[EXPLAINED] E1-8: GHG Emissions (Scopes 1,2,3)

ESRS E1-8: Gross Scopes 1, 2 and 3 GHG emissions

1. Introduction

Greenhouse gas (GHG) emissions are the main cause of climate change — and one of the clearest indicators of a company’s climate impact.

E1-8 requires companies to measure and disclose how much GHG they emit, where those emissions come from, and how they are changing over time.

This disclosure is one of the most data-heavy under ESRS E1, but it’s also the backbone of your entire climate report. Your actions, targets, and transition plan all rely on these numbers.

I will briefly explain the requirements for companies to disclose their gross Scopes 1, 2 and 3 GHG emissions.

More elaborate articles are available, which can be found below.

2. What are greenhouse gas (GHG) emissions?

Greenhouse gases (GHGs) are gases in the atmosphere that trap heat from the sun and make the Earth warmer — a natural process known as the greenhouse effect.

Human activity, especially the burning of fossil fuels, has sharply increased the amount of these gases, which is why the planet is heating faster than ever before.

The main greenhouse gases are:

Carbon dioxide (CO₂) – released from burning coal, oil, and gas, or from deforestation.

Methane (CH₄) – emitted from livestock, waste, and gas leaks.

Nitrous oxide (N₂O) – from fertilisers and industrial processes.

Fluorinated gases (HFCs, PFCs, SF₆, NF₃) – used in cooling systems and manufacturing.

Because each gas traps different amounts of heat, they’re combined into a single unit called CO₂ equivalent (CO₂e).

This lets companies report a total climate impact as one comparable number — for example:

“Our operations emitted 1.2 million tonnes of CO₂e in 2024.”

So, when we talk about GHG emissions, we mean all the gases that contribute to global warming, expressed together as CO₂ equivalents.

The ESRS defines GHG as follows:

“Greenhouse Gases (GHG) The gases listed in Part 2 of Annex V of Regulation (EU) 2018/1999 of the European Parliament and of the Council8 . These include Carbon dioxide (CO2), Methane (CH4), Nitrous Oxide (N2O), Sulphur hexafluoride (SF6), Nitrogen trifluoride (NF3), Hydrofluorocarbons (HFCs), Perfluorocarbons (PFCs).”

3. Understanding the scopes

The ESRS uses the same structure as the GHG Protocol, which divides emissions into three scopes:

Scope 1 – Direct emissions

Emissions from sources you own or control, such as company vehicles, boilers, or production facilities.Scope 2 – Indirect emissions from energy

Emissions from the electricity, heat, or steam you purchase and use. They occur at your energy supplier, but result from your energy demand.Scope 3 – Other indirect emissions

Emissions that happen in your value chain, both upstream and downstream — for example:Purchased goods and materials

Employee commuting and business travel

Product use and disposal

Transport, investments, and cloud services

Scope 3 is usually the largest and hardest to measure but gives the most complete view of your footprint.

The ESRS defines the scopes as follows:

“Scope 1 GHG emissions Direct GHG emissions from sources that are owned or controlled by the undertaking.

Scope 2 GHG emissions Indirect emissions from the generation of purchased or acquired electricity, steam, heat or cooling consumed by the undertaking. Scope 3 GHG emissions All indirect GHG emissions (not included in Scope 2 GHG emissions) that occur in the value chain of the reporting undertaking, including both upstream and downstream emissions.

Scope 3 GHG emissions can be broken down into Scope 3 categories.”

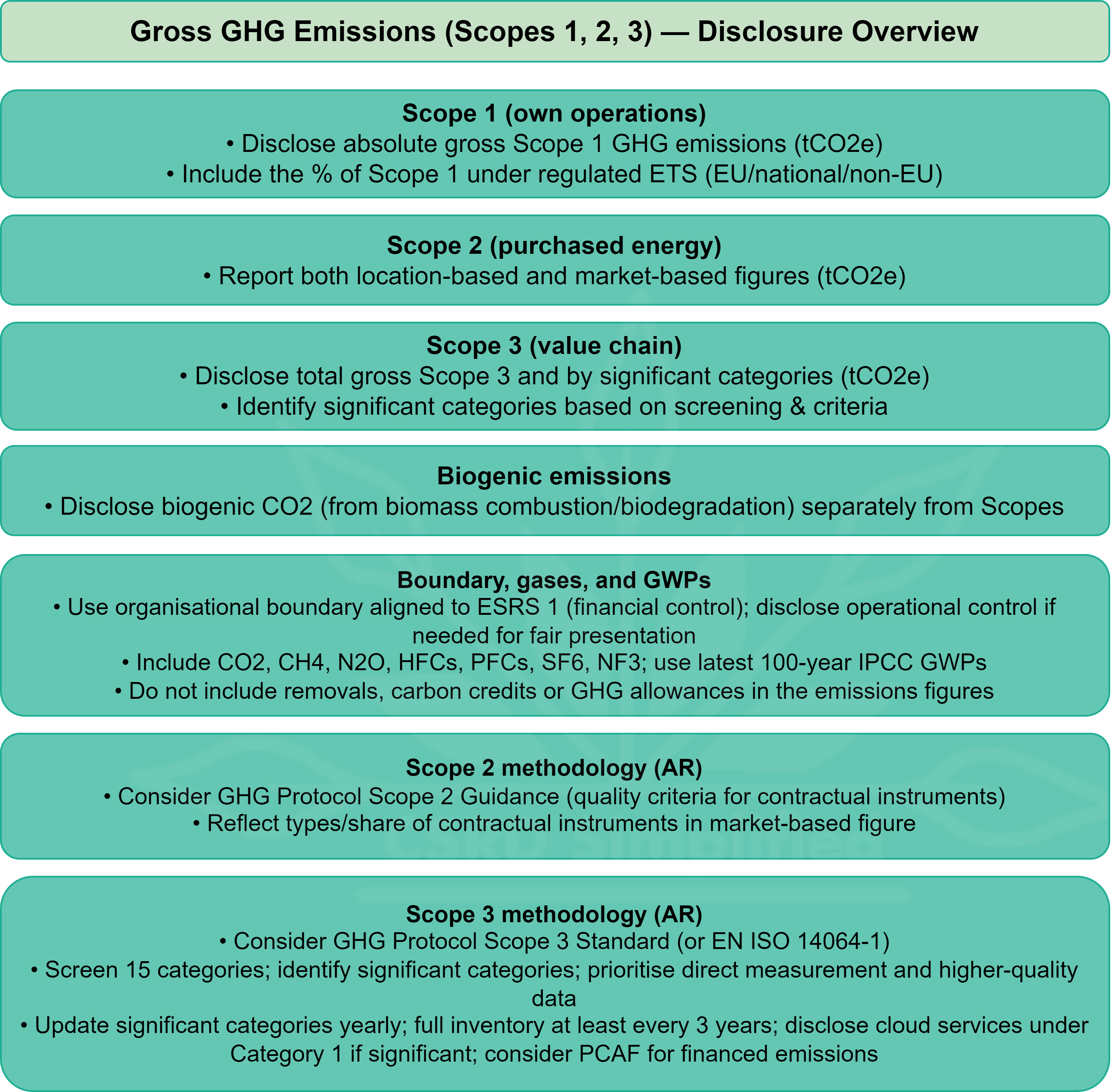

4. ESRS E1-8 at a glance

E1-8 requires you to disclose:

Read about boundaries for emissions reporting:

Read more about choosing operational boundaries here:

Read about location-based vs market-based emissions:

Read about emission factors:

Read about the EU ETS:

![[BREAKDOWN] E1-8: What are organizational & operational boundaries for emissions reporting?](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

5. How E1-8 links to the rest of ESRS E1

E1-8 gives the baseline for your emissions footprint.

E1-6 (targets) and E1-5 (actions) use these numbers to show how emissions will fall over time.

E1-1 (transition plan) brings it all together by explaining how your strategy leads to real emission reductions.

Without reliable data under E1-8, the rest of your climate disclosure loses credibility — it’s the foundation of the entire E1 topic.

6. Bottom line

E1-8 is about turning climate impact into numbers that can be tracked and verified. To meet the requirement:

Measure comprehensively across Scopes 1, 2, and 3.

Be transparent about methods, boundaries, and data sources.

Keep consistency so that year-over-year comparisons are meaningful.

Strong GHG data lets you prove progress — and helps investors, regulators, and the public see that your climate actions are producing real results.