewardship.

ESRS E3 addresses how companies disclose their water-related impacts, risks, and opportunities, along with the strategies and metrics used to manage them. It is designed to align business reporting with, among others, the EU Water Framework Directive, the EU Drinking Water Directive, and the emerging EU Water Resilience Strategy.

In this article, you will learn:

✅ What water encompasses in a sustainability framework

✅ The main objectives of ESRS E3

✅ How ESRS E3 connects with other standards like Climate (E1), Pollution (E2), and Affected Communities (S3)

✅ The key components of ESRS E3 (E3-1 to E3-4), from policy to site-level metrics

✅ Acronyms and terms used in ESRS E3

By the end, you’ll gain a clear, structured understanding of reporting on water and ESRS E3.

Before we dive into the guide, here is an overview of all articles that are currently available.

Missing something? Please send me a message or place a comment.

You can find any of these articles by navigating to sustainabilitysimplified.eu/

and using the search button.

2. Short introduction to water and marine resources

First of all, it is important to know what water actually encompasses in a reporting context. In short: Water includes freshwater as well as brackish water, surface water, groundwater, seawater, produced water, and third-party water supplies.

Water and marine resources can be seen as the lifeblood of our planet. They sustain diverse ecosystems and play a vital role in supporting life. Water and marine resources consist of bodies of water such as rivers, lakes, oceans, and seas.

Water and marine resources are very important for several reasons. Beyond serving as a source of drinking water for humans, these resources play a crucial role in supporting diverse flora and fauna. Regarding climate change, the oceans act as a major carbon sink, absorbing carbon from the atmosphere. This absorption helps mitigate the impact of greenhouse gas emissions on the climate. Additionally, marine resources contribute significantly to global food security, as fisheries provide food for countless communities worldwide.

However, these invaluable resources face a multitude of challenges. Overfishing, pollution, climate change, and habitat destruction pose threats to the delicate balance of aquatic ecosystems. The threat to global water systems has officially crossed a tipping point. Scientists at the Stockholm Resilience Centre have confirmed that we have breached the planetary boundary for freshwater change (covering both “blue water” in rivers and lakes, and “green water” held in soil and vegetation). This means human activity has disrupted the global water cycle far beyond the safe operating space that maintains planetary stability.

To address water crises and prepare European infrastructure for a more volatile climate, the EU has updated its regulations to protect aquatic environments and support corporate water stewardship.

Because water risks pose such a direct, measurable hazard to both global health and business continuity, it is included as the third environmental standard (ESRS E3) in the CSRD.

Here follows a brief timeline of water frameworks by the European Union:

October 2000: The EU published the Water Framework Directive (2000/60/EC). This foundational legislation established a unified, basin-wide approach to achieving a “good status” for all clean surface waters and groundwaters across Europe.

December 2020: The EU adopted the revised Drinking Water Directive (2020/2184/EU). This updated framework introduced strict safety standards to protect human health from water contamination, addressing emerging chemical risks and improving access to clean water.

Recent developments: The EU launched initiatives under the EU Water Resilience Strategy, mainstreaming hydrological risks directly into corporate governance to protect businesses and ecosystems from structural water scarcity and intense flooding.

Read the EU Water Framework Directive here: Water Framework Directive - European Commission

Read more about the EU Water Resilience initiatives here: EU Water Resilience Strategy

3. Understanding the objective of ESRS E3

The objective of ESRS E3 is for companies to disclose information on water whenever it represents a material impact, risk, or opportunity. This ensures stakeholders understand how a company withdraws, consumes, discharges, and stores water, especially when operating in highly sensitive environments.

![[INSIGHT] 7 important water metrics you should understand](https://substackcdn.com/image/fetch/$s_!SZun!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F8131281a-09d5-4e49-a72f-87ab2abff2ae_1857x1731.png)

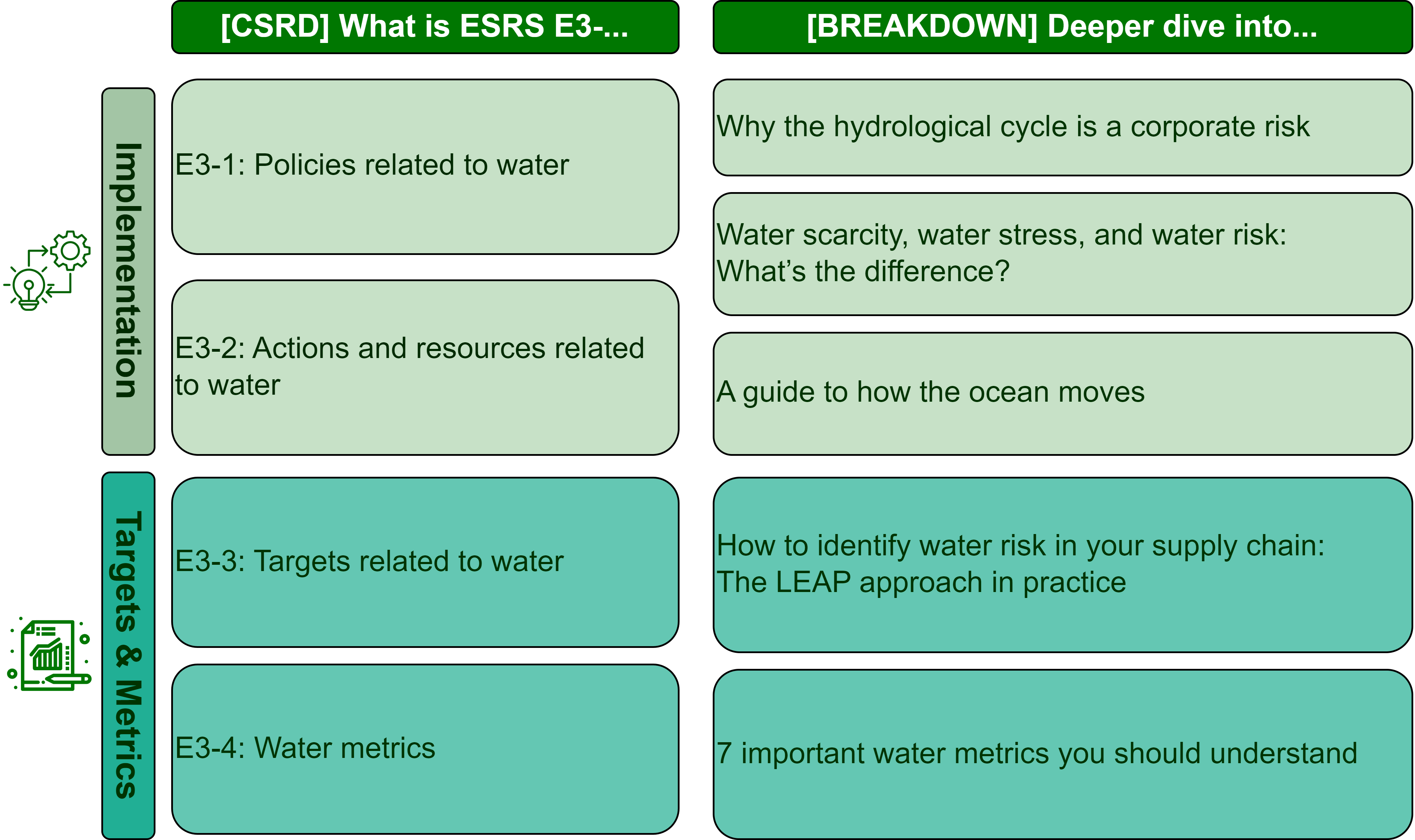

To help you gain a broader perspective beyond the regulatory disclosure requirements, I have published several deep-dive articles breaking down key hydrological concepts, risk assessments, and metric measurement frameworks.

Articles about understanding foundational water & ocean systems:

![[BREAKDOWN] A guide to how the ocean moves](https://substackcdn.com/image/fetch/$s_!60Cc!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F89ab7b74-35d4-448c-9030-20267d65e687_1857x1731.png)

Articles about water risk terminology & supply chain assessment:

![[BREAKDOWN] Water scarcity, water stress, and water risk: What’s the difference?](https://substackcdn.com/image/fetch/$s_!atiX!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fef616b57-0c24-413f-9b8a-5f78750eca27_1857x1731.png)

![[BREAKDOWN] How to identify water risk in your supply chain: The LEAP approach in practice](https://substackcdn.com/image/fetch/$s_!bjje!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F18e8a8aa-bc84-4e32-9322-b074b22a517d_1857x1731.png)

Articles about reporting & metrics:

ESRS E3 interacts closely with several other sustainability standards:

ESRS E1 Climate Change: E1 covers acute and chronic physical risks driven by climate change—such as droughts, changing precipitation patterns, and severe floods—which directly dictate water availability.

ESRS E2 Pollution: E2 handles the quality and chemical contaminants released into water bodies (including microplastics), whereas E3 focuses primarily on the volumetric flows of water use.

ESRS E4 Biodiversity: E4 looks at how aquatic ecosystem degradation impacts wildlife, while E3 tracks the physical resource extraction causing that ecological strain.

ESRS E5 Resource Use: E5 tracks material circularity, but any marine or water-based raw material inflows are explicitly cross-referenced with E3.

ESRS S3 Affected Communities: S3 addresses the social impact on local populations whose direct access to safe, clean, or abundant water might be compromised by corporate operations.

4. The different components of ESRS E3

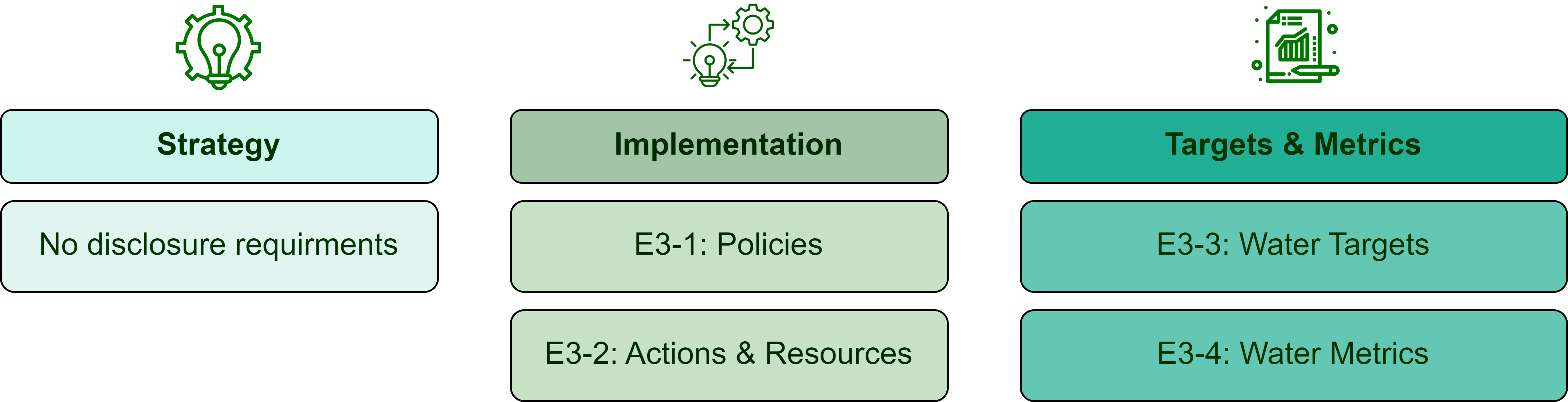

While ESRS E1 is structured around three pillars (Strategy, Implementation, and Targets/Metrics), ESRS E3 is structured into two pillars: Implementation (how you govern your water footprint) and Targets & Metrics (the actual data).

Because water is highly context-specific, ESRS E3 places a heavy emphasis on geographical disaggregation—meaning companies must report details at the local river basin or site level if they operate in water-stressed areas.

Read more below to explore each element in detail. I’ve also linked to my other articles below, where you can dive deeper into each specific topic, from ESRS E3-1 through ESRS E3-4, for a more comprehensive understanding.

E3-1, E3-2: Policies, actions, and resources

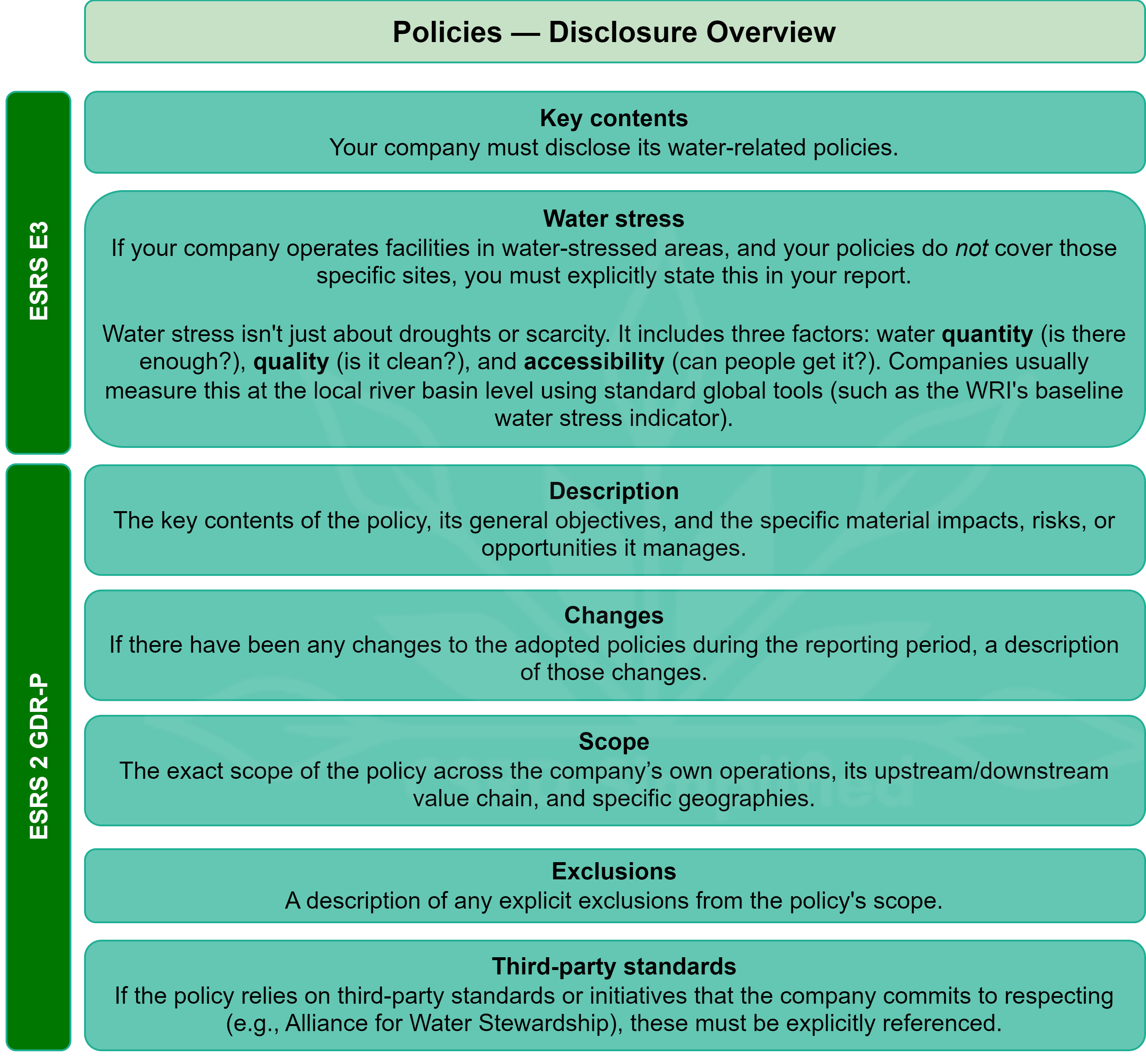

E3-1 (Policies): companies must disclose their explicit strategies for managing water resources. Crucially, if an organization owns operations or sites located in areas with high water stress that are not covered by a formal water policy, it must explicitly state this fact to investors.

Read more about ESRS E3-1 here:

![[CSRD] E3-1: Policies related to water](https://substackcdn.com/image/fetch/$s_!eiJ4!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fe0e04b77-db4d-4c5f-88f1-a6d244c4c7d7_600x600.png)

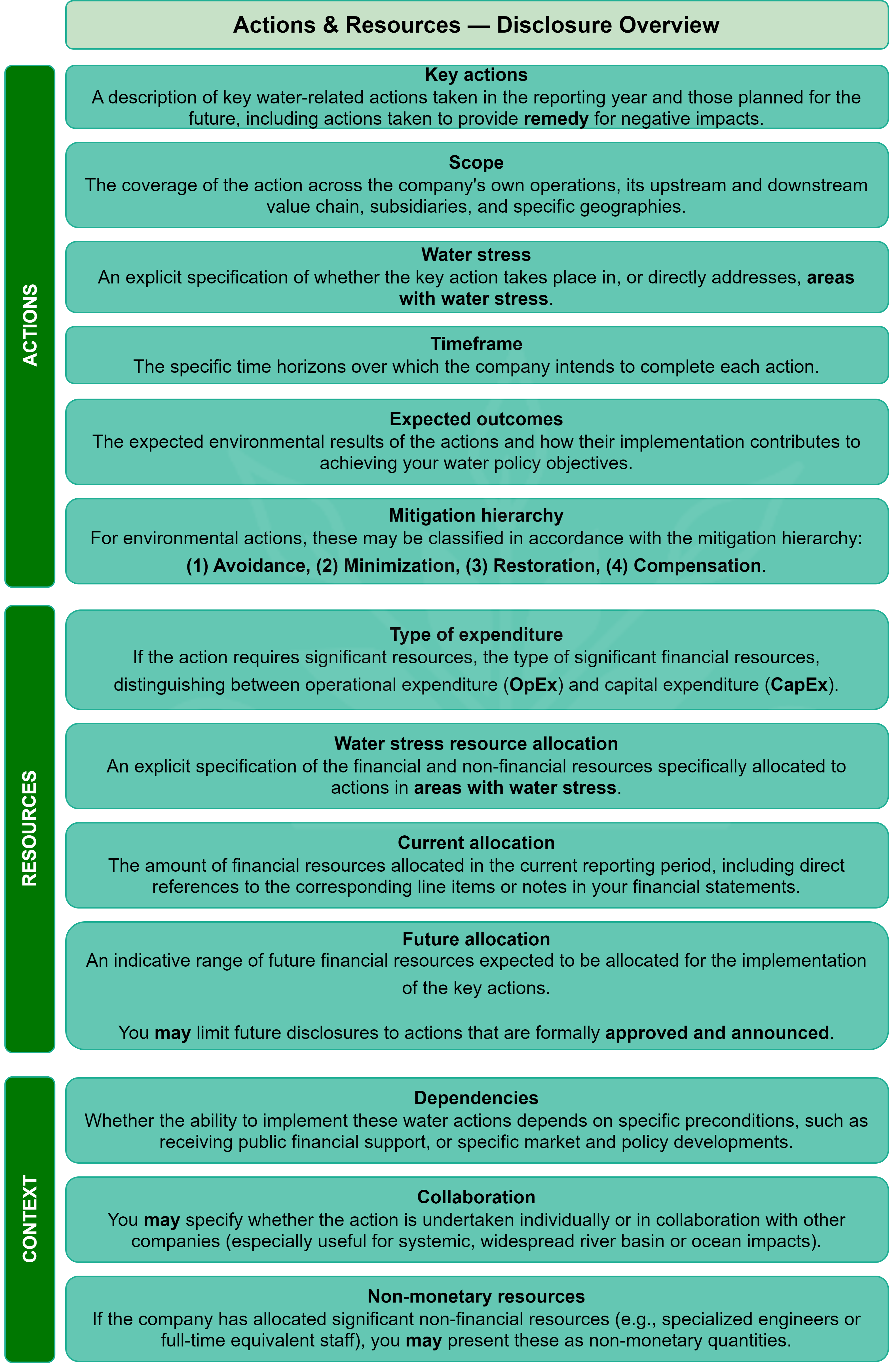

E3-2 (Actions and resources): requires reporting on the operational actions taken to optimize water efficiency (such as installing closed-loop recycling infrastructure) and detailing the financial resources (CapEx/OpEx) dedicated to executing these resilience projects.

Read more about ESRS E3-2 here:

E3-3: Targets related to water

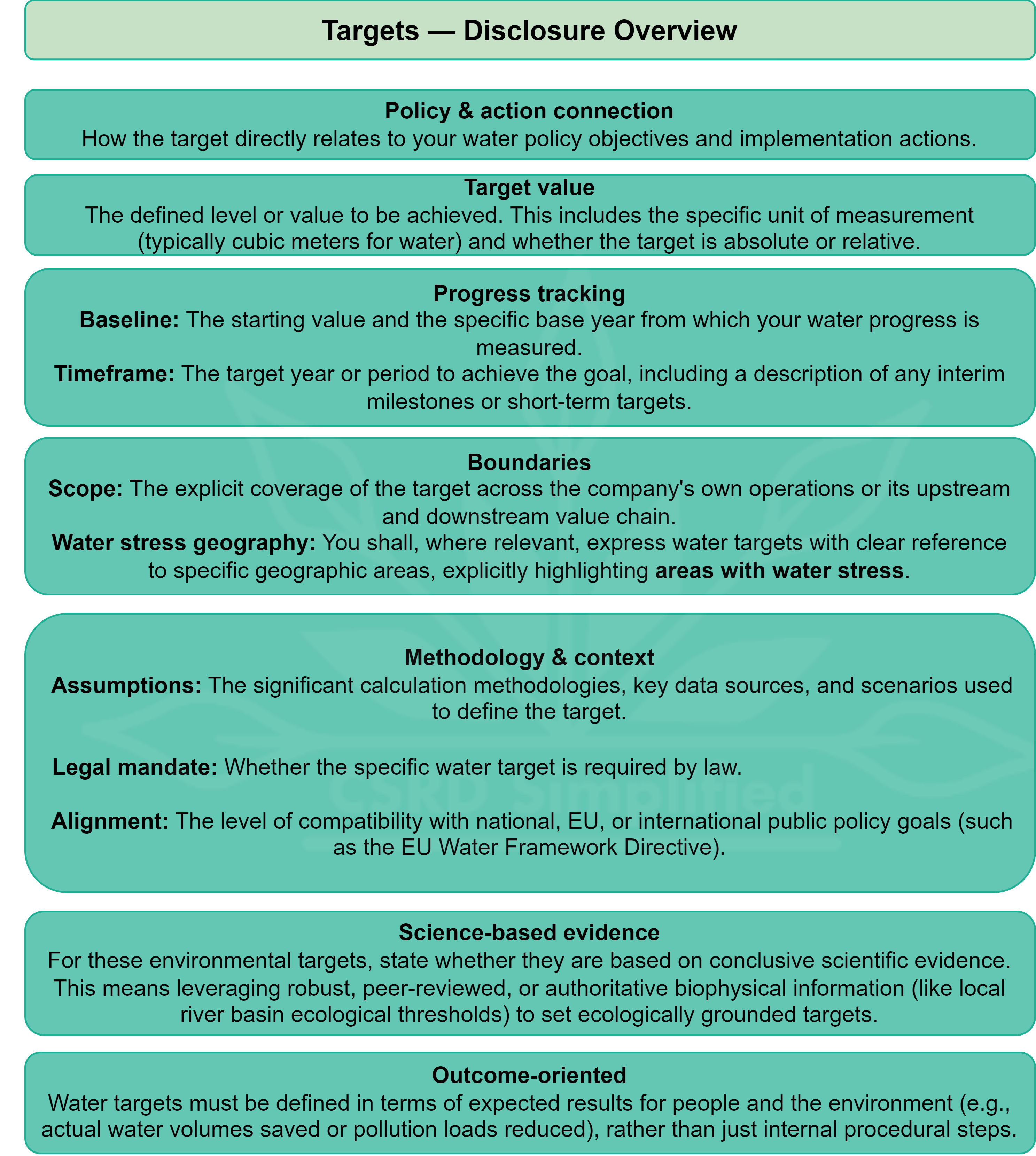

E3-3 focuses on the disclosure of specific, measurable goals for reducing water consumption or improving recycling rates. In line with cross-cutting rules, these targets should be tied to specific geographic basins or areas identified as water-stressed.

Read more about ESRS E3-3 here:

E3-4: Water metrics

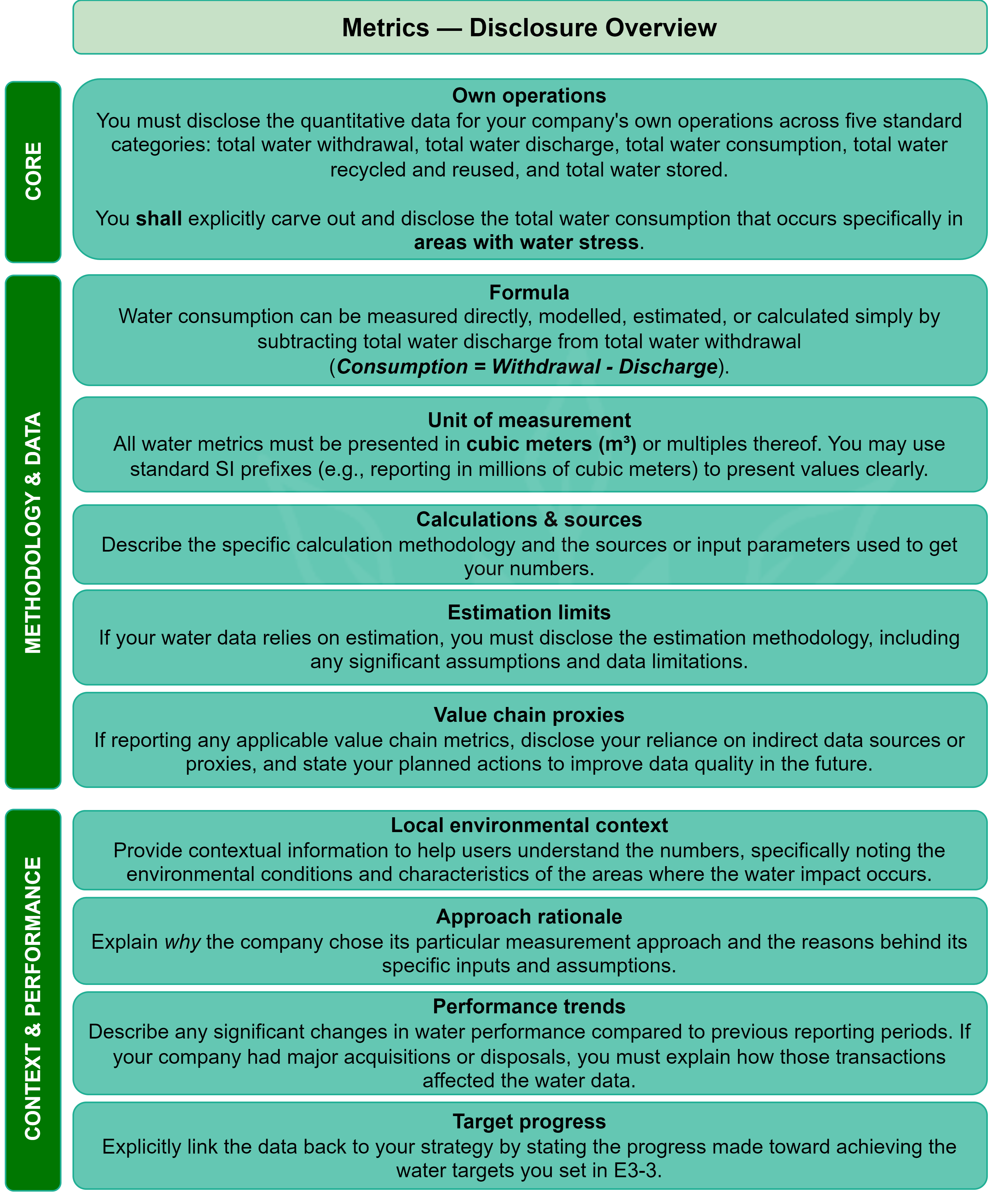

E3-4: this is the technical, data-heavy section of the standard. For their own operations, companies must disclose their data in cubic meters across different categories.

Read more about ESRS E3-4 here:

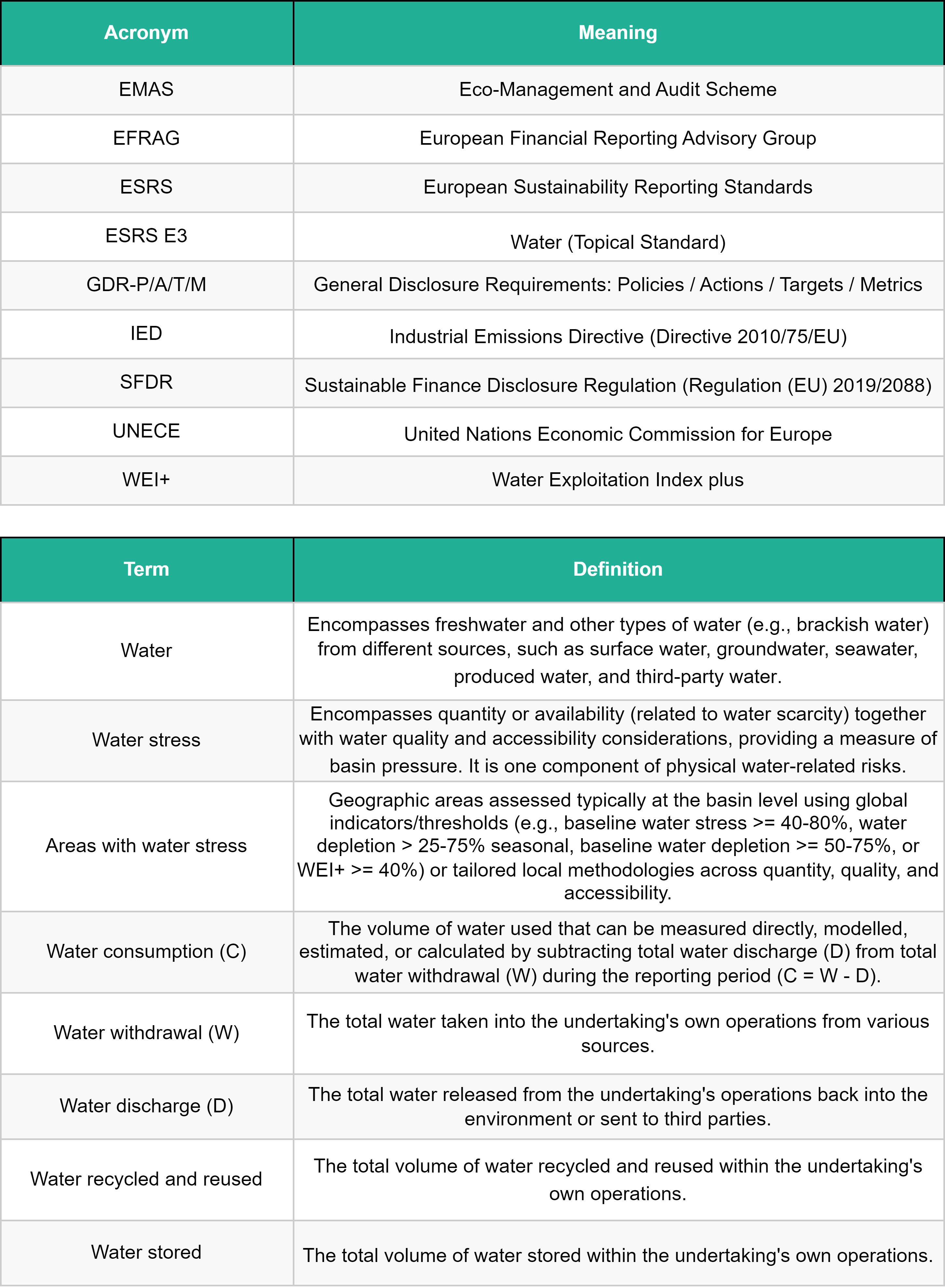

4. Acronyms and terms