[EXPLAINED] E1-3: Resilience Assessment

ESRS E1-3: Resilience in relation to climate change

1. Introduction

Climate change is also about showing whether your business can withstand climate risks. That’s where E1-3 comes in. This disclosure asks companies to explain how resilient their strategy and business model are when faced with climate-related risks. In other words: if extreme weather, new carbon taxes, or rapid technology shifts happen, can your business still adapt and succeed?

I will briefly explain the requirements for companies to disclose their resilience in relation to climate change.

More elaborate articles are available, which can be found below.

2. What does resilience mean here?

In plain terms, resilience means the ability to keep going, adapt and remain competitive even under tough climate conditions. For a company, this involves:

Testing how your strategy performs under different climate scenarios (e.g. 1.5°C vs high emissions).

Identifying where your business might be vulnerable.

Explaining how your current or planned actions and investments will help you adapt.

Being clear about uncertainties — no company has all the answers.

The ESRS defines climate resilience as follows:

“The capacity of an undertaking to adjust to climate changes, and to developments or uncertainties related to climate change. Climate resilience involves the capacity to manage climate-related Scope 1 and benefit from climate-related opportunities, including the ability to respond and adapt to transition risks and physical risks. An undertaking’s climate resilience includes both its strategic resilience and its operational resilience to climate-related changes, developments or uncertainties associated with climate change.”

3. ESRS E1-3 at a glance

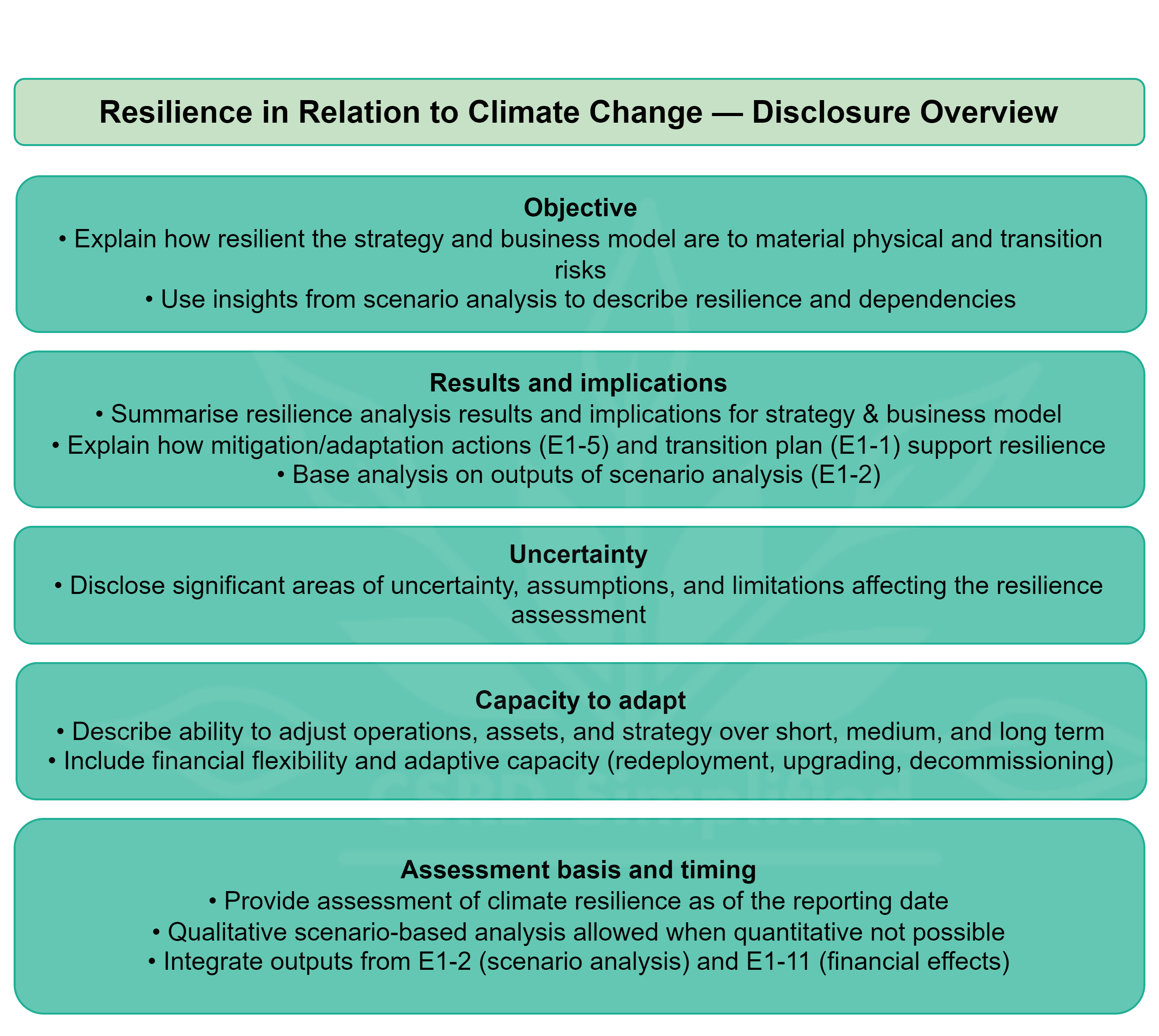

Under E1-3 you must disclose:

Coming soon!

E1-3: Resilience assessment with ISO 14091

4. How E1-3 links to the rest of ESRS E1

E1-2 (risks and scenarios) provides the input: which risks you face and under what scenarios.

E1-3 (resilience) explains how your business would cope with those risks.

E1-11 (financial effects) shows the expected impact in monetary terms.

Together, these disclosures tell the full story: what risks you face, how resilient you are, and what that means for your financial performance.

5. Bottom line

E1-3 asks companies to demonstrate that their climate strategy is stress-tested and adaptable. To do this well, focus on:

Being transparent about the outcomes of your resilience analysis.

Showing how your plans and investments strengthen resilience.

Admitting where there are uncertainties and how you plan to manage them.

Done right, this disclosure builds trust: it shows stakeholders that your business is ready to handle whatever climate change throws at it.