[BREAKDOWN] E1-2: Scenario analysis with the TCFD

ESRS E1: Scenario analysis with the TCFD

1. Introduction

The European Sustainability Reporting Standards (ESRS) E1 is a cornerstone of corporate climate accountability, requiring companies to grapple with the complexity of scenario analysis. This analysis is critical for identifying and assessing material climate-related impacts, risks, and opportunities (as outlined in ESRS 2 IRO-1) and understanding how these factors interact with your strategy and business model (as specified in ESRS 2 SBM-3).

At first glance, this may sound overwhelming, but there’s a robust roadmap to guide us: the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD). Specifically, the 2017 Technical Supplement: The Use of Scenario Analysis in Disclosure of Climate-Related Risks and Opportunities and the Guidance on Scenario Analysis for Non-Financial Companies offer invaluable insights for tackling ESRS E1 requirements. Let’s break it down.

2. Why scenario analysis?

Scenario analysis is not just a regulatory checkbox—it’s a way to future-proof your organization. By exploring how plausible climate-related scenarios could unfold, businesses can:

Identify risks like extreme weather disruptions, carbon pricing policies, or resource scarcity.

Uncover opportunities such as shifts in consumer behavior toward green products or emerging markets for renewable technologies.

Make better-informed strategic decisions to thrive in an uncertain future.

In essence, scenario analysis forces us to move beyond linear thinking and embrace climate risks and opportunities.

3. The role of TCFD in ESRS E1 compliance

TCFD’s guidance remains a valuable reference for meeting ESRS E1 on climate-related risks and scenario analysis. Its resources, including the Technical Supplement and the Guidance for Non-Financial Companies, can help companies structure their analysis to meet disclosure expectations.

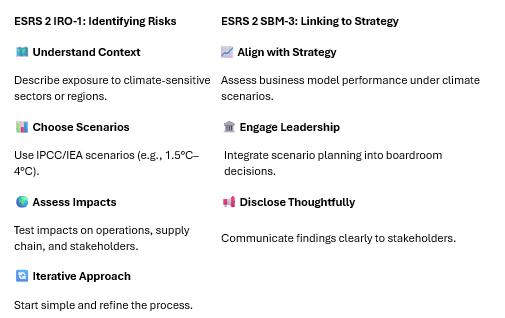

Under ESRS E1-2, companies must explain for each climate-related material risk whether it is a physical risk or a transition risk (as identified under ESRS 2 IRO-1 and IRO-2), and disclose the key elements of the methodology used. TCFD’s approach supports this by helping companies:

Define the scope of the analysis, including own operations and value chain.

Select relevant scenarios (e.g., IPCC, IEA) covering short-, medium-, and long-term horizons.

Identify and assess climate-related hazards (physical risks) with spatial resolution, and evaluate exposure and sensitivity of assets based on likelihood, magnitude, and duration — including at least one high-emission scenario.

Identify and assess transition events and trends (transition risks) and evaluate exposure and sensitivity under at least one 1.5°C-aligned scenario with no or limited overshoot.

Document the methodologies, tools, and timeframes used, and explain how scenario analysis informs strategic decision-making.

By following TCFD’s structured process, companies can also link their scenario analysis to strategy (ESRS 2 SBM-3), ensuring that climate-related risks and opportunities are integrated into governance, business planning, and transparent disclosures for stakeholders.

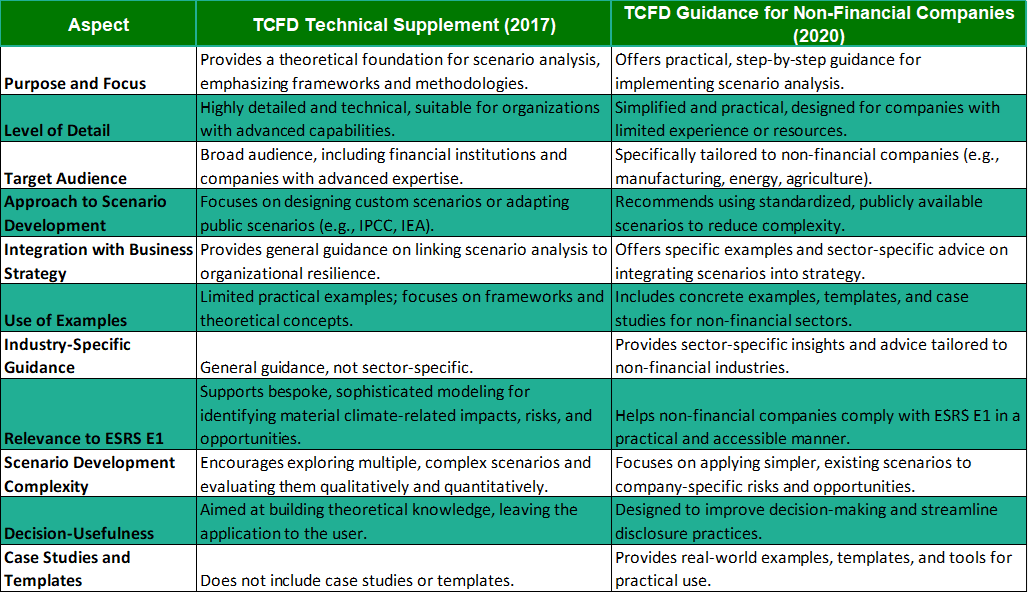

4. Differences between the Technical Supplement and the Guidance for Non-Financial Companies

A comparison illustrates the Technical Supplement as more suited for organizations seeking an advanced, theoretical approach, while the Non-Financial Guidance offers practical, hands-on assistance for companies needing accessible methodologies.

5. Practical steps for using TCFD in ESRS E1 reporting

Here we present a structured approach to conducting climate-related scenario analysis, based on the TCFD Technical Supplement (2017) as a foundation, with additional practical elements from the Non-Financial Guidance (2020).