[CSRD] E3-3: Targets related to water

CSRD Simplified: Disclosure Requirement E3-3: Targets related to water

1. Introduction

If policies (E3-1) set the rules and actions (E3-2) describe the work, then targets define the destination. ESRS E3-3 asks undertakings to disclose the specific, measurable goals they have set regarding water consumption, withdrawals, discharges, and water stored.

This disclosure provides the benchmark for accountability. Because water is often a localized resource, vague global ambitions are no longer sufficient. E3-3 requires you to translate high-level water stewardship commitments into trackable, location-specific numbers.

I will briefly explain the requirements for disclosing water-related targets.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are water targets?

Water targets are measurable, time-bound objectives designed to manage an undertaking’s material water impacts or risks.

According to the cross-cutting standards, targets regarding material impacts must be outcome-oriented. This means they must focus on the actual environmental result (e.g., cubic meters of water saved) rather than just an internal process (e.g., conduct three water audits).

Typical examples include:

Withdrawal: Reduce absolute freshwater withdrawal by 40% by 2030 against a 2022 baseline.

Discharge/Quality: Achieve 100% zero-liquid discharge at all manufacturing sites by 2028.

Efficiency: Increase the proportion of recycled/reused water in operations to 60% by 2026.

Water stress: Reduce water withdrawal by 30% across facilities located in areas with water stress by 2030.

The ESRSes define targets as follows:

“Measurable, outcome-oriented and time-bound goals that the undertaking aims to achieve in relation to material impacts, risks or opportunities. They may be set voluntarily by the undertaking or derive from legal requirements on the undertaking.”

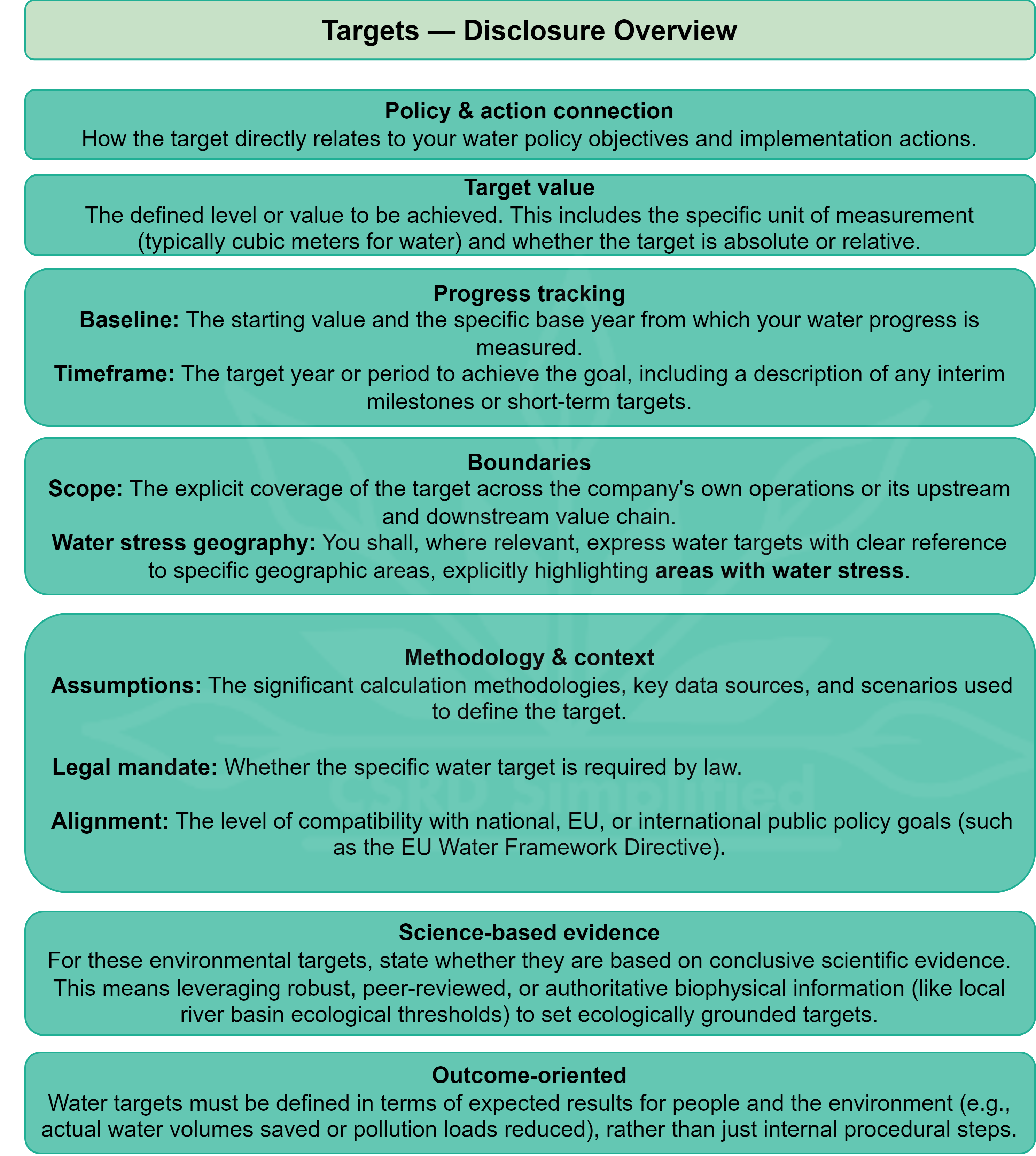

3. ESRS E3-3 at a glance

E3-3 requires that “the undertaking shall disclose its water-related targets in accordance with the provisions of ESRS 2 GDR-T“.

In addition, Application Requirement AR 3 for paragraph 14 explicitly specifies that:

“In line with the scope considerations set out in ESRS 2 GDR-T, paragraph 51(c), the undertaking shall, where relevant, express water-related targets with reference to specific geographic areas, such as areas with water stress.”

To comply with ESRS E3-3 and GDR-T, the disclosure must include:

If the undertaking has not set any measurable outcome-oriented targets for a material water topic, it shall disclose whether and, if so, how it nevertheless tracks the effectiveness of its policies and actions.

4. How E3-3 links to the rest of ESRS E3

Targets provide the necessary context to evaluate your raw data:

E3-1 (Policy): Establishes the commitment to reduce freshwater reliance in vulnerable regions.

E3-2 (Action): Details the investment in a closed-loop cooling system at a specific facility.

E3-3 (Target): Sets the measurable goal (e.g., reduce freshwater withdrawal at that facility by 50% by 2028).

E3-4 (Metric): Provides the actual cubic meters withdrawn, consumed, or discharged; without the target in E3-3, the metric in E3-4 is an isolated number, but the target tells users whether that number represents progress.

5. Bottom line

E3-3 demands precision and localized context. To report effectively:

Ditch the global average: Move away from generic aggregate targets. Targets should be expressed with reference to specific geographic areas, particularly river basins experiencing water stress.

Define the baseline clearly: Explicitly state your starting point (baseline year and value) so progress can be tracked over time.

Ground targets in scientific evidence: Where relevant, leverage conclusive scientific evidence and biophysical information regarding local ecological thresholds to set ecologically grounded, context-specific targets.