The climate change guide: Everything you need to know about emissions reporting and ESRS E1

A practical guide to understanding climate change, emissions disclosure, and the ESRS E1 reporting framework.

Last updated: 09-10-2025

1. Introduction

Climate change has become a defining business issue. Companies across all sectors are expected to measure their environmental footprint and to demonstrate how they will transition to a climate-neutral economy.

This article isn’t only for companies in scope of the CSRD. It’s for any organisation that wants to report credibly on climate: EU or non-EU, listed or private, big or small. I use European Sustainability Reporting Standard (ESRS) E1 as a clear and practical blueprint for climate disclosure. If CSRD doesn’t apply to you (yet), you can still use this guide to structure your reporting.

ESRS E1 addresses how companies disclose their climate change impacts, risks, and opportunities, along with the strategies, actions, and metrics that support them. It is designed to align business reporting with the Paris Agreement, the EU Climate Law, and global standards such as the GHG Protocol and ISO 14064.

In this article, you will learn:

✅ What climate change is

✅ The main objectives of ESRS E1

✅ How ESRS E1 connects with other environmental standards, like water and biodiversity

✅ The key components of ESRS E1 (E1-1 to E1-11), from transition plans to financial impacts

✅ Acronyms and terms used in ESRS E1

By the end, you’ll gain a clear, structured understanding of ESRS E1.

Before we dive into the guide, here is an overview of all articles that are currently available.

Missing something? Please send me a message or place a comment.

You can find any of these articles by navigating to sustainabilitysimplified.eu/

and using the search button.

2. What is climate change?

First of all, it is important to know what climate change actually is. In short: Climate change is the long-term alteration of Earth's average weather patterns, including shifts in temperature and precipitation.

In today's world, climate change is becoming more and more evident. Escalating floods, relentless droughts, and scorching heatwaves have been observed. Simultaneously, extreme weather events, leave millions of people grappling with acute food and water shortages.

The threat of global warming at 1.5 degrees Celsius carries irrevocable consequences. Central to this crisis is the burning of fossil fuels for electricity generation. This practice inundates the atmosphere with greenhouse gases, leading to global warming.

For context, in 2020, a staggering 73% of total anthropogenic greenhouse gas emissions originated from fossil fuel combustion. To avoid catastrophic temperature increases and limit global warming to 1.5 degrees Celsius, an urgent transformation is needed: achieving net-zero emissions by 2050, a goal championed by the United Nations in 2022.

Because, climate change is so important it is included as the first ESRS E in the CSRD.

3. Understanding the objective of ESRS E1

The objective of ESRS E1 is straightforward: it requires companies to disclose information on climate change whenever it represents a material impact, risk, or opportunity for the business. This covers policies, actions, targets, dependencies, metrics, and anticipated financial effects.

The standard defines three sub-topics:

Climate change mitigation – reducing greenhouse gas (GHG) emissions in line with the Paris Agreement and EU Climate Law.

Climate change adaptation – adjusting to actual or expected climate impacts, such as physical risks.

Energy – reporting on energy production and consumption.

Interaction with other topics (ESRS Standards)

Importantly, ESRS E1 interacts with other topical standards. For example, ESRS E1 focuses on seven main greenhouse gases (like CO₂ and methane). Other harmful air emissions, such as ozone-depleting substances, are covered in ESRS E2.

Climate change also connects closely with ESRS E3 Water and ESRS E4 Biodiversity. For example, changes in climate can cause water-related problems, like floods and droughts, which in turn affect ecosystems and species. Actions to fight climate change, such as protecting forests, restoring wetlands, or changing how land is used, can also help nature. These “nature-based solutions” can reduce greenhouse gases while improving water quality, protecting wildlife habitats, and keeping ecosystems healthy.

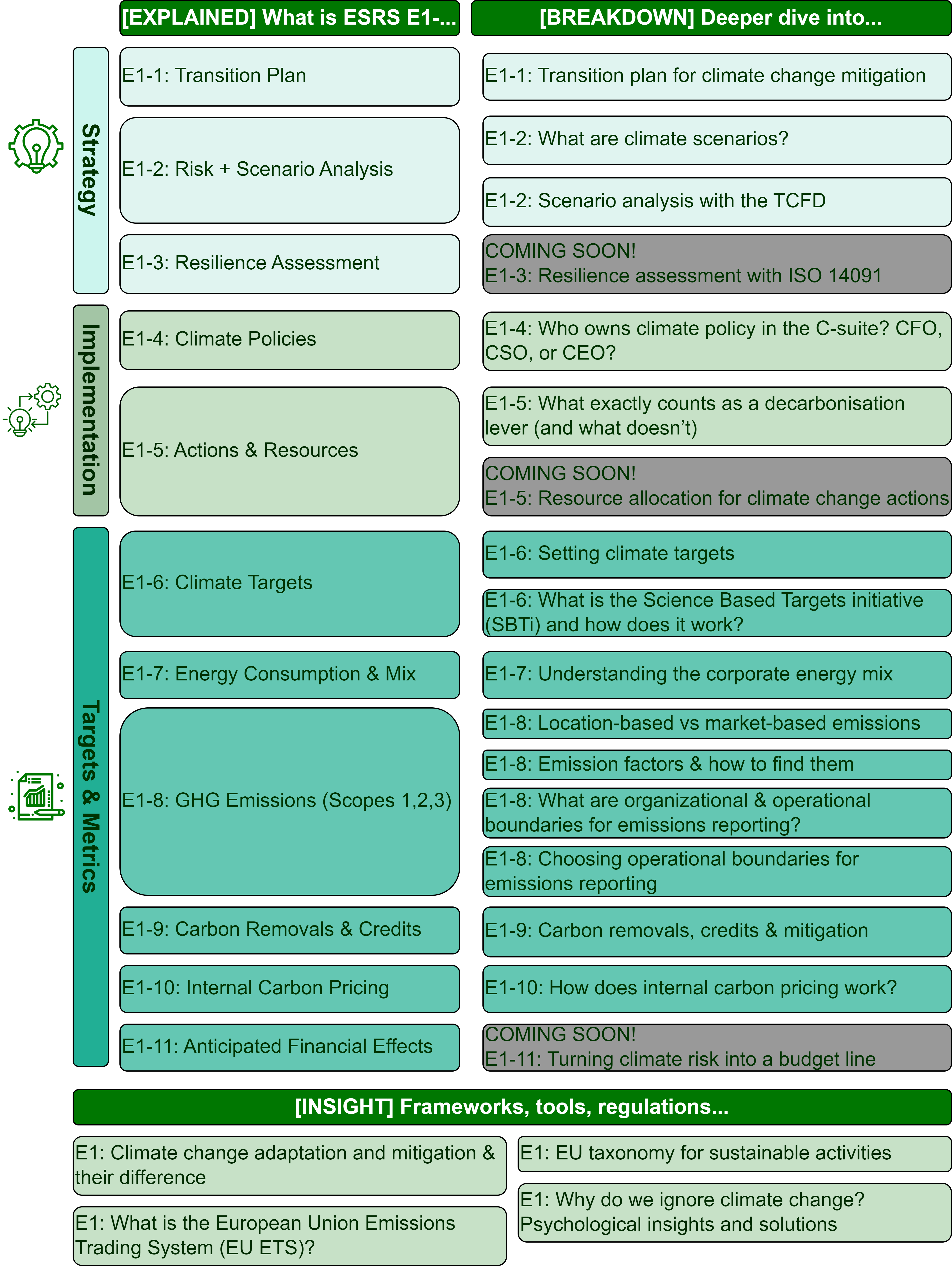

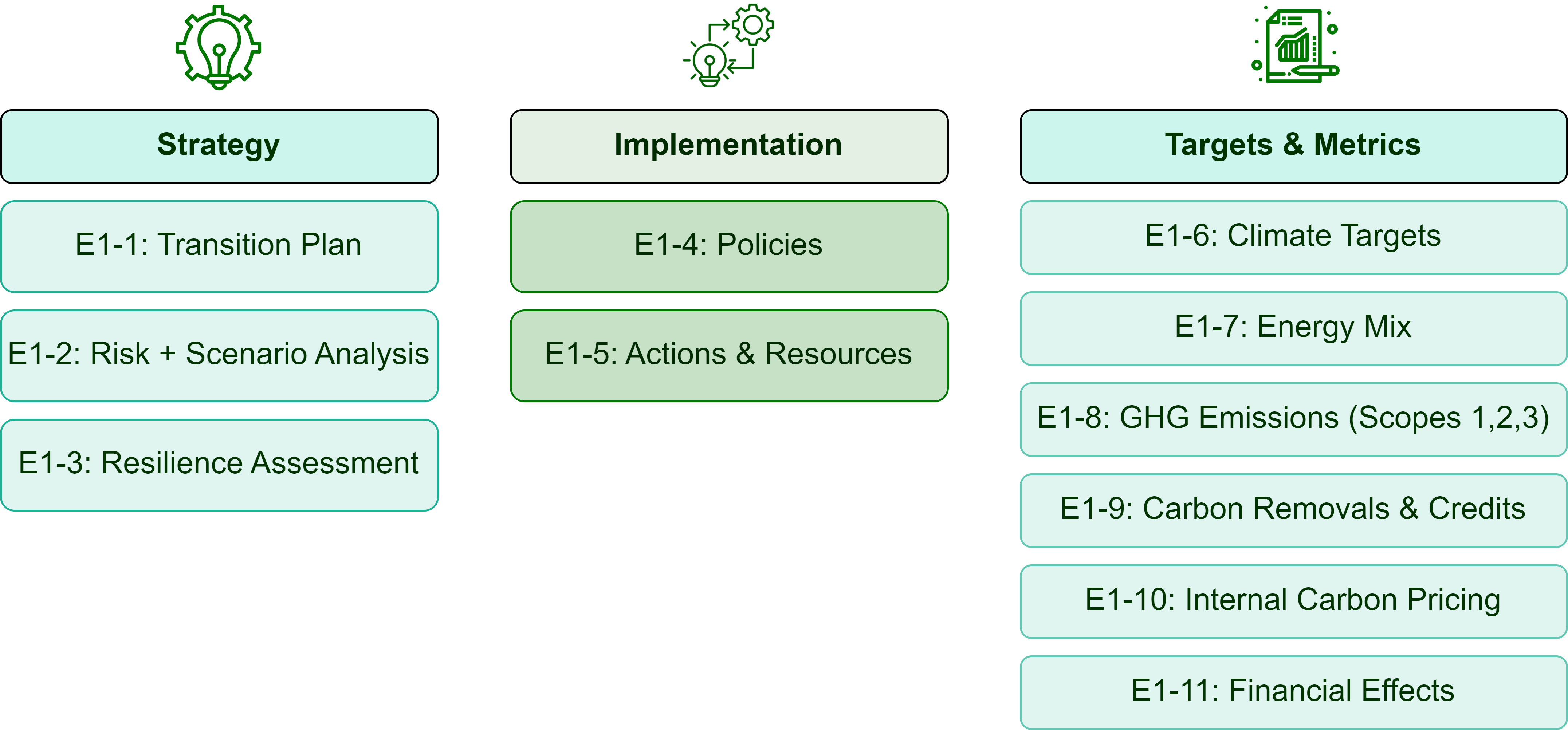

4. The different components of ESRS E1

The standard is structured around three pillars: Strategy (long-term plans, risk analysis, and resilience), Implementation (policies, actions, and resources), and Targets & Metrics (quantifiable goals, emissions data, and financial implications).

Read more below to explore each element in detail. I’ve also linked to my other articles below, where you can dive deeper into each specific topic, from ESRS E1-1 through ESRS E1-11, for a more comprehensive understanding.

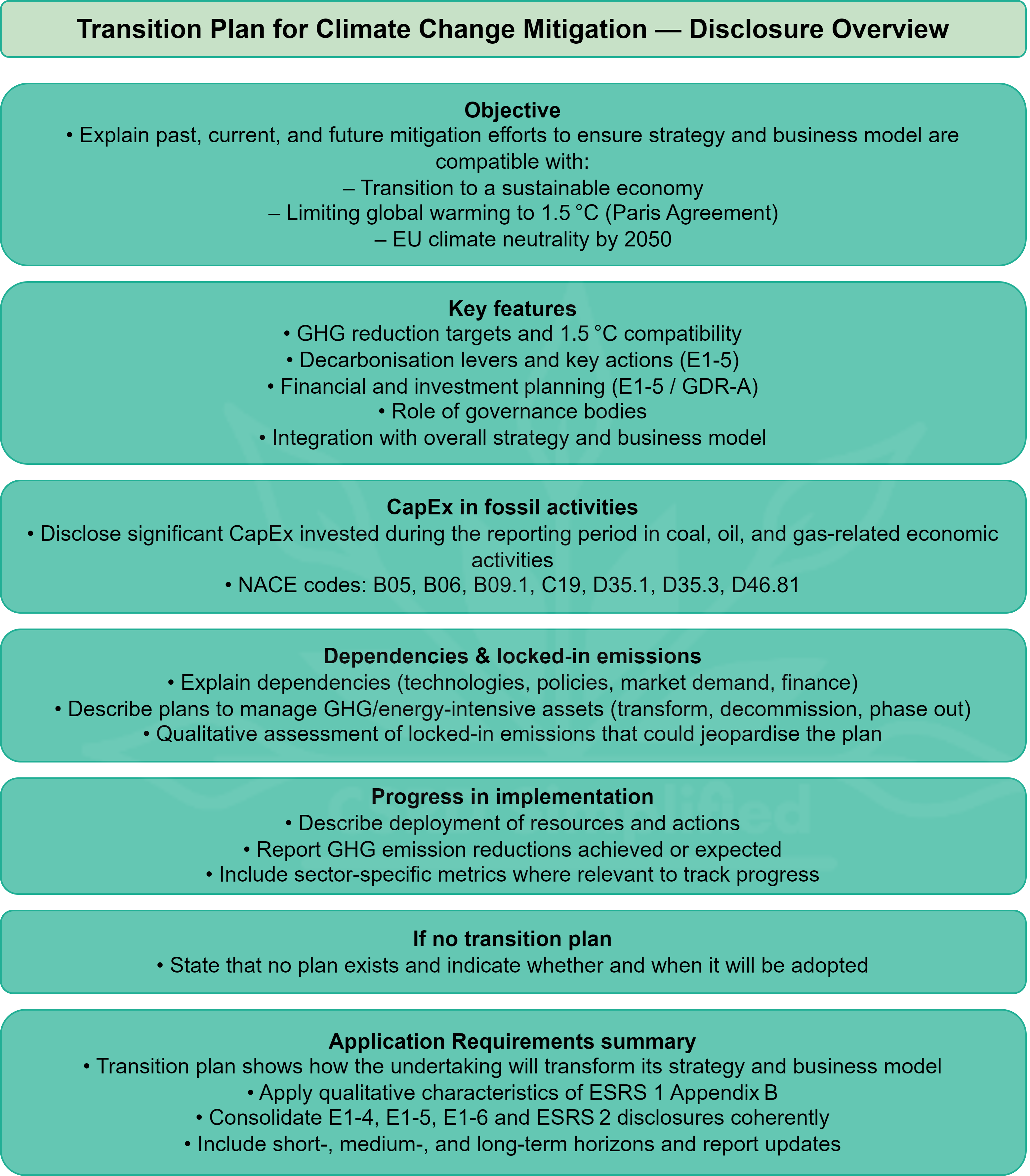

E1-1: Transition plans: the cornerstone of mitigation

The transition plan for climate change mitigation (E1-1) is arguably the heart of ESRS E1. Companies must disclose how their strategy and business model align with limiting global warming to 1.5°C and achieving climate neutrality by 2050.

If no transition plan exists, companies must state whether they intend to adopt one and when.

Read more about ESRS E1-1 here:

![[EXPLAINED] E1-1: Transition plan](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

E1-2, E1-3: Climate-related risks and resilience

E1-2: Identifying risks through scenario analysis

Under E1-2, companies must explain how they identify and assess climate-related risks and opportunities. These are split into:

Physical risks (acute and chronic hazards such as floods, droughts, or heatwaves)

Transition risks (regulatory, market, or technological changes from the shift to a low-carbon economy)

Read more about ESRS E1-2 here:

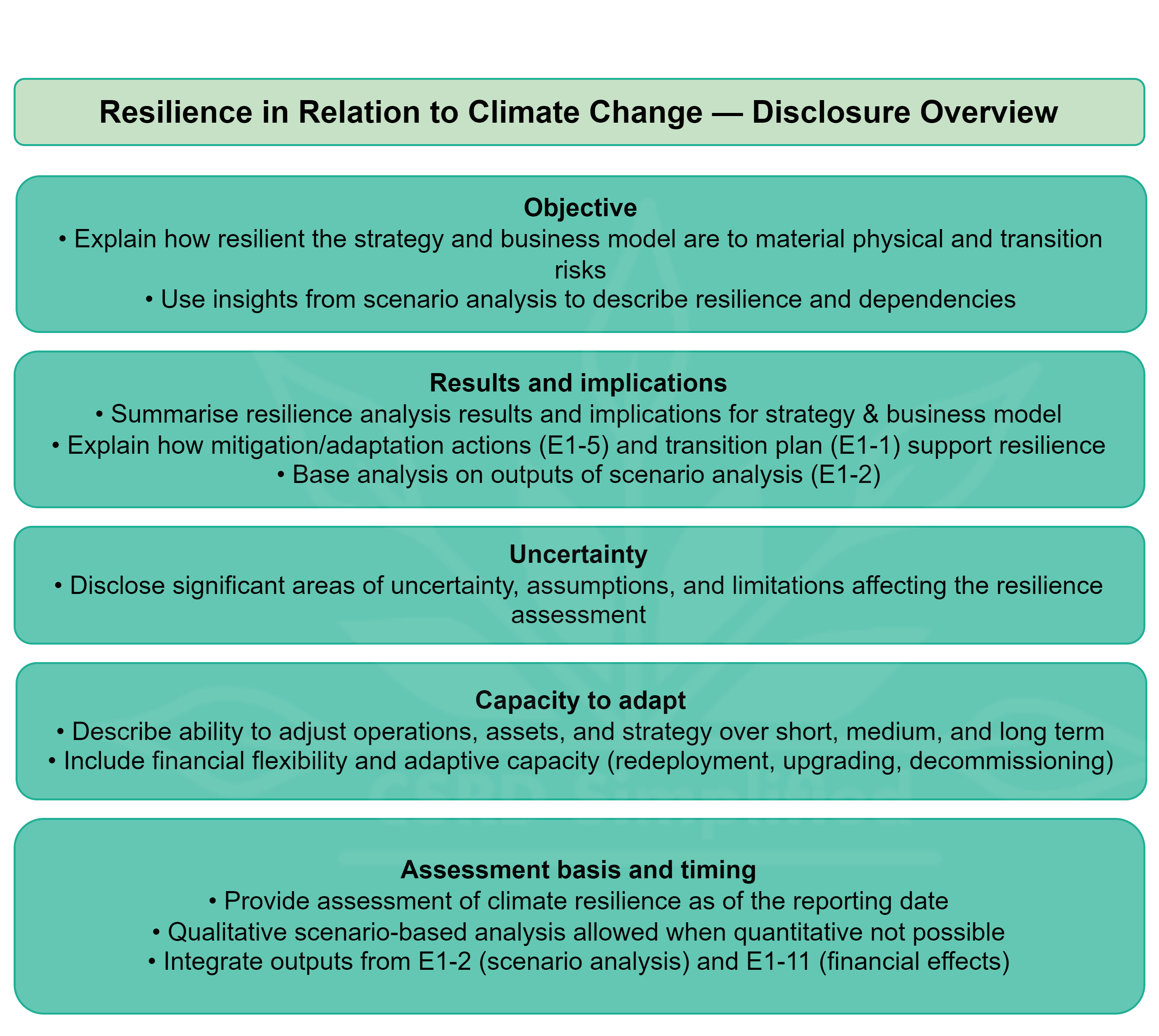

E1-3: Resilience of strategy and business model

E1-3 requires disclosure of how resilient the company’s strategy and business model are in relation to identified risks.

Read more about ESRS E1-3 here:

E1-4, E1-5: Policies, actions, and resources

Beyond strategy, ESRS E1 emphasizes operational measures.

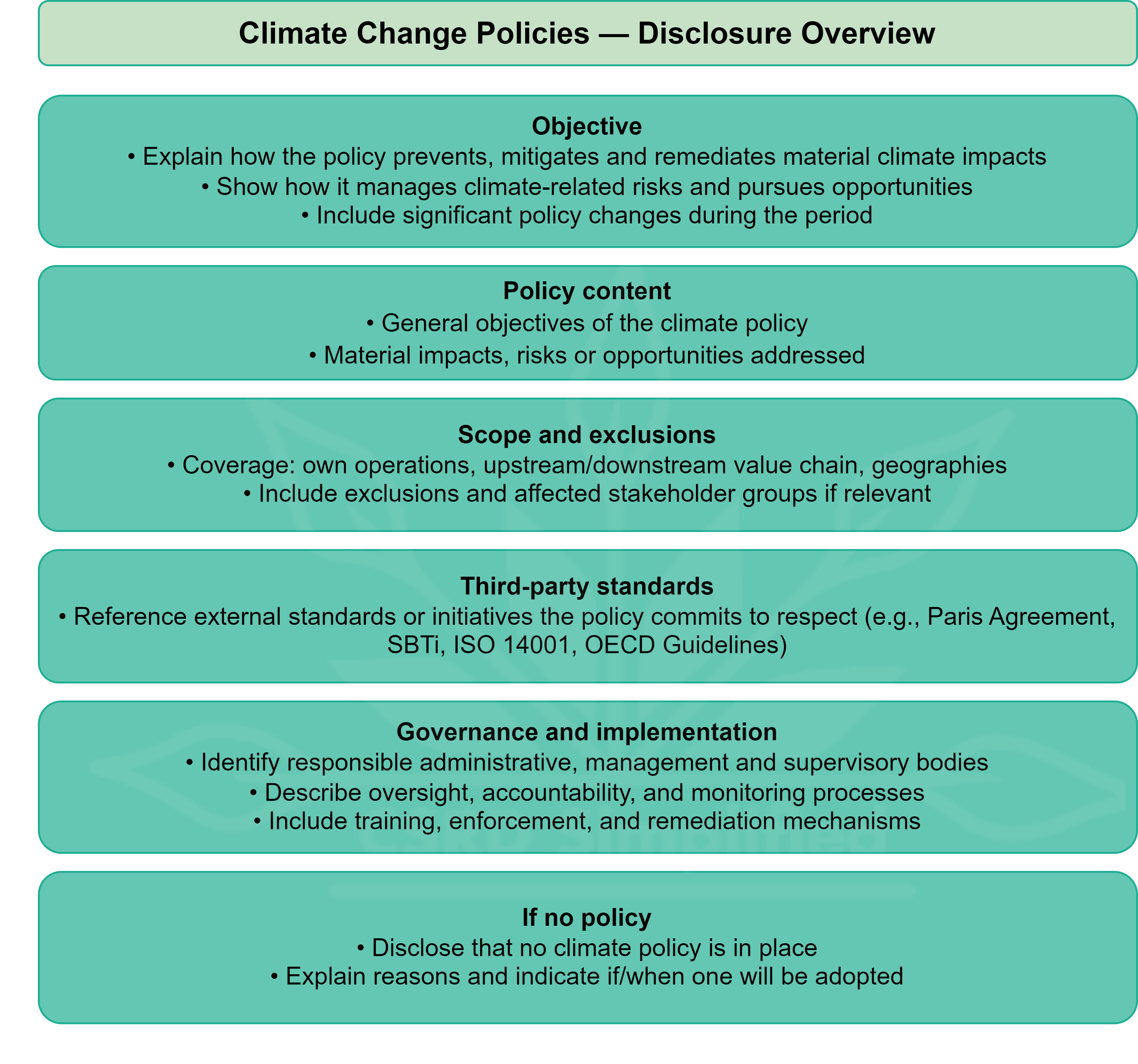

E1-4 (Policies): disclosure of climate policies in line with ESRS 2.

Read more about ESRS E1-4 here:

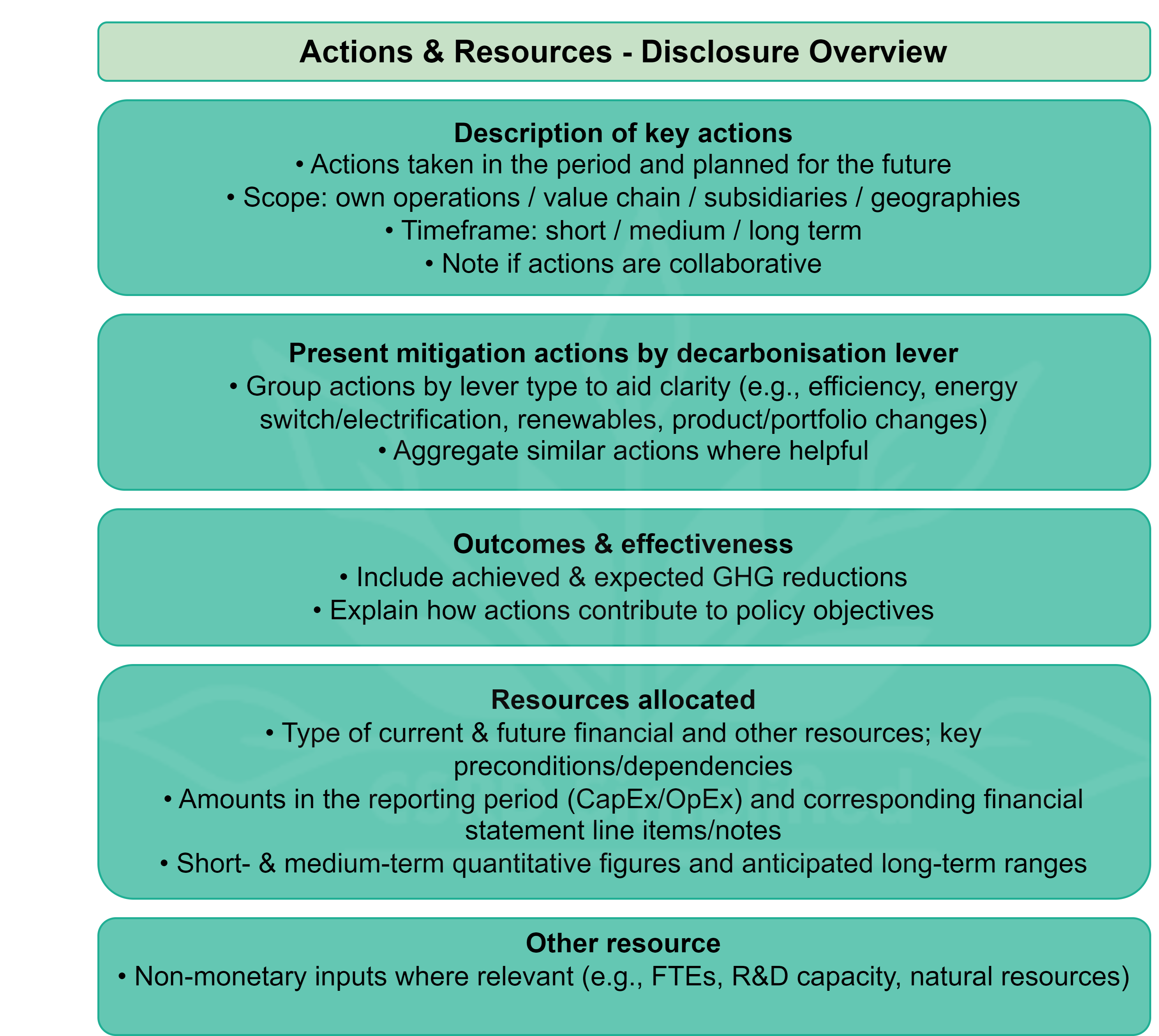

E1-5 (Actions and resources): companies must report their key mitigation actions, expected GHG reductions, and financial resources allocated—quantified where possible as CapEx/OpEx.

Read more about ESRS E1-5 here:

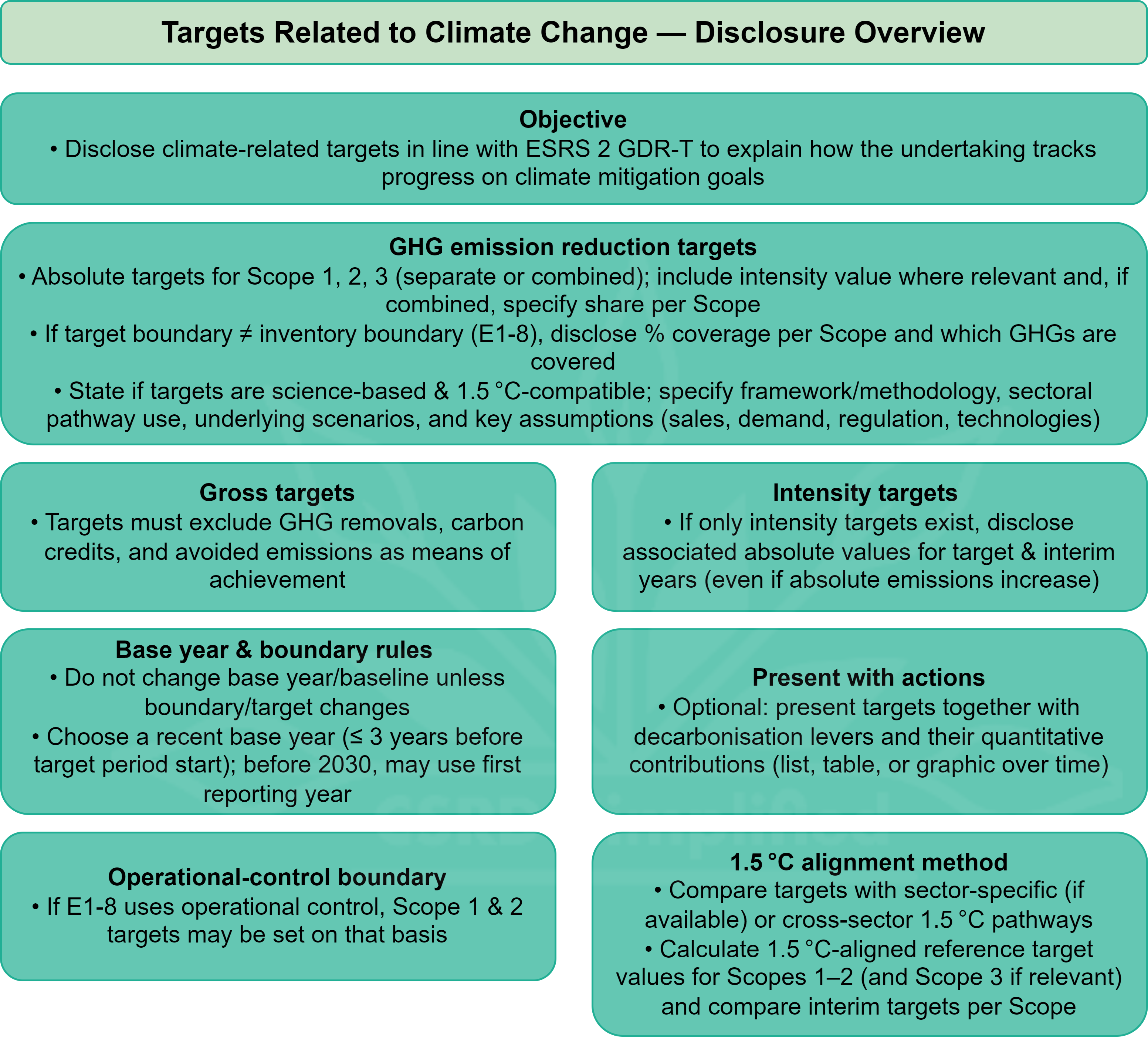

E1-6: Absolute, science-based, and transparent targets

E1-6 focuses on climate targets, particularly GHG reduction. Targets must be gross, excluding removals or carbon credits. Intensity targets are allowed but must be accompanied by absolute values.

Read more about ESRS E1-6 here:

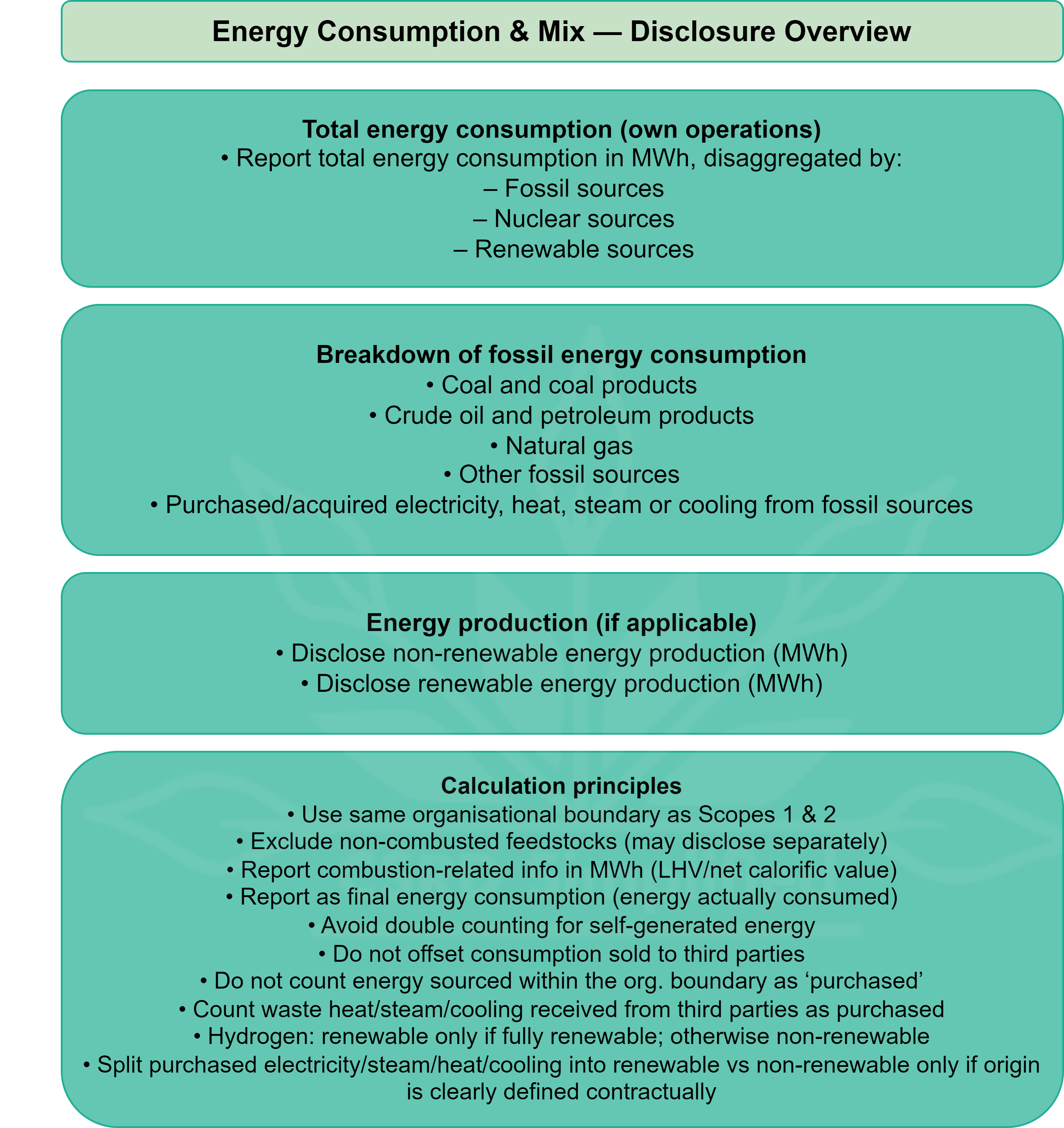

E1-7: Energy consumption and mix

E1-7 requires disclosure of total energy consumption.

This disclosure links directly with SFDR indicators on non-renewable energy use, ensuring financial market participants can assess transition alignment.

Read more about ESRS E1-7 here:

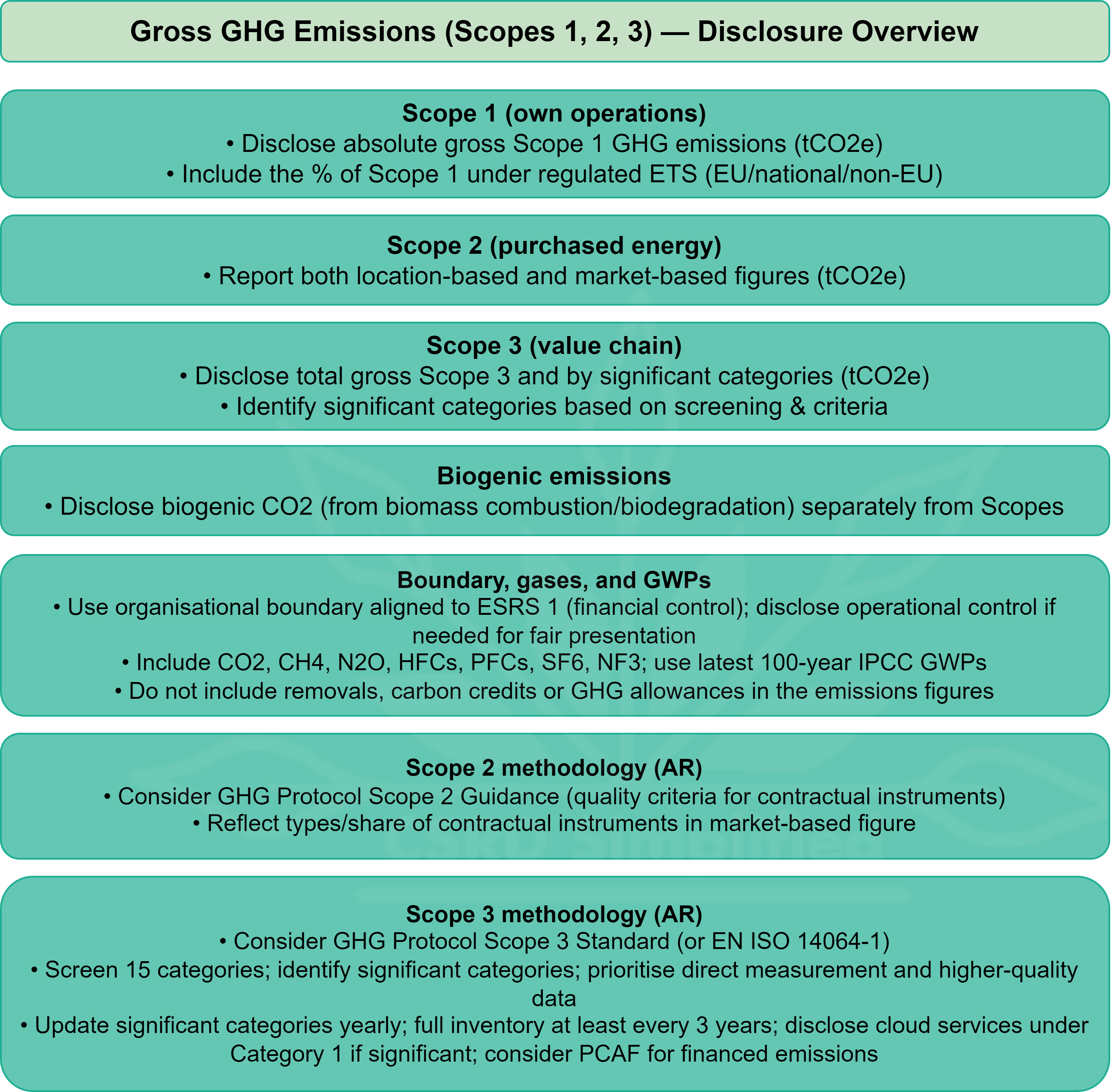

E1-8: Measuring GHG emissions

The most technical requirement is E1-8, which mandates disclosure of gross Scope 1, 2, and 3 emissions:

Scope 1: direct emissions (with percentage under emissions trading schemes)

Scope 2: indirect emissions (both location-based and market-based)

Scope 3: significant categories across the value chain, disaggregated

Read more about ESRS E1-8 here:

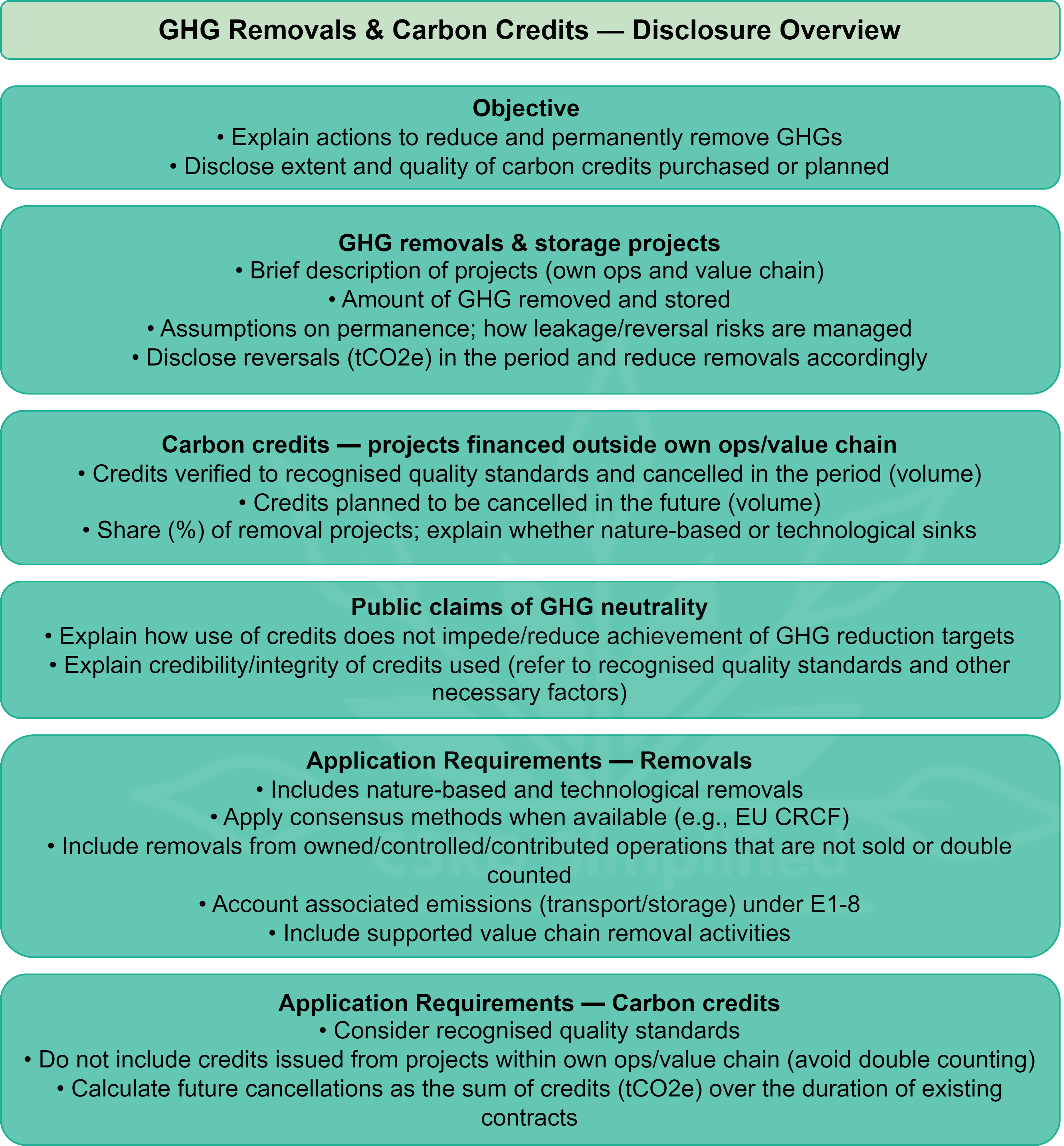

E1-9, E1-10: Carbon removals, credits, and internal pricing

E1-9 addresses carbon removals and credits. Companies must disclose projects for GHG removal (e.g., nature-based or technological) and their permanence, reversals, and leakage risks.

Read more about ESRS E1-9 here:

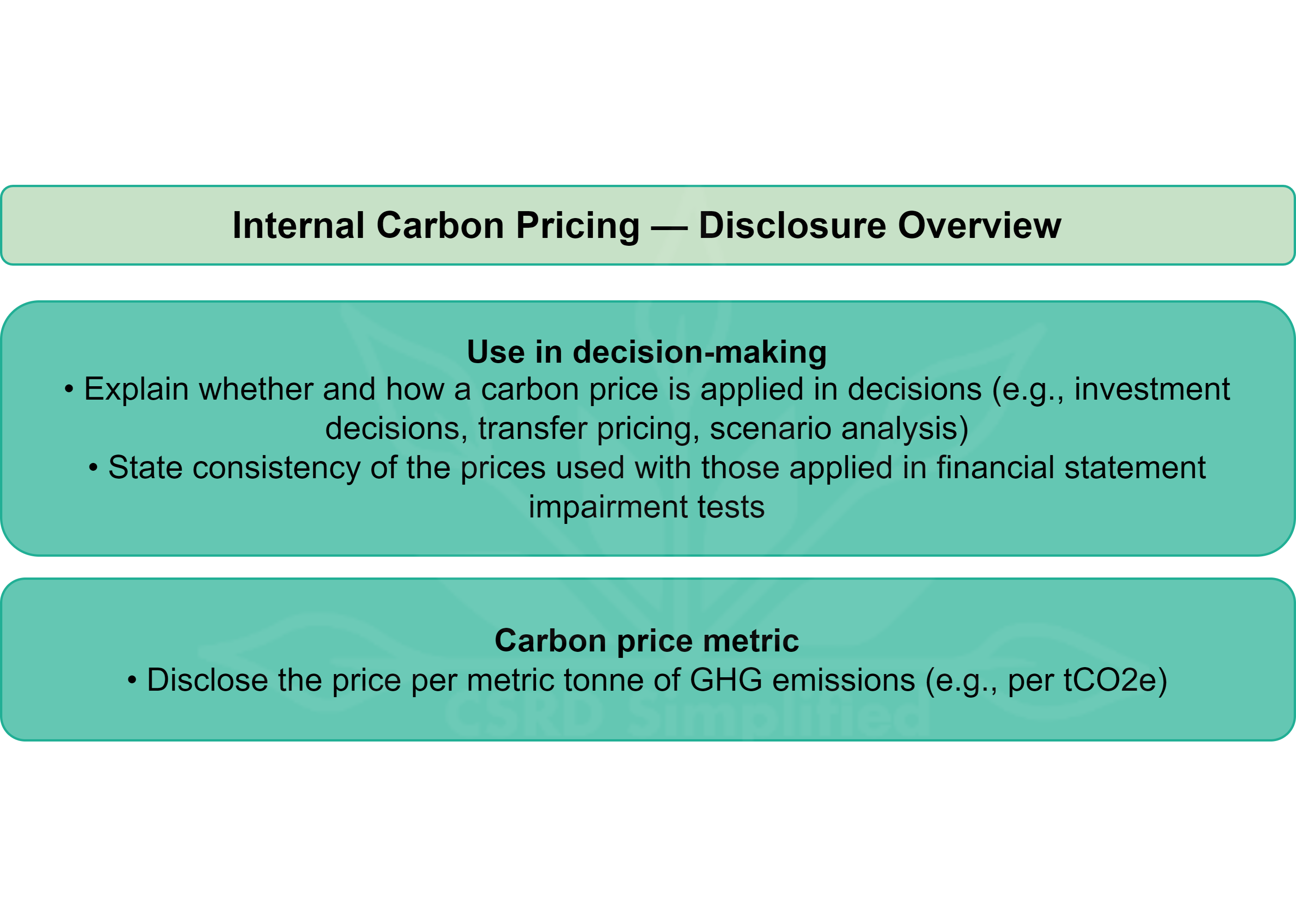

E1-10 requires disclosure of internal carbon pricing: how carbon prices are used in decision-making and the price per tonne applied.

Read more about ESRS E1-10 here:

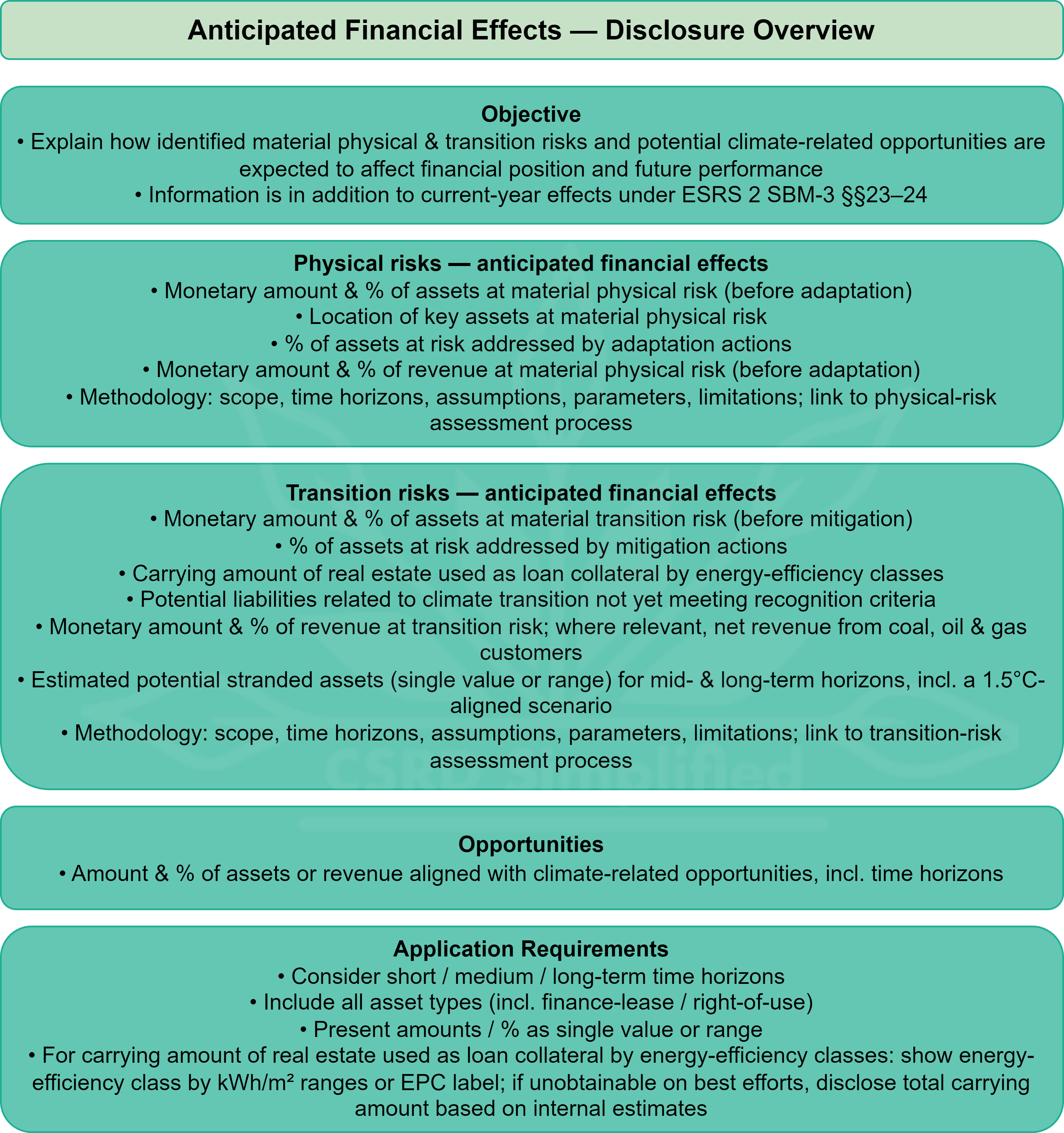

E1-11: Financial effects of climate risks and opportunities

Finally, E1-11 requires companies to quantify the anticipated financial effects of climate risks and opportunities.

Read more about ESRS E1-11 here:

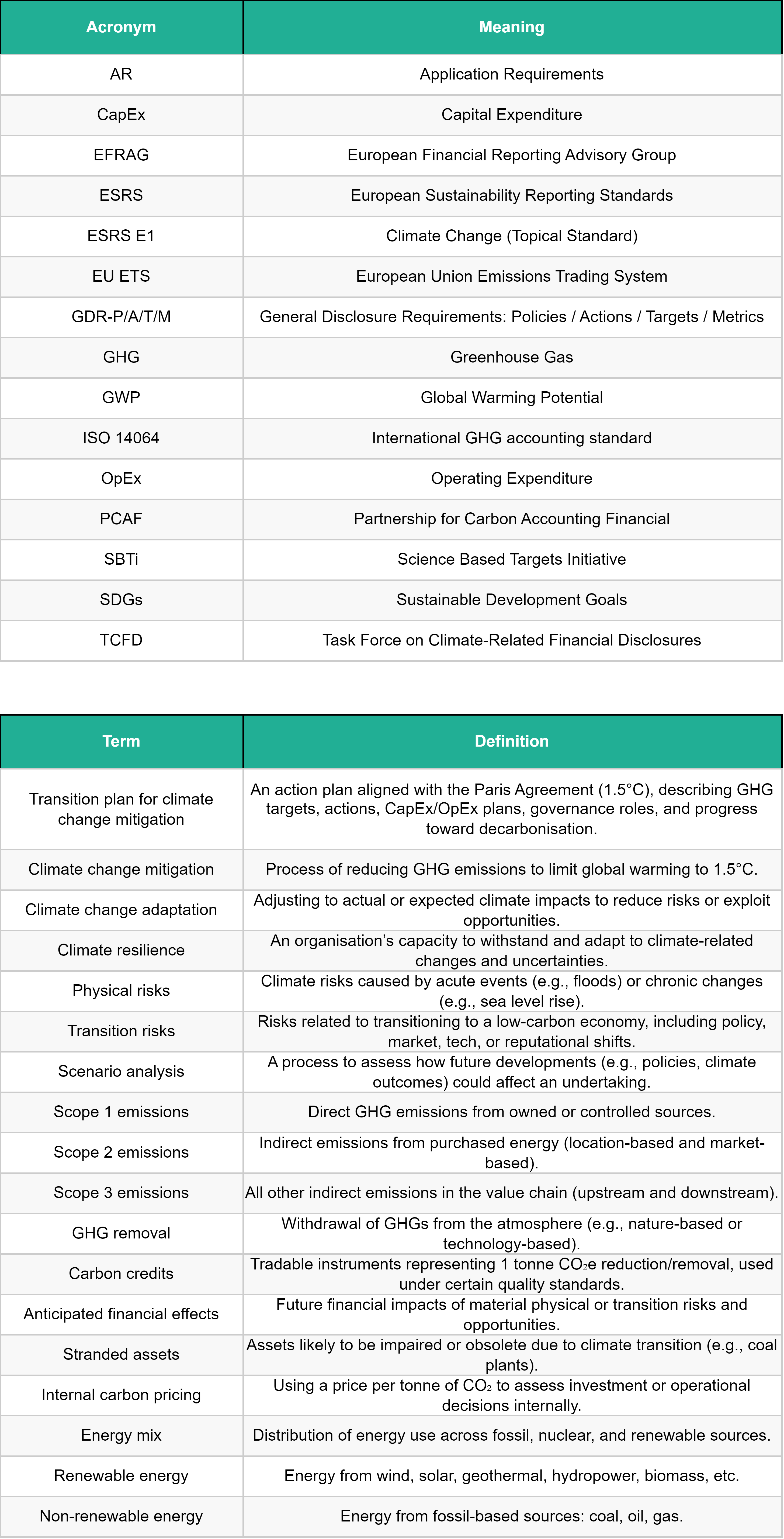

4. Acronyms and terms

Relevant Sources

Amended ESRS E1 – Exposure Draft – July 2025

IPCC. (2022). Climate Change 2022: Impacts, Adaptation and Vulnerability . https://doi.org/10.1017/9781009325844

Gür, T. M. (2018). Review of electrical energy storage technologies, materials and systems: challenges and prospects for large-scale grid storage. Energy & Environmental Science, 11(10), 2696–2767. https://doi.org/10.1039/C8EE01419A

Excellent overview, Lars. What I find interesting is how E1 forces the integration of climate strategy, governance, and financial planning, turning “sustainability reporting” into business transformation. It’s also a test case for how future ESRS topics will operationalize double materiality across impacts, risks, and opportunities.