1. Introduction

Companies must disclose environmental, social, and governance (ESG) impacts. However, not every ESG topic is relevant for each company. To identify relevant ESG topics a company can perform a materiality assessment. Materiality assessment is the process through which a company determines which sustainability topics are most significant to its operations and stakeholders. These significant topics, are the ones that the company needs to report on.

This article aims to explain what a materiality assessment is. How a company can perform a materiality assessment will be covered in another article.

2. Materiality Assessment

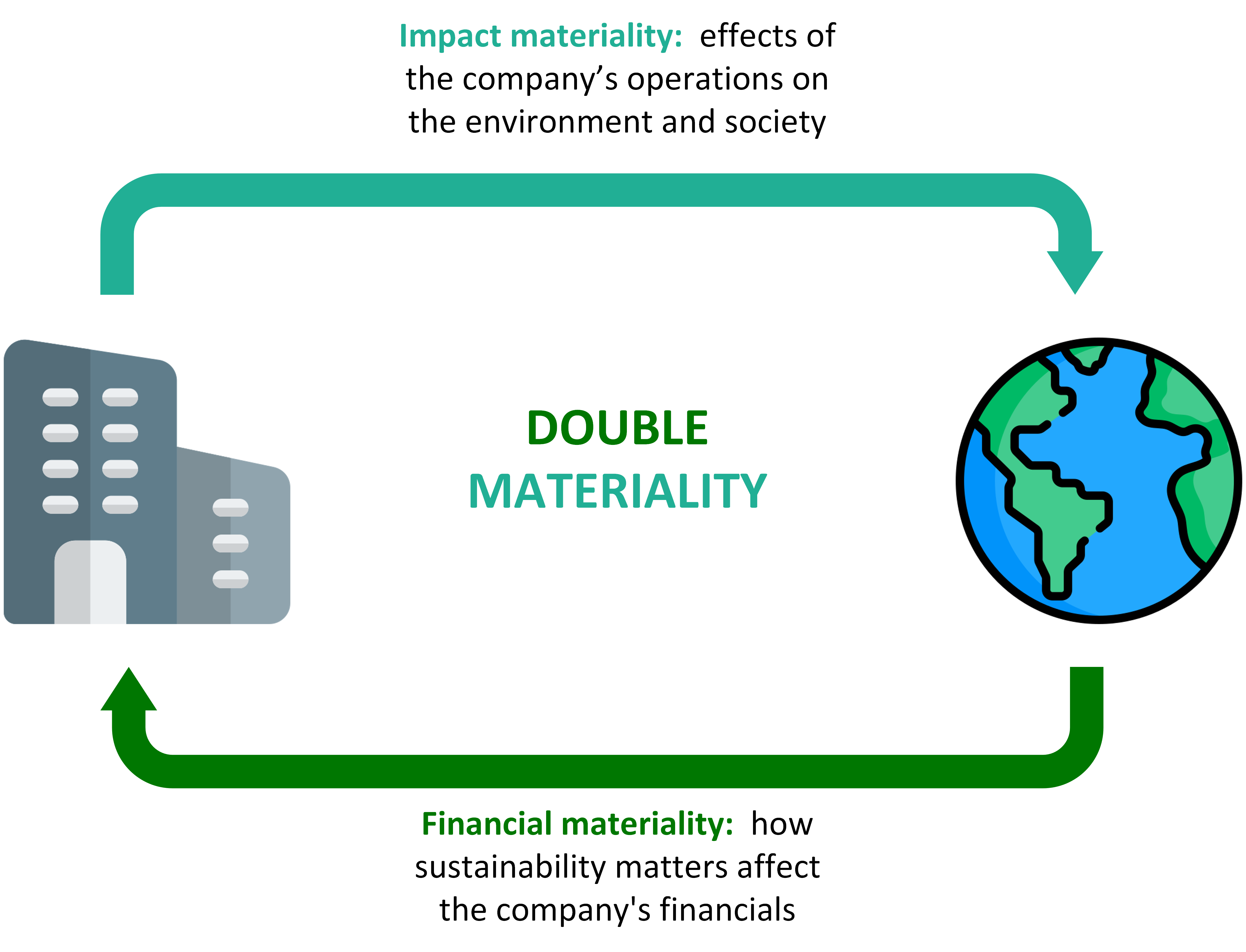

The ESRS approach to materiality is rooted in the concept of double materiality. Double materiality requires companies to report not only on how external factors impact their business, but also how their business activities impact the environment and society:

Impact materiality

This looks at how a company's operations affect people and the environment. When assessing the materiality of an impact, one should consider its severity and likelihood. The severity of the impact is based on the scale, scope, and remediability:

Scale: This indicates how serious the impact is, considering how it affects fundamental needs and rights such as access to education, livelihood, or basic life necessities. For example, the pollution caused by a multinational corporation contributing to global pollution is much more severe compared to the pollution from a small local company affecting only its immediate surroundings.

Scope: This indicates the extent of the impact, particularly the number of individuals affected or the extent of environmental damage. For instance, assessing how a company’s waste management practices affect local communities, wildlife, and the broader ecosystem gives a clear picture of the scope of the impact.

Remediability: This assesses whether the impact can be undone or mitigated. Irremediable impacts are those that cause lasting or irreversible harm. For example: Permanent loss of biodiversity due to deforestation versus temporary air pollution that can be reduced through cleaner technologies.

To decide what should be considered, a distinction is made between actual and potential impacts and between positive and negative impacts.

Actual positive impact: scale and scope.

Potential positive impact: scale, scope, and likelihood.

Actual negative impact: scale, scope, remediability.

Potential negative impact: scale, scope, remediability, and likelhood.

Financial materiality

This perspective focuses on how ESG issues affect the company's financial health, including performance, cash flow, and access to capital. It’s of particular interest to investors, lenders, and suppliers. It includes both risks and opportunities. Risks affect the company negatively, while opportunities affect the company positively.

Key aspects of financial materiality include:

Financial performance: This looks at how sustainability matters impact the company’s revenues, expenses, and profitability. For example: A company’s reputation for sustainable practices could boost sales and customer loyalty, while failure to comply with environmental regulations could result in fines and increased operational costs.

Financial position: This involves the company’s assets, liabilities, and equity. Sustainability factors can affect the valuation of these elements. For example: Environmental liabilities due to contamination requiring cleanup could decrease the value of a company's assets.

Cash flows: This perspective examines how sustainability issues affect the company's inflow and outflow of cash, which is critical for maintaining operations. For example: Investments in energy-efficient technologies may initially increase capital expenditures but lead to long-term savings and positive cash flows.

Access to finance: This looks at the company’s ability to secure funding and the cost of capital. Companies with robust sustainability practices may find it easier to attract investors and secure loans at favorable rates. For example: Banks and investors increasingly favor companies with strong ESG credentials, potentially reducing the cost of capital for such firms.

Scale of financial materiality

The scale of financial materiality can be assessed by looking at the magnitude and likelihood:

Magnitude refers to how big the financial effects of an ESG issue could be on a company. This can be measured in terms of money and considered over different time frames:

Short-term: What impact will this issue have on the company's finances in the near future (e.g., the next year)?

Medium-term: What financial effects will it have in the somewhat distant future (e.g., the next 2-5 years)?

Long-term: How will this issue affect the company's financial situation far into the future (e.g., beyond 5 years)?

Likelihood is about the chances that an ESG issue will actually lead to financial effects. It's the probability that a risk or an opportunity will happen within a certain time frame.

If the likelihood is high, it means there’s a strong chance that the financial effect will occur.

If the likelihood is low, it means there’s a smaller chance that the financial effect will happen.

For example, if a company operates in a flood-prone area, the likelihood would assess how probable it is that flooding will cause financial damage to the company within the next few years.

3. Requirements

Performing a materiality assessment involves among others these important requirements:

Inclusion of entire value chain: Companies must consider their entire value chain, including both upstream (suppliers) and downstream (customers) impacts.

Stakeholder engagement: Engaging with affected stakeholders is important to understand the significance of various sustainability matters. This engagement helps discover the materiality of impacts from the perspective of those affected.

Structured process: While the ESRS does not mandate a specific process, companies are expected to follow a structured approach that reflects their unique circumstances.

Documentation: Companies must disclose the processes used to identify and assess material topics.

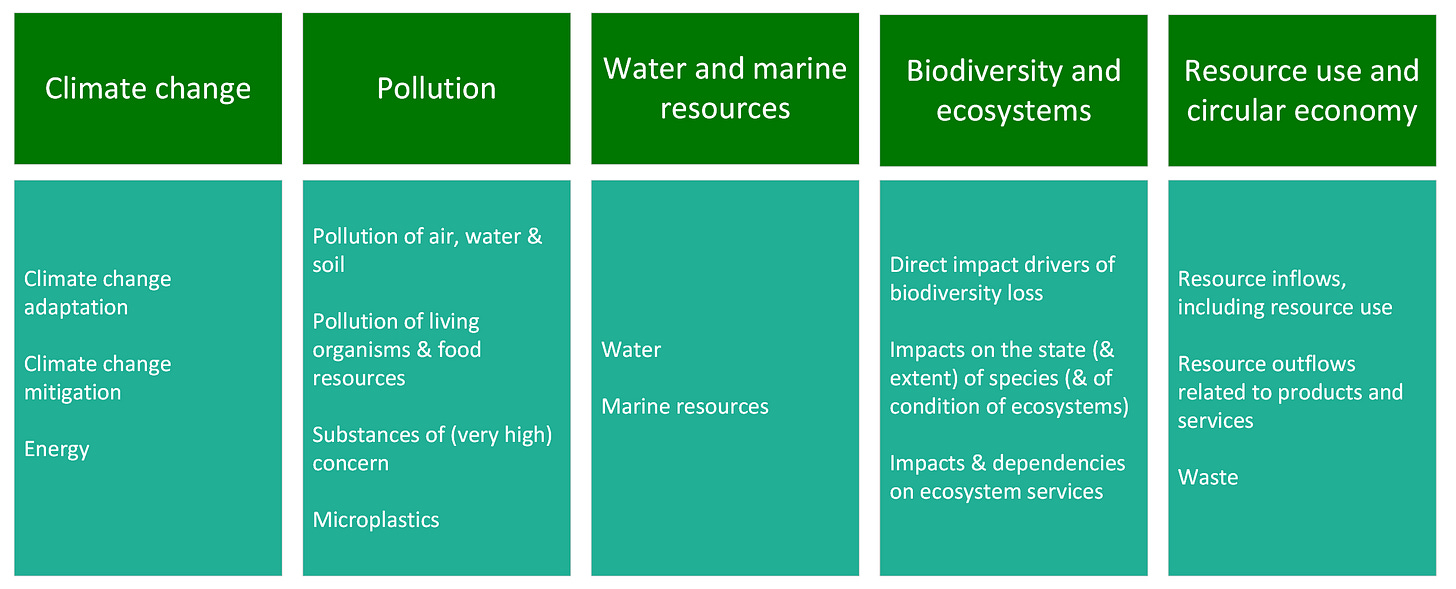

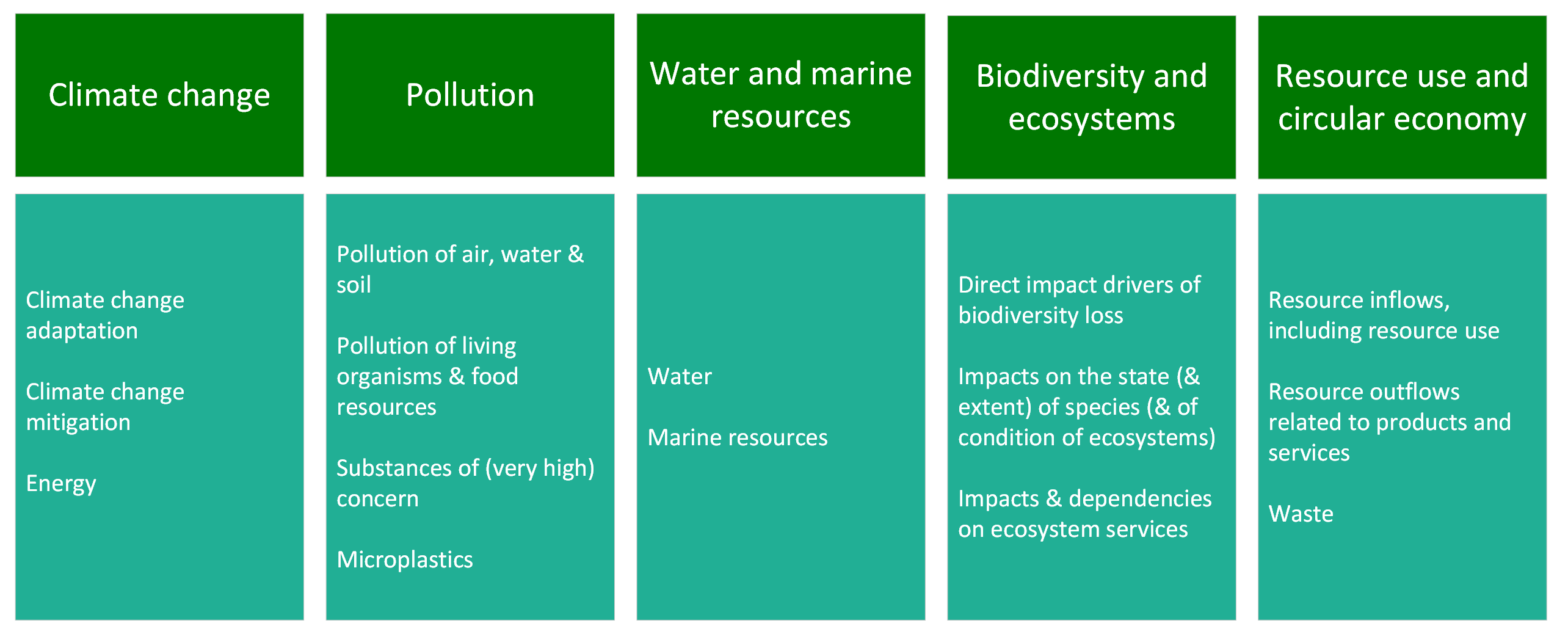

Topics: Companies must at least consider all the topics presented in ESRS 1, which are more than 90 (including the sub-sub-topics as they are called in ESRS 1). For example, there are 5 environmental topics, these topics include sub-topics (i.e. climate change adaptation, climate change mitigation, and energy). Meanwhile, sub-topics can have their own sub-topics, the so-called sub-sub-topics.

4. Conclusion

Making a value chain is followed by performing a materiality assessment. A materiality assessment is essential to ensure that companies provide meaningful sustainability information. By understanding what is required and following a structured approach, companies can effectively identify and report on the ESG topics that are relevant to them.

In an upcoming article, we will explore how companies can perform a materiality assessment. Subscribe to stay updated.

Relevant Standards

EFRAG IG 1: Materiality Assessment Implementation Guidance

ESRS 1

3. Double materiality as the basis for sustainability disclosures

21. The undertaking shall report on sustainability matters based on the double materiality principle as defined and explained in this chapter.

3.1 Stakeholders and their relevance to the materiality assessment process

22. Stakeholders are those who can affect or be affected by the undertaking. There are two main groups of stakeholders:

(a) affected stakeholders: individuals or groups whose interests are affected or could be affected – positively or negatively – by the undertaking’s activities and its direct and indirect business relationships across its value chain; and

(b) users of sustainability statements: primary users of general-purpose financial reporting (existing and potential investors, lenders and other creditors, including asset managers, credit institutions, insurance undertakings), and other users of sustainability statements, including the undertaking’s business partners, trade unions and social partners, civil society and non-governmental organisations, governments, analysts and academics.

23. Some, but not all, stakeholders may belong to both groups referred to in paragraph 22.

24. Engagement with affected stakeholders is central to the undertaking’s on-going due diligence process (see chapter 4 Due diligence) and sustainability materiality assessment. This includes its processes to identify and assess actual and potential negative impacts, which then inform the assessment process to identify the material impacts for the purposes of sustainability reporting (see section 3.4 of this Standard).

3.2 Material matters and materiality of information

25. Performing a materiality assessment (see sections 3.4 Impact materiality and 3.5 Financial materiality) is necessary for the undertaking to identify the material impacts, risks and opportunities to be reported.

26. Materiality assessment is the starting point for sustainability reporting under ESRS. IRO-1 in section 4.1 of ESRS 2, includes general disclosure requirements about the undertaking’s process to identify impacts, risks and opportunities and assess their materiality. SBM-3 of ESRS 2 provides general disclosure requirements on the material impacts, risks and opportunities resulting from the undertaking’s materiality assessment.

27. The Application Requirements in Appendix A of this Standard include a list of sustainability matters covered in topical ESRS, categorised by topics, sub-topics and sub-sub-topics, to support the materiality assessment. Appendix E Flowchart for determining disclosures to be included of this Standard provides an illustration of the materiality assessment described in this section.

28. A sustainability matter is “material” when it meets the criteria defined for impact materiality (see section 3.4 of this Standard) or financial materiality (see section 3.5 of this Standard), or both.

29. Irrespective of the outcome of its materiality assessment, the undertaking shall always disclose the information required by: ESRS 2 General Disclosures (i.e. all the Disclosure Requirements and data points specified in ESRS 2) and the Disclosure Requirements 6 (including their datapoints) in topical ESRS related to the Disclosure Requirement IRO-1 Description of the process to identify and assess material impacts, risks and opportunities, as listed in ESRS 2 Appendix C Disclosure/Application Requirements in topical ESRS that are applicable jointly with ESRS 2 General Disclosures.

30. When the undertaking concludes that a sustainability matter is material as a result of its materiality assessment, on which ESRS 2 IRO-1, IRO-2 and SBM-3 set disclosure requirements, it shall:

(a) disclose information according to the Disclosure Requirements (including Application Requirements) related to that specific sustainability matter in the corresponding topical and sector-specific ESRS; and

(b) disclose additional entity-specific disclosures (see paragraph 11 and AR 1 to AR 5 of this Standard) when the material sustainability matter is not covered by an ESRS or is covered with insufficient granularity.

31. The applicable information prescribed within a Disclosure Requirement, including its datapoints, or an entity-specific disclosure, shall be disclosed when the undertaking assesses, as part of its assessment of material information, that the information is relevant from one or more of the following perspectives:

(a) the significance of the information in relation to the matter it purports to depict or explain; or

(b) the capacity of such information to meet the users’ decision-making needs, including the needs of primary users of general-purpose financial reporting described in paragraph 48 and/or the needs of users whose principal interest is in information about the undertaking’s impacts.

32. If the undertaking concludes that climate change is not material and therefore omits all disclosure requirements in ESRS E1 Climate change, it shall disclose a detailed explanation of the conclusions of its materiality assessment with regard to climate change (see ESRS 2 IRO-2 Disclosure Requirements in ESRS covered by the undertaking’s sustainability statement), including a forward-looking analysis of the conditions that could lead the undertaking to conclude that climate change is material in the future. If the undertaking concludes that a topic other than climate change is not material and therefore it omits all the Disclosure Requirements in the corresponding topical ESRS, it may briefly explain the conclusions of its materiality assessment for that topic.

33. When disclosing information on policies, actions and targets in relation to a sustainability matter that has been assessed to be material, the undertaking shall include the information prescribed by all the Disclosure Requirements and datapoints in the topical and sector-specific ESRS related to that matter and in the corresponding Minimum Disclosure Requirement on policies, actions, and targets required under ESRS 2. If the undertaking cannot disclose the information prescribed by either the Disclosure Requirements and datapoints in the topical or sector-specific ESRS, or the Minimum Disclosure Requirements in ESRS 2 on policies, actions and targets, because it has not adopted the respective policies, implemented the respective actions or set the respective targets, it shall disclose this to be the case and it may report a timeframe in which it aims to have these in place.

34. When disclosing information on metrics for a material sustainability matter according to the Metrics and Targets section of the relevant topical ESRS, the undertaking:

(a) shall include the information prescribed by a Disclosure Requirement if it assesses such information to be material; and

(b) may omit the information prescribed by a datapoint of a Disclosure Requirement if it assesses such information to be not material and concludes that such information is not needed to meet the objective of the Disclosure Requirement.

35. If the undertaking omits the information prescribed by a datapoint that derives from other EU legislation listed in Appendix B of ESRS 2, it shall explicitly state that the information in question is “not material”.

36. The undertaking shall establish how it applies criteria, including appropriate thresholds, to determine:

(a) the information it discloses on metrics for a material sustainability matter according to the Metrics and Targets section of the relevant topical ESRS, in accordance with paragraph 34; and

(b) the information to be disclosed as entity-specific disclosures.

3.3 Double materiality

37. Double materiality has two dimensions, namely: impact materiality and financial materiality. Unless specified otherwise, the terms “material” and “materiality” are used throughout ESRS to refer to double materiality.

38. Impact materiality and financial materiality assessments are inter-related and the interdependencies between these two dimensions shall be considered. In general, the starting point is the assessment of impacts, although there may also be material risks and opportunities that are not related to the undertaking’s impacts. A sustainability impact may be financially material from inception or become financially material, when it could reasonably be expected to affect the undertaking’s financial position, financial performance, cash flows, its access to finance or cost of capital over the short-, medium- or long-term. Impacts are captured by the impact materiality perspective irrespective of whether or not they are financially material.

39. In identifying and assessing the impacts, risks and opportunities in the undertaking’s value chain to determine their materiality, the undertaking shall focus on areas where impacts, risks and opportunities are deemed likely to arise, based on the nature of the activities, business relationships, geographies or other factors concerned.

40. The undertaking shall consider how it is affected by its dependencies on the availability of natural, human and social resources at appropriate prices and quality, irrespective of its potential impacts on those resources.

41. An undertaking’s principal impacts, risks and opportunities are understood to be the same as the material impacts, risks and opportunities identified under the double materiality principle and therefore reported on in its sustainability statement.

42. The undertaking shall apply the criteria set under sections 3.4 and 3.5 in this Standard, using appropriate quantitative and/or qualitative thresholds. Appropriate thresholds are necessary to determine which impacts, risks and opportunities are identified and addressed by the undertaking as material and to determine which sustainability matters are material for reporting purposes. Some existing standards and frameworks use the term "most significant impacts” when referring to the threshold used to identify the impacts that are described in ESRS as "material impacts."

3.4 Impact materiality

43. A sustainability matter is material from an impact perspective when it pertains to the undertaking’s material actual or potential, positive or negative impacts on people or the environment over the short-, medium- or long-term. Impacts include those connected with the undertaking’s own operations and upstream and downstream value chain, including through its products and services, as well as through its business relationships. Business relationships include those in the undertaking’s upstream and downstream value chain and are not limited to direct contractual relationships.

44. In this context, impacts on people or the environment include impacts in relation to environmental, social and governance matters.

45. The materiality assessment of a negative impact is informed by the due diligence process defined in the international instruments of the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises. For actual negative impacts, materiality is based on the severity of the impact, while for potential negative impacts it is based on the severity and likelihood of the impact. Severity is based on the following factors:

(a) the scale;

(b) scope; and

(c) irremediable character of the impact.

In the case of a potential negative human rights impact, the severity of the impact takes precedence over its likelihood.

46. For positive impacts, materiality is based on:

(a) the scale and scope of the impact for actual impacts; and

(b) the scale, scope and likelihood of the impact for potential impacts.

3.5 Financial materiality

47. The scope of financial materiality for sustainability reporting is an expansion of the scope of materiality used in the process of determining which information should be included in the undertaking’s financial statements.

48. The financial materiality assessment corresponds to the identification of information that is considered material for primary users of general-purpose financial reports in making decisions relating to providing resources to the entity. In particular, information is considered material for primary users of general-purpose financial reports if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that they make on the basis of the undertaking’s sustainability statement.

49. A sustainability matter is material from a financial perspective if it triggers or could reasonably be expected to trigger material financial effects on the undertaking. This is the case when a sustainability matter generates risks or opportunities that have a material influence, or could reasonably be expected to have a material influence, on the undertaking’s development, financial position, financial performance, cash flows, access to finance or cost of capital over the short-, medium- or long-term. Risks and opportunities may derive from past events or future events. The financial materiality of a sustainability matter is not constrained to matters that are within the control of the undertaking but includes information on material risks and opportunities attributable to business relationships beyond the scope of consolidation used in the preparation of financial statements.

50. Dependencies on natural, human and social resources can be sources of financial risks or opportunities. Dependencies may trigger effects in two possible ways:

(a) they may influence the undertaking’s ability to continue to use or obtain the resources needed in its business processes, as well as the quality and pricing of those resources; and

(b) they may affect the undertaking’s ability to rely on relationships needed in its business processes on acceptable terms.

51. The materiality of risks and opportunities is assessed based on a combination of the likelihood of occurrence and the potential magnitude of the financial effects.

3.6 Material impacts or risks arising from actions to address sustainability matters

52. The undertaking’s materiality assessment may lead to the identification of situations in which its actions to address certain impacts or risks, or to benefit from certain opportunities in relation to a sustainability matter, might have material negative impacts or cause material risks in relation to one or more other sustainability matters. For example:

(a) an action plan to decarbonise production that involves abandoning certain products might have material negative impacts on the undertaking’s own workforce and result in material risks due to redundancy payments; or

(b) an action plan of an automotive supplier to focus on the supply of e-vehicles might lead to stranded assets for the production of supply parts for conventional vehicles.

53. In such situations, the undertaking shall:

(a) disclose the existence of material negative impacts or material risks together with the actions that generate them, with a cross-reference to the topic to which the impacts or risks relate; and

(b) provide a description of how the material negative impacts or material risks are addressed under the topic to which they relate.

3.7 Level of disaggregation

54. When needed for a proper understanding of its material impacts, risks and opportunities, the undertaking shall disaggregate the reported information:

(a) by country, when there are significant variations of material impacts, risks and opportunities across countries and when presenting the information at a higher level of aggregation would obscure material information about impacts, risks or opportunities; or

(b) by significant site or by significant asset, when material impacts, risks and opportunities are highly dependent on a specific location or asset.

55. When defining the appropriate level of disaggregation for reporting, the undertaking shall consider the disaggregation adopted in its materiality assessment. Depending on the undertaking’s specific facts and circumstances, a disaggregation by subsidiary may be necessary.

56. Where data from different levels, or multiple locations within a level, is aggregated, the undertaking shall ensure that this aggregation does not obscure the specificity and context necessary to interpret the information. The undertaking shall not aggregate material items that differ in nature.

57. When the undertaking presents information disaggregated by sectors, it shall adopt the ESRS sector classification to be specified in a delegated act adopted by the Commission pursuant to article 29b(1) third subparagraph, point (ii), of Directive 2013/34/EU. When a topical or sector-specific ESRS requires that a specific level of disaggregation is adopted in preparing a specific item of information, the requirement in the topical or sector-specific ESRS shall prevail.