[EXPLAINED] E1-5: Actions & Resources

ESRS E1-5: Actions and resources in relation to climate change

1. Introduction

Climate commitments mean little without concrete steps to back them up.

E1-5 focuses on what your company is actually doing to address climate change and how much you’re investing to make it happen.

This disclosure links your policies (E1-4) and your targets (E1-6). It demonstrates that your business is actively implementing plans with actions, funding, and accountability.

I will briefly explain the requirements for companies to disclose their actions and resources in relation to climate change.

More elaborate articles are available, which can be found below.

2. What counts as a climate action?

A climate action is any initiative that reduces greenhouse gas (GHG) emissions, removes them from the atmosphere, or helps the business adapt to climate impacts. Examples include:

Switching to renewable electricity or green heat sources.

Electrifying fleets or production processes.

Improving energy efficiency in buildings and operations.

Developing low-emission products or services.

Engaging suppliers to reduce upstream emissions.

Building flood protection or climate-resilient infrastructure.

Each action should connect back to a specific goal in your transition plan (E1-1) or target (E1-6).

The ESRS defines actions as follows:

“Actions refer to:

i. actions and action plans (including transition plans) that are undertaken to ensure that the undertaking delivers against targets set and through which the undertaking seeks to address material impacts, risks and opportunities; and

ii. decisions to support these with financial, human or technological resources.

Actions can be individual actions, taken only by the undertaking, or collective actions, this is, collaborative efforts by a group of stakeholders - such as undertakings, governments, civil society, or communities - to address shared challenges or achieve common goals, particularly when those goals cannot be effectively achieved by any single actor working alone.”

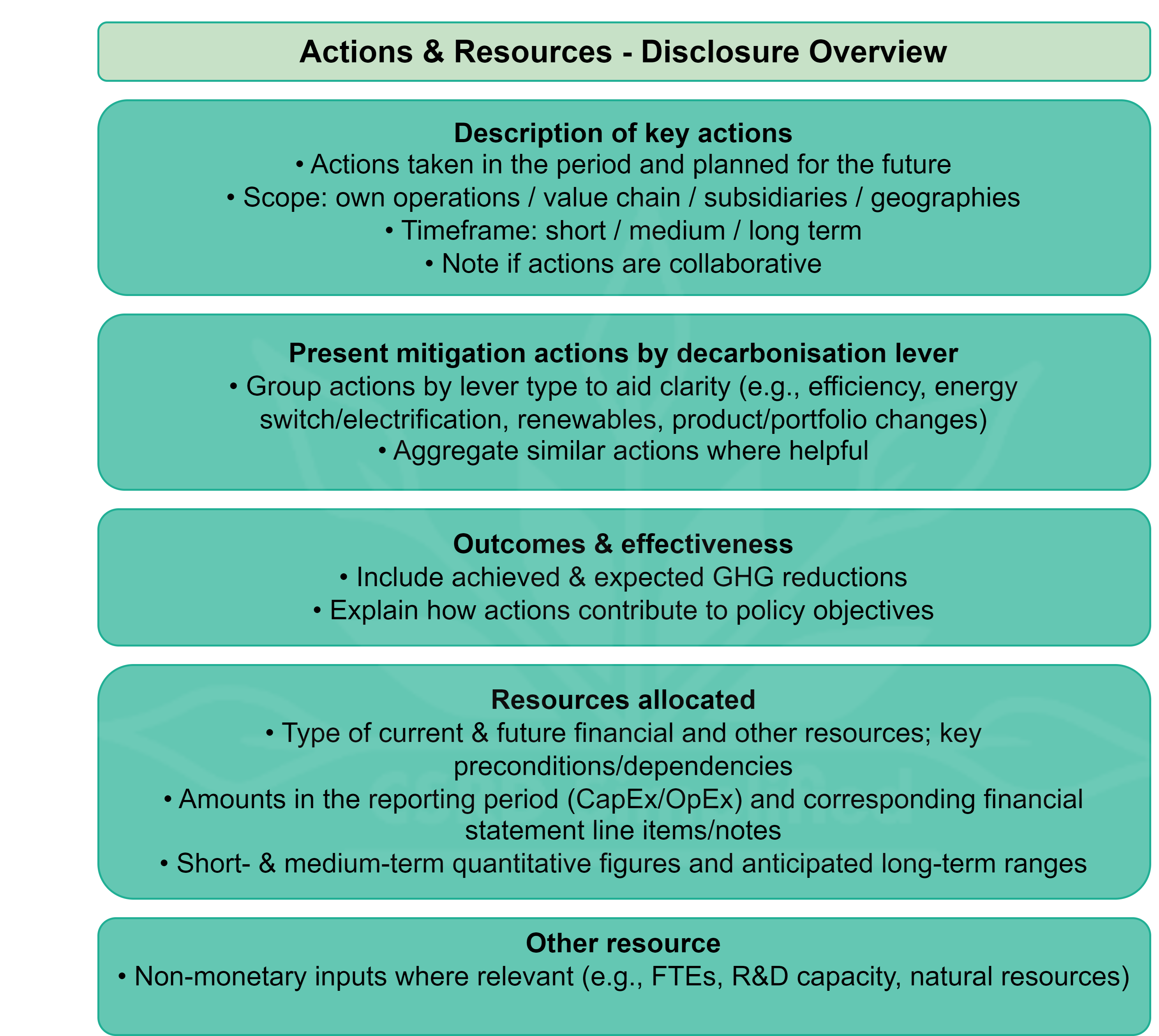

3. ESRS E1-5 at a glance

E1-5 requires you to disclose:

Read about who owns the climate policy in the C-suite here:

More articles about actions and resources coming soon!

![[BREAKDOWN] E1-5: What exactly counts as a decarbonisation lever (and what doesn’t)](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

4. How E1-5 links to the rest of ESRS E1

E1-4 (policies) defines the rules guiding your climate actions.

E1-5 (actions & resources) shows what you’re doing and funding.

E1-6 (targets) explains the goals these actions contribute to.

E1-1 (transition plan) connects them all into a single transformation roadmap.

Together, these disclosures build a credible picture: what your plans are, how you’ll execute them, and whether your investments match your ambition.

5. Bottom line

E1-5 turns your climate strategy into evidence. To meet this requirement and tell a convincing story:

List your key mitigation and adaptation actions, grouped by decarbonisation lever.

Quantify both the financial input (CapEx/OpEx) and the expected emission reductions.

Show progress — what has been done, what is underway, and what comes next.

When done clearly, this section demonstrates that your company is moving from planning to performance — making climate action measurable, funded, and real.