[EXPLAINED] E1-11: Anticipated Financial Effects

ESRS E1-11: Anticipated financial effects from material physical and transition risks and potential climate-related opportunities

1. Introduction

Climate change affects money.

E1-11 asks companies to show how climate-related risks and opportunities are expected to influence their finances over time.

This disclosure connects sustainability and finance. It helps investors understand how your assets, revenues, and costs might change as the world transitions to a low-carbon, climate-resilient economy.

I will briefly explain the requirements for companies to disclose their anticipated financial effects.

More elaborate articles are available, which can be found below.

2. What are climate-related financial effects?

In simple terms, these are the ways that climate change — and the response to it — can change what your company owns, earns, or spends.

They come from three main sources:

Physical risks: damage or disruption from floods, heatwaves, droughts, or storms.

Transition risks: financial losses caused by new climate laws, carbon pricing, shifting markets, or technological change.

Opportunities: new or growing markets for low-carbon products, energy efficiency, or adaptation solutions.

E1-11 asks you to identify the monetary size and share of assets and revenues affected by these factors, and to explain how you estimated them.

The ESRS defines anticipated financial effects as follows:

“Financial effects that do not meet the recognition criteria for inclusion in the financial statement line items in the reporting period and that are not captured by the current financial effects.”

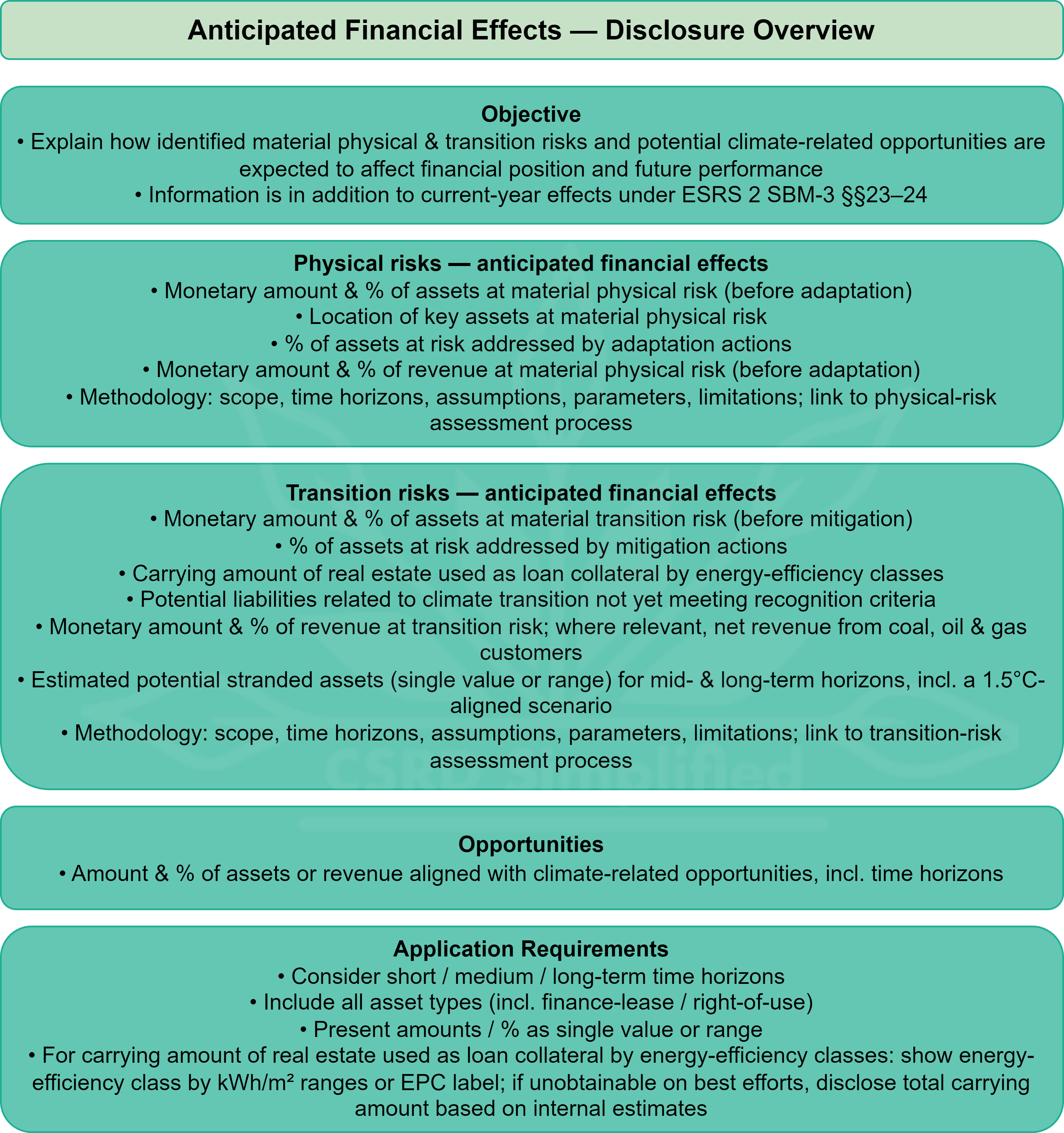

3. ESRS E1-11 at a glance

E1-11 requires you to disclose:

Read more about anticipated financial effects from material physical and transition risks and potential climate-related opportunities:

Coming soon!

4. How E1-11 links to the rest of ESRS E1

E1-2 and E1-3 identify and test the risks and resilience.

E1-5 to E1-6 show the actions and targets to reduce those risks.

E1-11 translates all of that into financial terms — what it means for your assets, revenues, and liabilities.

Together, these disclosures show the full picture: from climate risk to business impact to financial outcome.

5. Bottom line

E1-11 closes the loop between climate strategy and financial performance. To meet the requirement:

Quantify exposure — show which assets and revenues are at risk or in opportunity.

Explain your methods — timeframes, assumptions, and data sources.

Link to actions and transition plans — show how you’re managing those effects.

When done clearly, this disclosure demonstrates that your company understands how climate change shapes its financial future.