[CSRD] E3-4: Water metrics

CSRD Simplified: Disclosure Requirement E3-4: Water metrics

1. Introduction

We have established the rules (E3-1), detailed the operational work and investments (E3-2), and set the specific goals (E3-3). Now, we arrive at the scorecard: ESRS E3-4.

This disclosure requires undertakings to report the hard quantitative data regarding their water performance. It moves the conversation from strategic ambitions to absolute volumes, allowing stakeholders to see exactly how much water you use, where you get it from, and where it goes.

I will briefly explain the requirements for disclosing water metrics.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are water metrics?

Water metrics are the standardized, quantitative measurements of how water flows through an organization’s operations.

To report correctly, you must understand the fundamental difference between key hydrological terms:

Withdrawal (W): The total amount of water you take in from any source (e.g., surface water, groundwater, municipal water supply).

Discharge (D): The total amount of water you put back out into the environment or to a third party (e.g., sending wastewater to a treatment plant or river).

Consumption (C): The water that is permanently removed from the local water cycle by your operations. It is what you take in minus what you return (e.g., water that evaporates in cooling towers or is incorporated into your final product).

Recycled/Reused water: The total volume of water recycled and reused within operations.

Water stored: The total volume of water stored.

![[INSIGHT] 7 important water metrics you should understand](https://substackcdn.com/image/fetch/$s_!SZun!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F8131281a-09d5-4e49-a72f-87ab2abff2ae_1857x1731.png)

The ESRSes define metrics as follows:

“Qualitative and quantitative indicators that the undertaking uses to measure and report on the effectiveness of the delivery of its sustainability-related policies and against its targets over time. Metrics also support the measurement of the undertaking’s results in respect of affected people, the environment and the undertaking.”

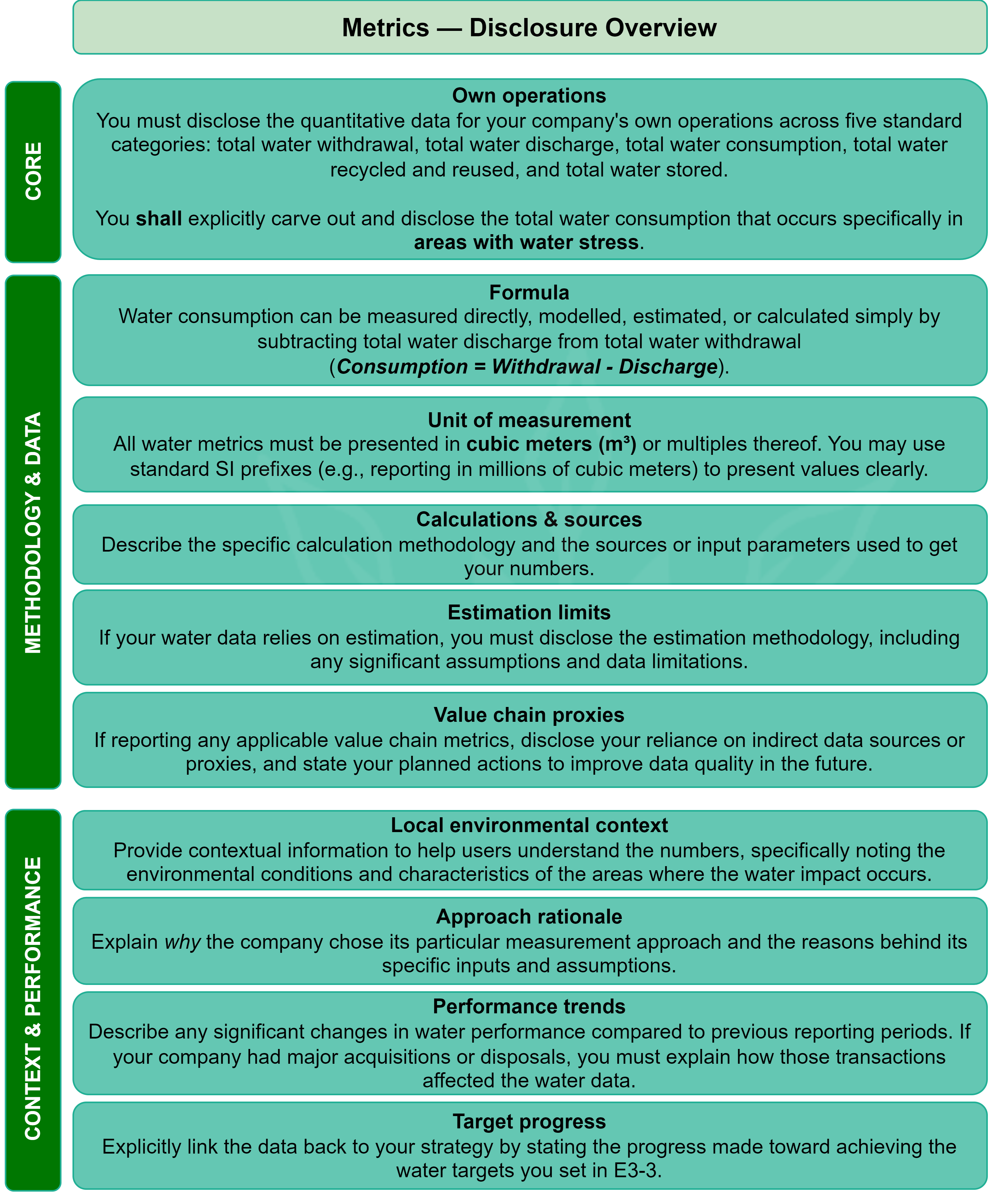

3. ESRS E3-4 at a glance

ESRS E3-4 requires that the undertaking disclose key water performance metrics for its own operations in accordance with the provisions of ESRS 2 GDR-M.

To comply with the standard, you must disclose the following:

4. How E3-4 links to the rest of ESRS E3

E3-4 is the ultimate proof of performance for your water strategy:

E3-1 (Policy): Establishes the commitment to reduce your impact on vulnerable water basins.

E3-2 (Action): Describes the installation of a new water recycling system.

E3-3 (Target): Sets the goal to reduce freshwater consumption in water-stressed areas by 30% by 2030.

E3-4 (Metric): The reality check. Reports the actual cubic meters consumed, withdrawn, discharged, stored, and recycled/reused, verifying whether the actions (E3-2) achieved the target (E3-3).

5. Bottom line

E3-4 is heavily data-dependent, and water accounting is notoriously tricky. To report effectively:

Master the definitions: Strictly follow the standard definitions for withdrawal, discharge, consumption, recycling/reuse, and storage.

Pinpoint the stress: The most highly scrutinized number in this disclosure will be water consumption in areas with water stress. Investors are increasingly treating this specific metric as a proxy for physical climate risk.

Meter your operations: Estimation is allowed, but primary data is always preferred. If you don’t have water meters installed at your major production sites, you need to start planning those CapEx investments now.

Provide contextual detail: Accompany the raw metrics with local environmental context and clear methodological assumptions to make the data understandable to users.

![[INSIGHT] Water scarcity, water stress, and water risk: What’s the difference?](https://substackcdn.com/image/fetch/$s_!atiX!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fef616b57-0c24-413f-9b8a-5f78750eca27_1857x1731.png)