1. Introduction

Putting a price on carbon is one of the most powerful ways to make climate impact visible in everyday business decisions.

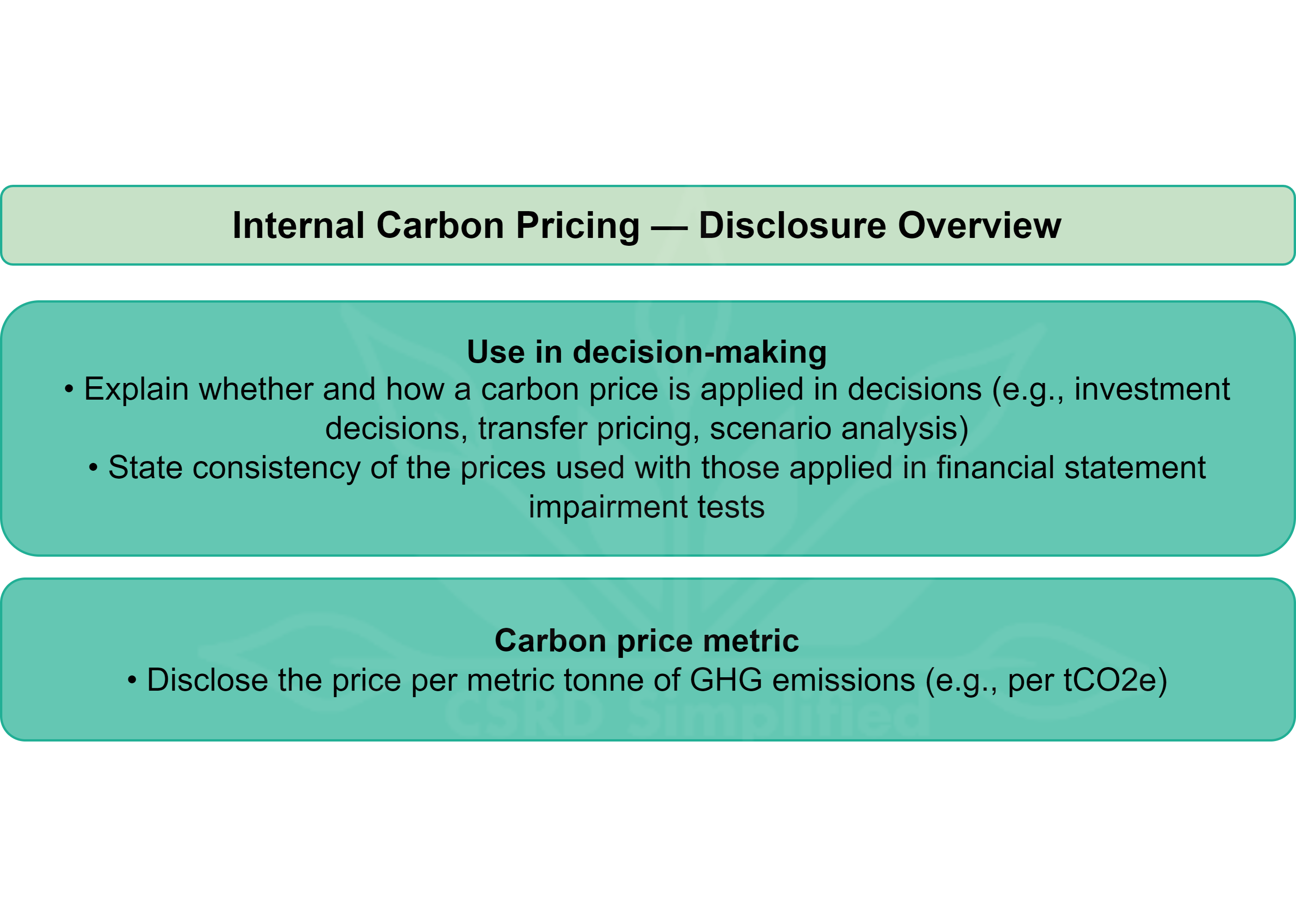

E1-10 asks companies to explain whether and how they apply a carbon price internally — that is, how they assign a financial value to their own greenhouse gas (GHG) emissions when making investment, planning, or risk decisions.

The goal is straightforward: to demonstrate to investors and stakeholders that your company understands the cost of carbon and is using it to inform smarter, lower-emission choices.

I will briefly explain the requirements for companies to disclose their internal carbon pricing.

More elaborate articles are available, which can be found below.

2. What is internal carbon pricing?

Internal carbon pricing (ICP) refers to treating carbon emissions as if they have a cost, even if no government tax or trading system is currently in place.

Companies can use different forms:

Shadow price: a hypothetical price per tonne of CO₂e used when evaluating investments.

Internal carbon fee: an actual payment charged to business units for their emissions.

Implicit price: the average cost your company already bears through existing carbon taxes or emissions trading schemes.

Example:

When choosing between two production lines, a company might add €100 per tonne of CO₂e as a “shadow cost.”

The option with lower emissions then shows a lower total lifetime cost — encouraging climate-friendly investment.

The ESRS defines an internal carbon price as follows:

“Price used by an undertaking to assess the financial implications of changes to investment, production, and consumption patterns, and of potential technological progress and future emissions abatement costs.”

3. ESRS E1-10 at a glance

E1-10 requires you to disclose:

Read more about how internal carbon pricing works here:

![[BREAKDOWN] E1-10: How does internal carbon pricing work?](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

4. How E1-10 links to the rest of ESRS E1

E1-8 (GHG emissions) gives you the quantity of emissions to which the price applies.

E1-5 (actions & resources) and E1-6 (targets) show how internal pricing influences where you invest.

E1-11 (financial effects) connects the carbon price to anticipated financial risks and opportunities.

Together, these disclosures show whether your financial decisions truly reflect the cost of carbon.

5. Bottom line

E1-10 turns climate strategy into economics. To comply and communicate clearly:

State whether you use internal carbon pricing — and if not, whether you plan to.

Disclose the price per tonne of CO₂e and how it’s applied.

Link it to decisions and financial impacts, not just policy statements.

Done well, internal carbon pricing shows that your company is preparing for a world where emitting greenhouse gases has a real and rising cost — and that you’re ready to compete in it.