[CSRD] E3-2: Actions and resources related to water

CSRD Simplified: Disclosure Requirement E3-2: Actions and resources related to water

1. Introduction

If policies (E3-1) are the blueprint, actions and resources are the construction phase. ESRS E3-2 asks undertakings to describe the concrete steps they are taking—and the financial or human resources they are spending—to manage their material water impacts.

This disclosure helps you demonstrate that your water policy is more than a document by showing the operational projects and financial investments that support it.

I will briefly explain the requirements for disclosing water-related actions and resources.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are water actions?

Water actions are the specific operational initiatives, projects, or changes in practice designed to achieve the objectives of your water policy. Resources refer to the financial capital (OpEx and CapEx) or workforce personnel dedicated to implementing those actions.

Because water is mostly a local issue, these actions are usually highly specific to the facilities or supply chain nodes where water risks are most acute.

Typical examples include:

Infrastructure upgrades: Allocating €2M in CapEx to install closed-loop water recycling systems at a manufacturing plant.

Process changes: Transitioning to dry-cleaning methods for production lines to eliminate wastewater discharge.

Value chain initiatives: Investing in training programs for upstream agricultural suppliers to adopt drip irrigation techniques.

Efficiency and storage: Implementing water consumption reduction measures or upgrading storage infrastructure in water-scarce regions.

The ESRS defines actions as follows:

“Actions refer to:

i. actions and action plans (including transition plans) that are undertaken to ensure that the undertaking delivers against targets set and through which the undertaking seeks to address material impacts, risks and opportunities; and

ii. decisions to support these with financial, human or technological resources.

Actions can be individual actions, taken only by the undertaking, or collective actions, this is, collaborative efforts by a group of stakeholders - such as undertakings, governments, civil society, or communities - to address shared challenges or achieve common goals, particularly when those goals cannot be effectively achieved by any single actor working alone.”

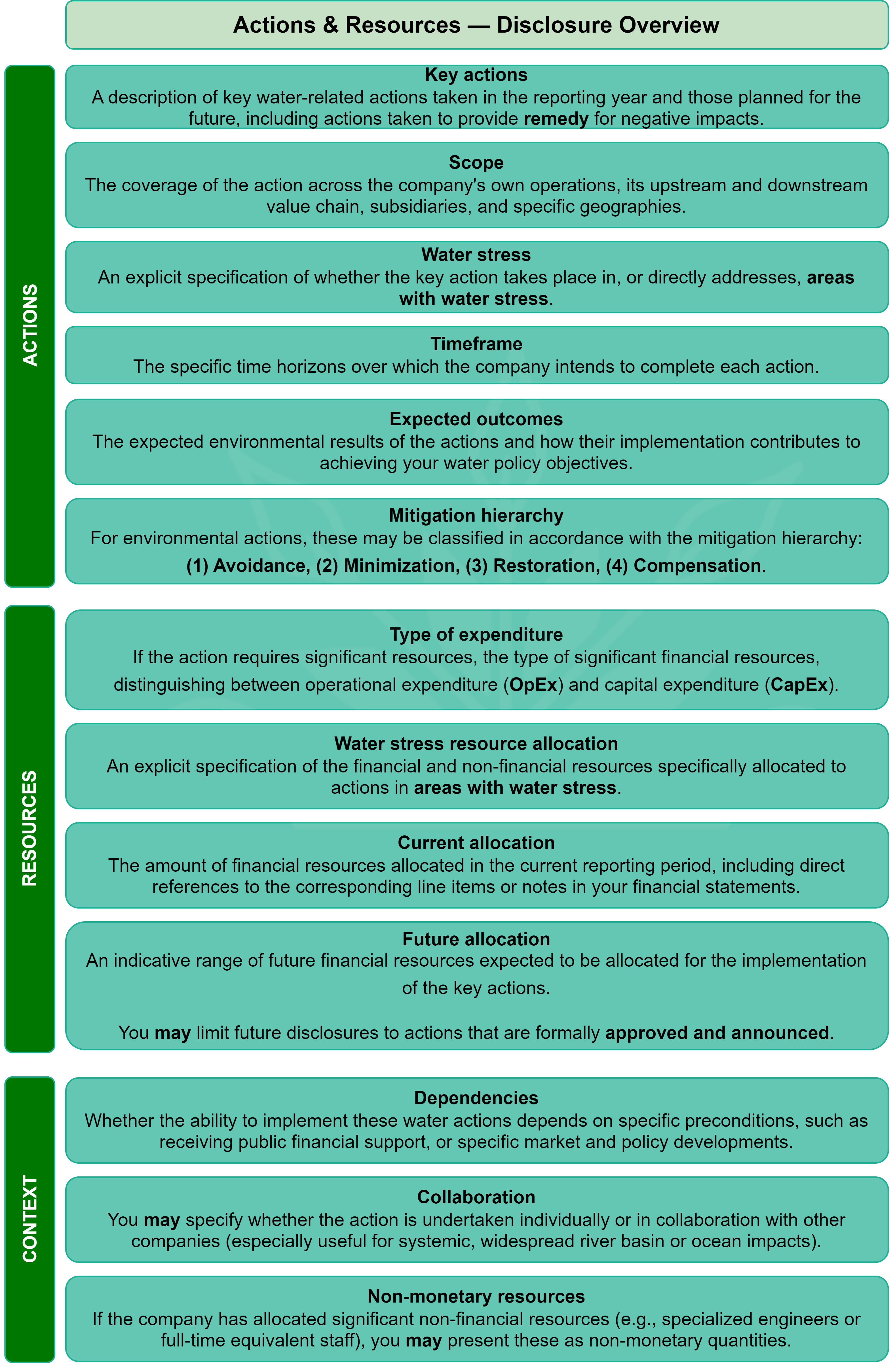

3. ESRS E3-2 at a glance

E3-2 requires that the company disclose its water-related actions and the resources allocated to their implementation using the framework provided by ESRS 2 GDR-A.

However, ESRS E3 adds a very specific, strict topical requirement:

You shall explicitly specify which key actions and resources are related to areas with water stress. You cannot simply report a global summary of water initiatives; you must isolate and highlight what you are doing in the most vulnerable geographic locations.

To comply with ESRS E3-2, the disclosure must include:

4. How E3-2 links to the rest of ESRS E3

E3-2 is the execution phase of your water strategy:

E3-1 (Policy): Establishes the commitment to prioritize water efficiency in vulnerable regions.

E3-2 (Action): The execution. Upgrading the cooling towers at the Spanish facility (an area with high water stress) at a cost of €500,000.

E3-3 (Target): Sets the goal to reduce that specific site’s water withdrawal by 25% by 2028.

E3-4 (Metric): Reports the actual cubic meters of water consumed, verifying whether the new cooling towers (E3-2) actually achieved the target (E3-3)

5. Bottom line

E3-2 is where companies must open their wallets to prove their commitments. To report effectively:

Map actions to stress: Generic, company-wide water initiatives are good, but the standard specifically hunts for localized action. You must map your initiatives and spending directly to the river basins experiencing water stress.

Follow the money: If your materiality assessment flags water as a highly material risk, but E3-2 shows zero CapEx or OpEx allocated to mitigate it, stakeholders and auditors will immediately notice the disconnect.

Context is everything: Saving 10,000 cubic meters of water in a region with abundant rainfall is a minor efficiency win. Saving the exact same amount in a drought-stricken region is a critical risk mitigation effort. E3-2 requires you to highlight that context.