EU CSRD and Omnibus Directive: Overview and 2025 updates

EU CSRD and Omnibus Directive: Overview and 2025 updates

1. Introduction

The Corporate Sustainability Reporting Directive (CSRD) is a major EU law (effective Jan 2023) that expands and modernises how companies report on environmental, social and governance (ESG) issues. It replaces the earlier Non-Financial Reporting Directive (NFRD) and requires large and listed companies to disclose reliable sustainability information so that investors, consumers and the public can assess corporate ESG performance. Companies in scope must use the EU’s new European Sustainability Reporting Standards (ESRS). The first reports under CSRD cover the 2024 financial year.

But in early 2025, the European Commission proposed changes to make CSRD simpler. These “Omnibus” proposals aim to ease the burden for smaller firms and refocus reporting on the biggest players.

This article will help you understand:

✅ What the Omnibus simplification package is

✅ Key 2025 developments, including the “Stop-the-Clock” delay

✅ What different company types need to do to prepare

✅ Practical next steps for compliance

By the end, you’ll have a clear picture of where EU sustainability reporting is headed and what your company can do to stay ahead.

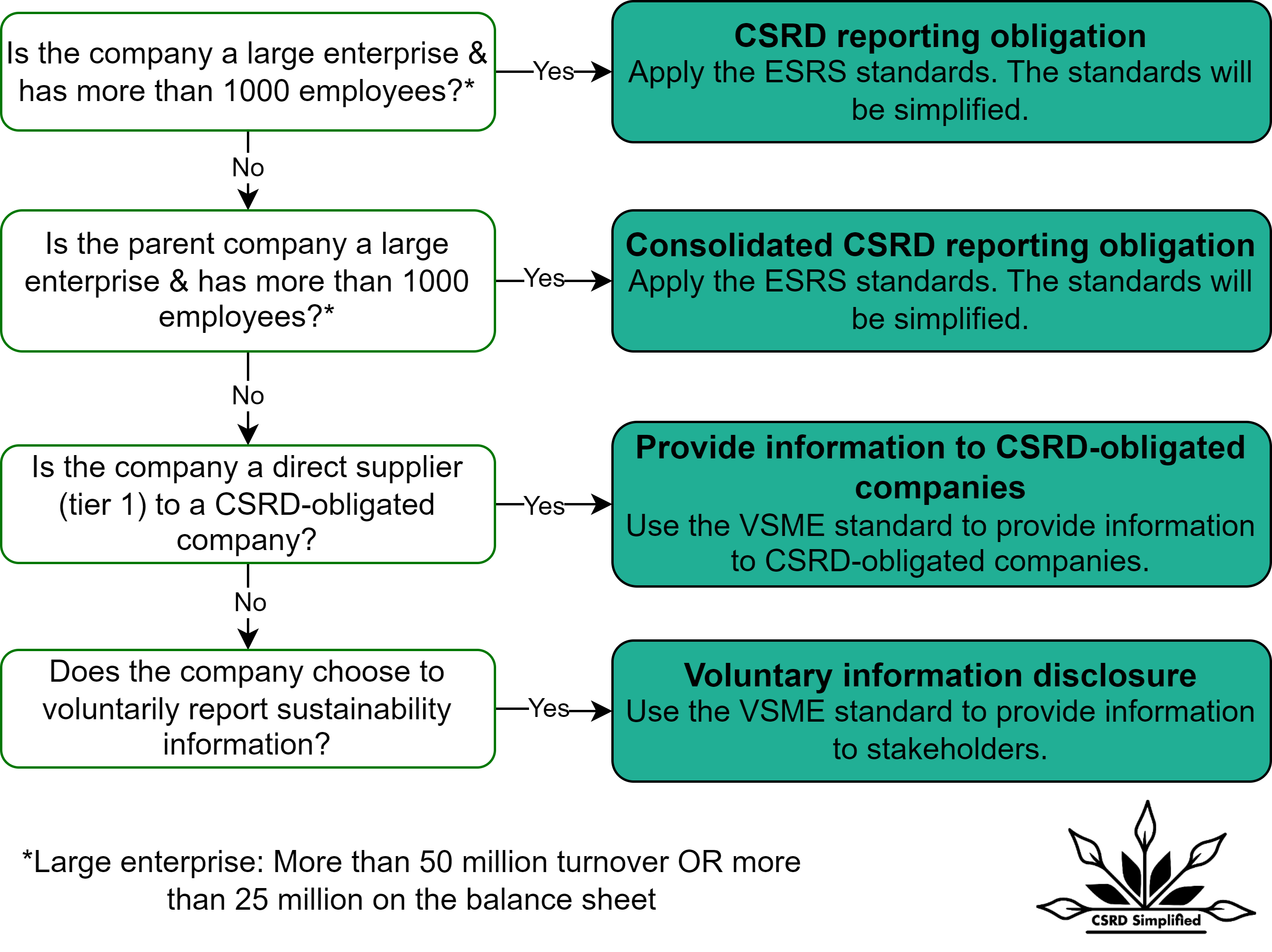

2. What is Omnibus?

The “Omnibus” Directive (package) refers to a set of simplification proposals introduced by the European Commission in February 2025 to amend CSRD and related rules. This Omnibus package (first proposed in Feb 2025) is intended to reduce red tape, focusing sustainability reporting obligations on the largest companies and easing burdens on smaller firms. It includes (Omnibus I) a draft directive amending CSRD, the Audit and Accounting Directives and the new Corporate Sustainability Due Diligence Directive (CSDDD), plus (Omnibus II) changes to sustainable finance rules and the EU Taxonomy.

In practice, the Omnibus proposals would raise thresholds (so only companies with >1,000 employees and either turnover >€50m or assets >€25m report), remove sector‑specific reporting standards, keep assurance at limited level, and introduce a voluntary SME reporting standard to shield smaller firms.

3. Key 2025 developments

Omnibus simplification proposals (Feb 2025):

On 26 Feb 2025 the Commission adopted an Omnibus package of proposals to simplify sustainability rules. Key intended changes include:

Scope narrowed: ~80% of companies would be removed from CSRD scope. Going forward, only very large firms (with >1,000 employees and high turnover/assets) would be mandated to report.

SME relief: A new voluntary reporting standard (based on the EFRAG SME standard) will be created for smaller companies. Large companies could only ask suppliers/SMEs (≤1,000 employees) for that limited information, reducing the “trickle-down” burden.

Simpler standards: Sector-specific ESRS would be scrapped and only the core standards retained, cutting down mandatory data points. The mandate to move from limited to reasonable assurance is removed, so auditors will continue to provide only limited assurance on CSRD reports.

Non-EU firms: For non-EU companies, the EU revenue threshold rises from €150m to €450m (aligning with CSDDD).

Value-chain cap: The existing cap on information requested from value-chain partners would explicitly cover all companies with ≤1,000 employees (not just SMEs).

Reporting delays: As a separate parallel measure, the Commission proposed postponing by two years the reporting obligations for many companies (see next section).

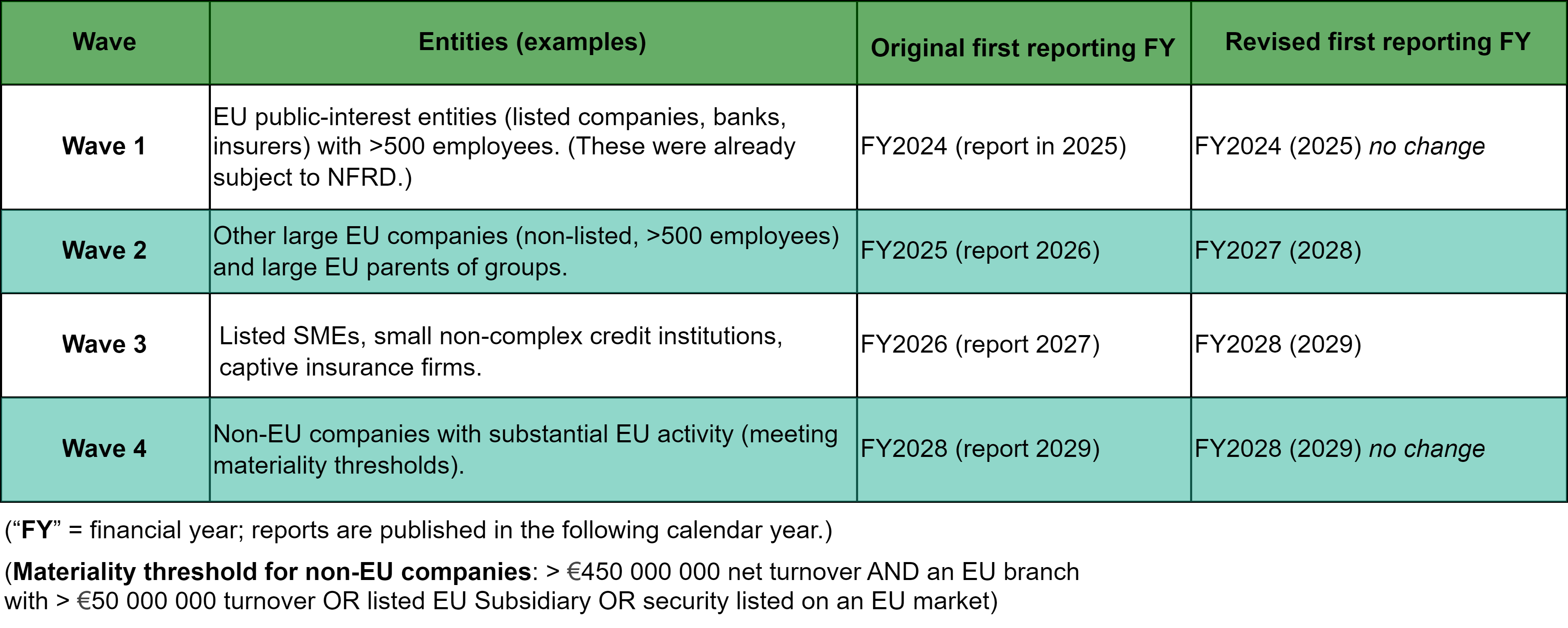

“Stop-the-Clock” Directive (Apr 2025): In early April 2025, the European Parliament and Council fast-tracked a directive to delay CSRD (and CSDDD) deadlines. This “stop-the-clock” measure shifts the application dates as follows:

Large companies (non-NFRD) originally due to report in 2026 (for FY2025) will instead report in 2028.

Listed SMEs and other small entities originally due in 2027 (for FY2026) will report in 2029.

(No change for first-wave NFRD companies or non-EU companies: they still report in 2025 and 2029 respectively.)

This gives legislators time to agree the Omnibus changes without forcing companies to start, stop and restart reporting. The directive was published in April 2025 and EU states must transpose it by end-2025.

Other Milestones:

2022–2023: CSRD was formally adopted on 14 Dec 2022 and entered into force 5 Jan 2023finance.ec.europa.eu. The first ESRS were adopted in late 2023, ready for use by companies reporting FY2024.

2025: Negotiations on the Omnibus proposals are underway. The Commission expects co-legislators to reach a rapid agreement on final rulesfinance.ec.europa.eu. According to EU leaders’ guidance, the aim is to finalise these simplifications by the end of 2025consilium.europa.eu.

4. Reporting implementation phases

CSRD rollout occurs in waves. Under the original rules, companies are grouped by size/type with staggered start dates. The stop-the-clock delays mean the revised timeline is:

The changes above come from the Omnibus proposals and final Stop-the-Clock directive. In practice, large companies in Waves 2 and 3 will begin reporting later than originally planned, giving them extra preparation time. Wave 1 and Wave 4 deadlines remain unchanged.

5. Implications by company size and industry

Very large companies: Those still in scope (typically global enterprises with >1,000 employees) should prepare robust ESG reporting processes. Even with simplifications, they must collect a broad range of data (climate, biodiversity, human rights, governance, etc.) and follow the ESRS framework. The move to limited assurance means audit costs stay predictable, but companies should gear up for mandatory external review of their disclosures.

Mid-sized groups: Companies on the cusp of the thresholds must check if they still qualify under the new tests (employees + turnover/assets). If they fall out of scope, they can opt into voluntary reporting using the EU SME standard to signal sustainability leadership. Those with listed securities should plan for Wave 3 timing.

Small and micro firms: Most will be exempt from CSRD. However, many small businesses have large customers in scope; these larger clients may require sustainability information (albeit limited by the value-chain cap). Small firms should therefore start basic ESG record-keeping and consider early adoption of simplified reporting practices to facilitate sales and finance relationships. Adopting the forthcoming EFRAG voluntary SME standard can prepare them for eventual downstream demands.

High-impact industries: Companies in pollution-intensive or high-risk sectors should invest early in robust sustainability strategies and metrics (energy use, emissions, waste, labor practices, etc.), as these will dominate reporting content. Even with lighter requirements, they must demonstrate concrete climate transition plans and compliance with EU Taxonomy rules.

Service and financial firms: These sectors often have complex value chains. Financial companies (banks, insurers, asset managers) will not only report their own ESG impacts but also enforce due diligence on clients’ sustainability (per CSDDD). Service companies should emphasize social governance practices, diversity policies and digital governance in their reports.

6. What’s next?

Here are some practical steps for CSRD compliance:

Check if you’re in scope

See if your company meets Omnibus thresholds (staff, turnover, assets) or is a listed SME or non-EU company affected.Do a gap analysis

Compare your current ESG data and practices with CSRD (ESRS) requirements. Identify what’s missing.Set up internal processes

Appoint a sustainability lead and start integrating ESG data into your operations. Start early: even with delayed deadlines, the first report may come in 2028.Use existing frameworks

Align current disclosures (e.g. GRI, CDP, IFRS S1/S2) with ESRS. This helps ease the transition.Consider voluntary reporting

If you’re not in scope but in someone’s value chain, look at the upcoming SME standard. It helps meet partner demands without too much burden.Invest in data systems

Implement or upgrade IT systems (ESG reporting software or modules) to track environmental and social data (energy use, emissions, HR stats, etc.). Automating data flows now will pay off when official reporting begins.Plan for assurance

Even “limited” assurance needs preparation. Early discussions with auditors can clarify the depth of the audit needed and help refine reporting quality.Train and communicate

Make sure your teams understand CSRD. Talk to suppliers and customers about what data you’ll need from them.Stay updated

The Omnibus proposals are not final law yet. Companies should watch final EU legislation (likely by late 2025) and any delegated acts (e.g. the detailed ESRS revisions). Stay informed with guidance from the European Commission, EFRAG, and industry groups for practical tips.Use Available Support

Use resources from EU and national authorities. For example, the EC’s Q&A on Omnibus and official guidelines (when published) will clarify details. Joining industry networks or working groups can provide peer insights on implementation challenges and solutions.

Relevant Sources

Omnibus simplification proposals and related press materials: