ESRS: What is the SFDR and to whom does it apply?

ESRS: What is the SFDR and to whom does it apply?

1. Introduction

The EU’s Sustainable Finance Disclosure Regulation, commonly referred to as the SFDR, is a major step in aligning financial markets with sustainability goals. Introduced by Regulation (EU) 2019/2088, the SFDR imposes new transparency requirements on the financial sector. Its main objective is to provide clear, consistent information on how financial institutions incorporate sustainability into their investment decisions and advice.

Let's dive into what the SFDR entails, who it applies to, and how it relates to the CSRD.

2. What is the SFDR?

The SFDR is a European Union regulation that mandates financial institutions to disclose how they handle sustainability risks, adverse impacts on sustainability, and sustainable investment goals. These disclosures are intended to enhance transparency for investors, ensuring they have the information needed to make environmentally and socially informed choices.

In simple terms, the SFDR requires that financial firms reveal the environmental, social, and governance (ESG) factors they consider when making investment decisions or advising clients. By standardizing this information, the SFDR helps investors to assess and compare the sustainability of different financial products and services across the EU.

Full compliance, including periodic disclosures and additional technical reporting standards, became mandatory by the end of 2022.

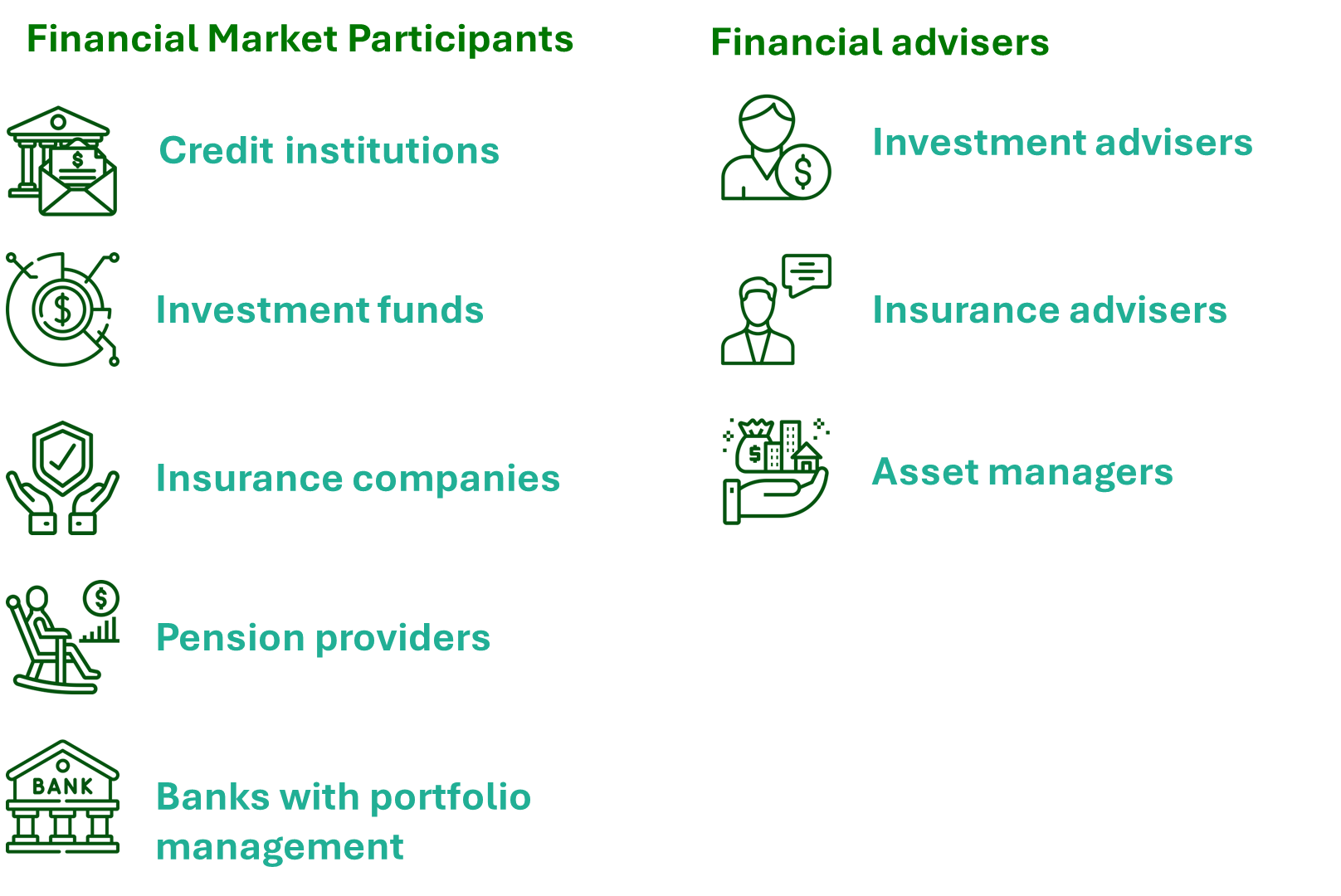

3. Who Needs to Comply with the SFDR?

The SFDR applies to a wide range of financial entities, including:

These entities must evaluate how sustainability factors impact their investment processes and disclose relevant information about their sustainability approaches on their websites, in pre-contractual information, and in periodic reports.

4. Key SFDR Requirements

The SFDR’s requirements focus on three primary areas:

1. Transparency of sustainability risks

Financial institutions must disclose how they integrate sustainability risks—like environmental, social, or governance issues that could impact an investment’s financial performance—into their decision-making and advisory processes. For example, a portfolio manager should explain whether or not they consider risks related to climate change when selecting investments, along with any potential impacts on returns.

2. Consideration of adverse sustainability impacts

Institutions also need to disclose if, and how, they consider the principal adverse impacts of their investments on sustainability factors, such as carbon emissions, water use, or human rights. Larger companies with more than 500 employees are specifically required to consider and report on these adverse impacts, while smaller entities can choose whether to do so.

3. Transparency of sustainable investment objectives

For products marketed as “sustainable” or that promote specific ESG characteristics, financial firms must provide detailed information on these goals and how they plan to achieve them. For instance, a fund with a goal to reduce carbon emissions must disclose how this goal is measured, including details about benchmarks or indices used.

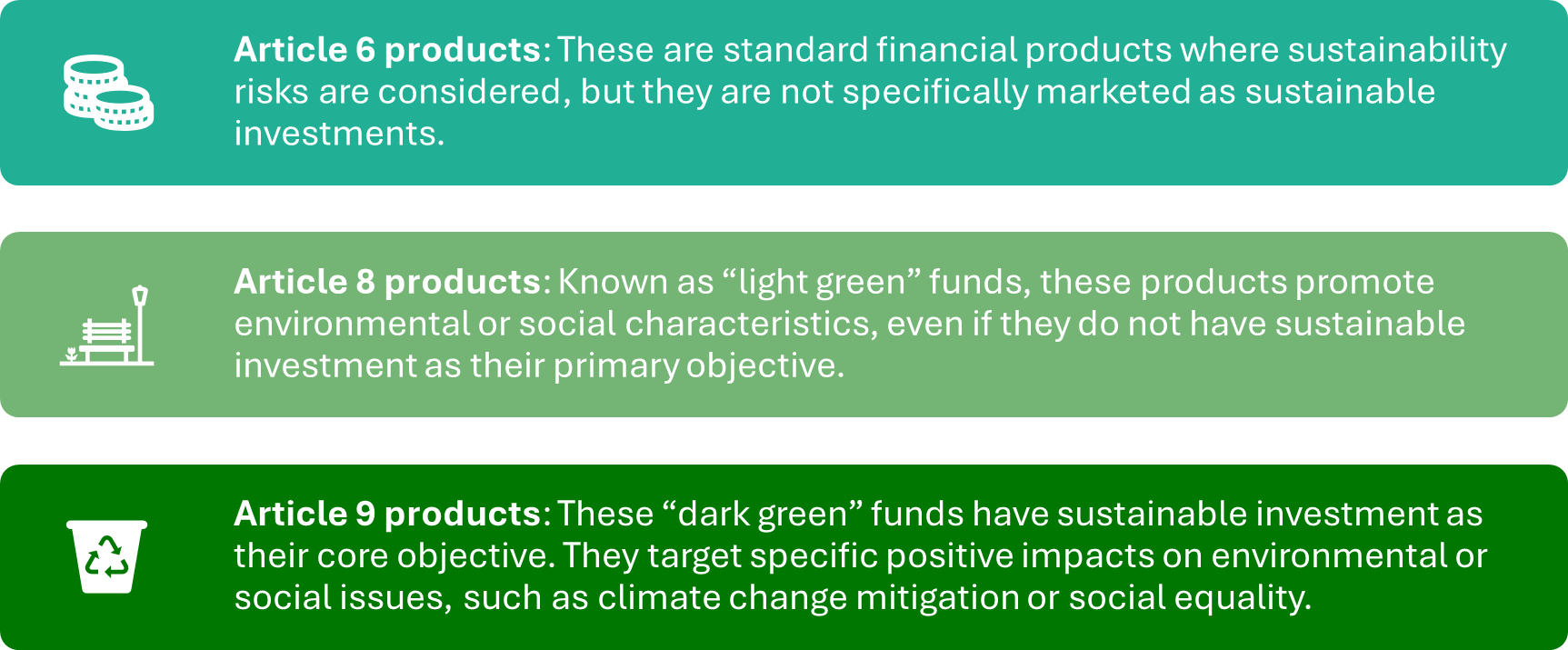

5. Classification of Financial Products under the SFDR

The SFDR introduces three categories for financial products:

For financial products with Article 8 or 9 designations, annual reporting must demonstrate the actual outcomes of their sustainability initiatives, comparing these to any benchmarks used.

6. How the SFDR and CSRD Work Together to Drive Sustainable Finance

While the SFDR primarily focuses on the financial sector's disclosure requirements, the CSRD sets out corporate reporting obligations for large companies. Together, they help create a holistic framework for sustainability information.

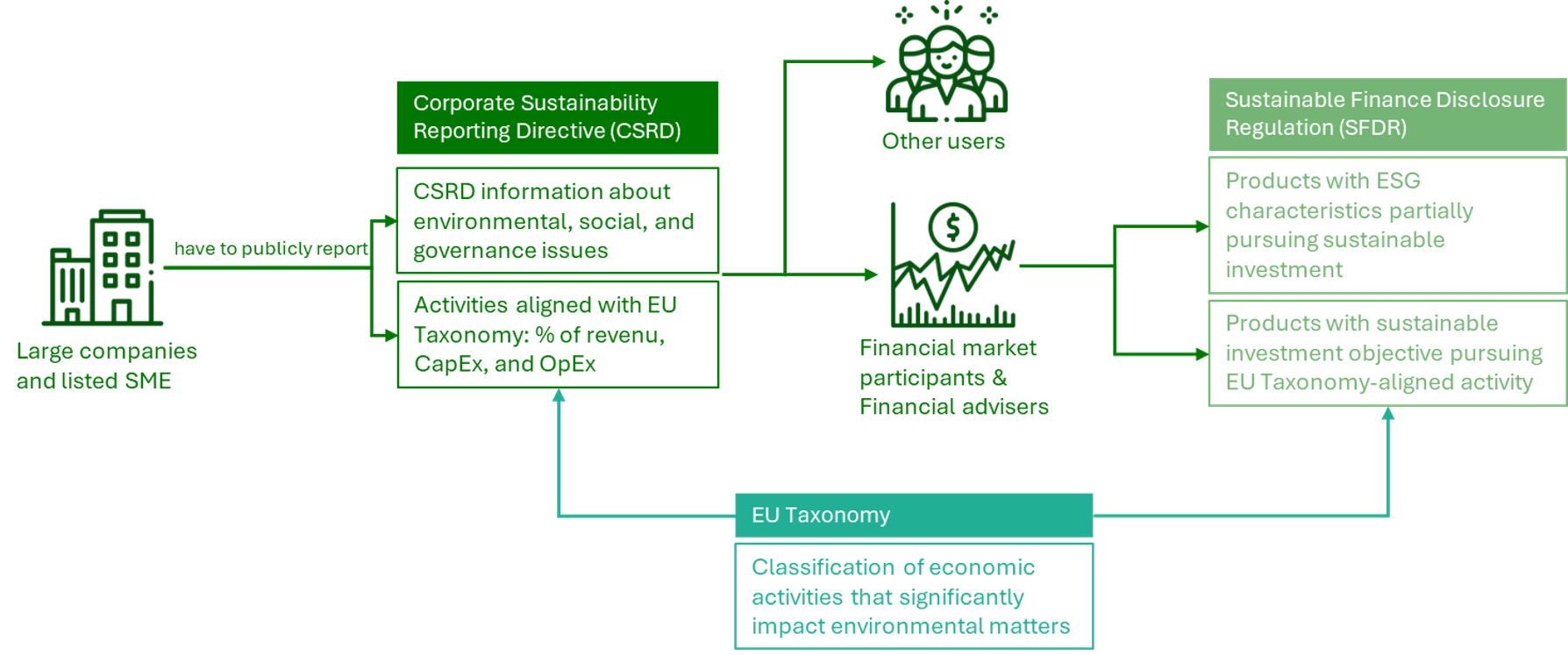

The CSRD is essential to the SFDR because it provides critical sustainability data that financial market participants need for their SFDR reporting. Companies affected by the CSRD—mainly large and listed companies in the EU—are required to report specific ESG metrics, including greenhouse gas emissions, water usage, waste production, and more. Financial institutions, in turn, use this information to fulfill their SFDR obligations by assessing the sustainability risks and performance of their investments.

SFDR compliance needs CSRD data: SFDR requires financial institutions to report on how their products align with sustainability factors and the EU Taxonomy. The CSRD’s disclosures give financial institutions access to standardized ESG data, enabling them to assess and report on sustainability risks, adverse impacts, and ESG alignment.

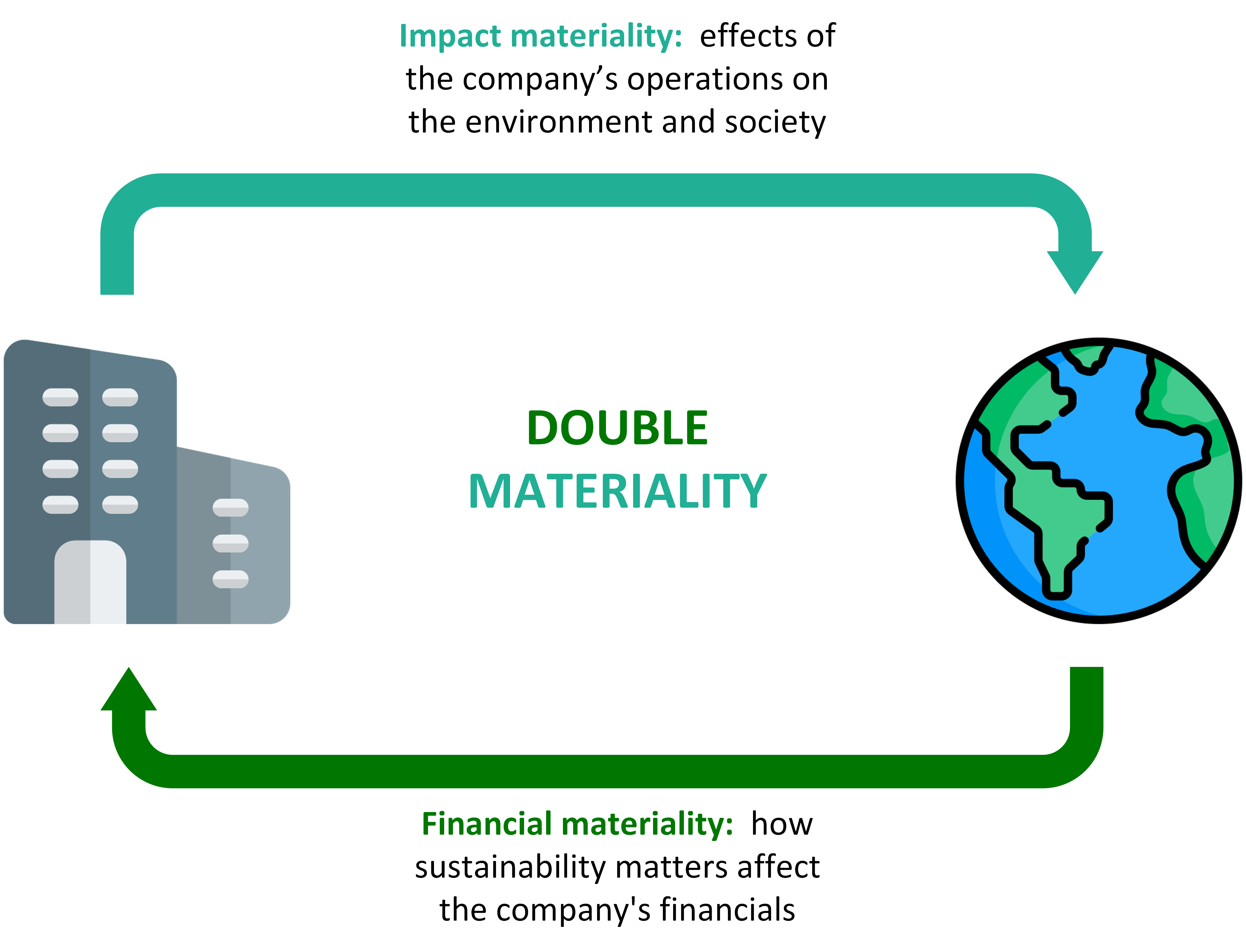

Double materiality in the CSRD: Not all SFDR data points are mandatory under the CSRD. Therefore, the CSRD introduces the concept of double materiality, requiring companies to report on ESG topics that are material to them. It covers how sustainability affects their financial performance and also their impacts on the environment and society. This broader perspective aligns with the SFDR’s objective of giving investors a comprehensive view of both sustainability risks and opportunities associated with their investments.

Both the SFDR and CSRD rely on the EU Taxonomy, a classification system that identifies environmentally sustainable activities, as their foundation for ESG reporting:

The EU Taxonomy: Defines economic activities that can be considered sustainable based on criteria like climate change mitigation, adaptation, and environmental objectives. More information about the EU Taxonomy can be found here.

The CSRD: Requires companies to disclose their performance based on Taxonomy-aligned metrics, which gives financial institutions a reliable benchmark for evaluating ESG alignment.

The SFDR: Obligates financial market participants to disclose how their products promote sustainability, using the EU Taxonomy as a reference for evaluating environmental alignment.

Together, these regulations create a transparent system where companies report their sustainability metrics (CSRD), and financial institutions disclose how these metrics impact their investment products (SFDR).

7. Conclusion

The SFDR requires financial market participants to disclose the sustainability impacts of their products, while the CSRD facilitates this process by providing companies with a standardized framework to report the necessary data.

By mandating transparency on both corporate and investment levels, these regulations reduce “greenwashing” risks, ensure consistent reporting, and support the EU’s overarching objective of directing capital toward sustainable activities. While still in the early stages of implementation, this integrated approach is set to shape sustainable finance in the EU, giving investors and companies the tools and information to make impactful, sustainability-focused decisions.

Relevant Sources

Key links between CSRD and SFDR

Relationships between CSRD, EU Taxonomy and SFDR