[CSRD] E3-1: Policies related to water

CSRD Simplified: Disclosure Requirement E3-1 – Policies related to water

1. Introduction

While targets and metrics measure the output of a company’s environmental impact, policies provide the governance framework that dictates how those results are meassured. ESRS E3-1 asks companies to describe the official rules, principles, and commitments they have established to manage their impact on water.

This disclosure serves as the foundation of the Water standard. It connects your high-level sustainability governance (ESRS 2) to the tangible actions (E3-2) and targets (E3-3) aimed at reducing your water footprint and managing water-related risks.

I will briefly explain the requirements for companies to disclose their policies in relation to water consumption, withdrawals, discharges, and water stored.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What is a water policy?

A water policy is a framework that outlines how an undertaking manages its interactions with water systems. It addresses the sustainable sourcing, consumption, discharge, and storage of water across different sources (such as surface water, groundwater, seawater, produced water, and third-party water).

Context-specific considerations are incredibly important here, as water impacts are mostly local and tied to specific geographies.

Typical examples include:

Water efficiency commitments: Strategies to reduce absolute water consumption or improve water recycling rates in manufacturing processes.

Water stress management: Strict rules governing water withdrawal and discharge specifically tailored for operations located in highly water-stressed regions.

Value chain guidelines: Supplier criteria requiring minimum water efficiency standards or zero-liquid discharge for water-intensive raw materials (like cotton or agriculture).

Cross-standard interactions: While ESRS E3 focuses directly on water management (use, withdrawal, consumption, discharge, and storage), related impacts on marine ecosystems and resources interact with other topical standards such as ESRS E4 (Biodiversity and Ecosystems) and ESRS E5 (Resource Use and Circular Economy).

The ESRS 2 General Disclosures (GDR-P) provides the framing for this requirement. It states that the objective is to enable an understanding of the policies the company has in place to manage the prevention, mitigation, or remediation of material actual and potential negative impacts, as well as to manage material risks and pursue material opportunities or positive impacts. The ESRS defines a policy as follows:

“A set or framework of general objectives and management principles that the undertaking uses for decision-making. A policy implements the undertaking’s strategy or management decisions related to a material sustainability topic. Each policy is under the responsibility of defined person(s), specifies its perimeter of application, and includes one or more objectives (linked when applicable to measurable targets). A policy is validated and reviewed following the undertakings’ applicable governance rules. A policy is implemented through actions or action plans.”

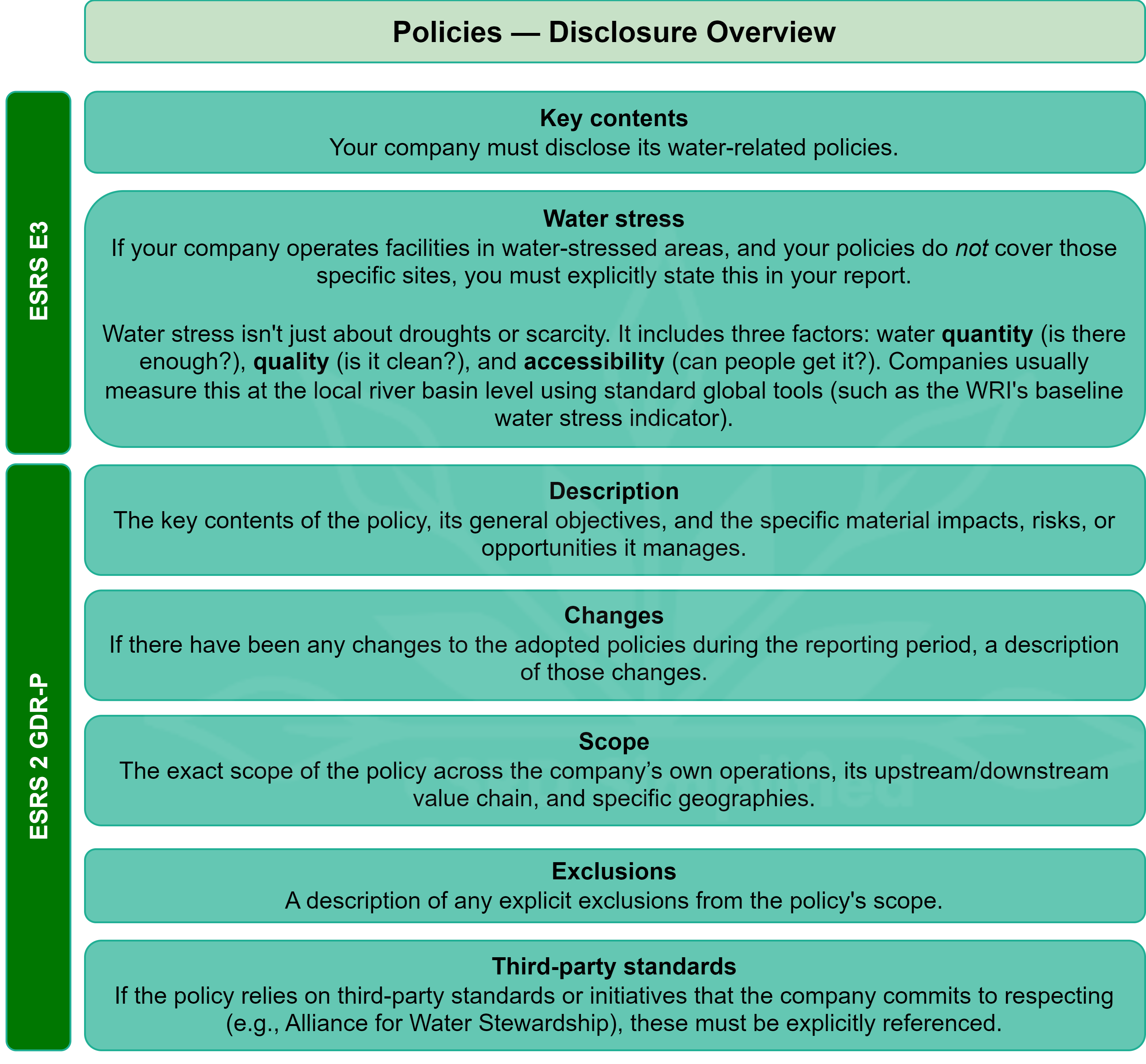

3. ESRS E3-1 at a glance

E3-1 specifically requires that “the undertaking shall disclose its water-related policies in accordance with the provisions of ESRS 2 GDR-P”.

To comply with ESRS E3-1, the disclosure must include:

If a company has not adopted policies regarding water despite it being a material topic, it must explicitly disclose this fact.

4. How E3-1 links to the rest of ESRS E3

E3-1 (policies) sets the rules and strategic direction for water management.

E3-2 (actions and resources) describes the key actions taken to implement those policies and the financial resources allocated to them.

E3-3 (targets) defines the measurable goals the company aims to achieve.

E3-4 (metrics) provides the data on for example actual water consumption, withdrawal, and discharges to track performance against the policy.

For example, a policy to minimize freshwater use in vulnerable regions (E3-1) would be implemented by investing in closed-loop cooling systems (E3-2), tracked against a target to reduce freshwater withdrawal by 30% by 2030 (E3-3), and reported via the absolute cubic meters of water consumed in areas with water stress (E3-4).

5. Bottom line

E3-1 is your opportunity to demonstrate that your organization’s approach to water is systematic and highly localized, rather than a generic global statement. To comply and communicate effectively:

Define the scope clearly: Be highly specific about geography. A water policy is most effective if it specifically addresses operations and supply chains located in areas with high water stress.

Address the full spectrum of water management: Ensure policies cover water quantity, quality, and accessibility, as well as consumption, withdrawal, and discharge.

Link to frameworks: Where relevant, show how your policies align with frameworks, such as the EU Water Framework Directive.

A robust water policy is the starting point for credible reporting on how an undertaking respects and preserves local aquatic environments.