1. Introduction

Managing and disclosing pollution is a vital aspect of corporate responsibility in today's world. Businesses must be transparent about the pollutants they emit to air, water, and soil, as well as their use of microplastics. This article focuses on the disclosure requirements regarding the pollution of air, water, and soil.

How companies can effectively disclose this information will be covered in another article.

2. Pollution of Air, Water, and Soil

Companies are required to disclose the types and amounts of pollutants they release through their operations. This includes:

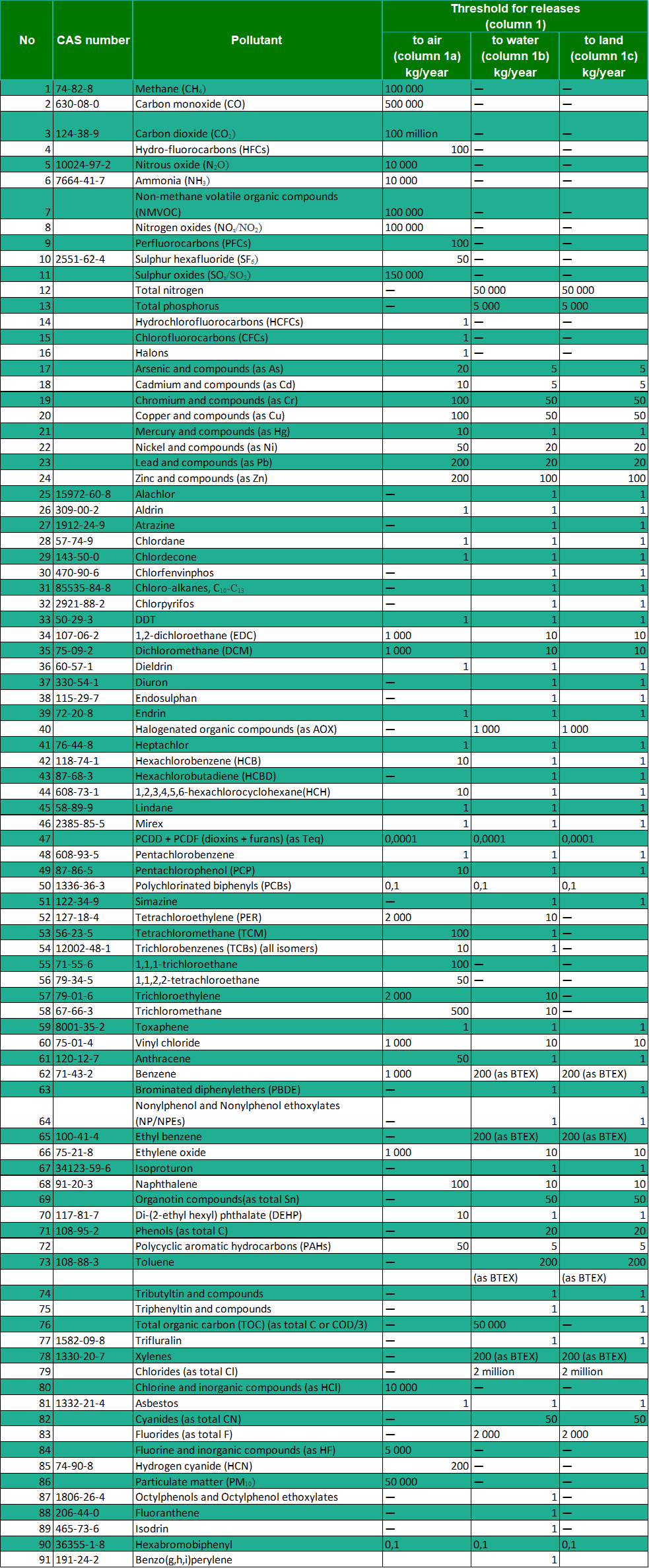

Specific pollutants: Details on each pollutant listed in the European Pollutant Release and Transfer Register (E-PRTR) Regulation emitted to air, water, and soil.

Microplastics: Information on the generation and use of microplastics within their operations.

The European Pollutant Release and Transfer Register (E-PRTR) is a publicly accessible database that tracks key environmental data from industrial facilities across Europe, including emissions to air, water, and land, as well as off-site transfers of pollutants. Regulation (EC) No 166/2006 established the E-PRTR, and it was amended in 2019 to streamline reporting requirements and enhance data accessibility. This regulation ensures that industrial operators report their pollutant releases and transfers annually, with national authorities compiling and submitting this data to the European Commission, which then makes it available to the public, supporting transparency and public participation in environmental decision-making.

The disclosed data must include emissions from all facilities under the company’s financial and operational control, provided they exceed certain threshold values specified in the E-PRTR Regulation.

To give a complete picture, companies should also provide contextual information, such as:

Changes over time: How emissions have varied over different periods.

Measurement methodologies: The methods used to measure emissions.

Data collection processes: The processes and types of data sources used for pollution-related reporting.

Methodology Transparency

If a company uses methods less accurate than direct measurement to quantify emissions, it must explain why and disclose the basis of its estimates, including the degree of uncertainty and the range of possible values.

Companies must disclose the types and amounts of pollutants they emit to air, water, and soil, including microplastics. This data should be comprehensive, covering all facilities under their control, and should include contextual information on changes over time, measurement methodologies, and data collection processes.

3. Conclusion

By disclosing detailed information about their pollution, companies can demonstrate their commitment to environmental responsibility. This includes not only the types and amounts of pollutants emitted but also the methodologies and data sources used.

In an upcoming article, we will explore how companies can report on these disclosures. Subscribe to stay updated.

Want to ask questions?

Relevant Standards

ESRS E2

Disclosure Requirement E2-4 – Pollution of air, water and soil

26. The undertaking shall disclose the pollutants that it emits through its own operations, as well as the microplastics it generates or uses.

27. The objective of this Disclosure Requirement is to provide an understanding of the emissions that the undertaking generates to air, water and soil in its own operations, and of its generation and use of microplastics.

28. The undertaking shall disclose the amounts of:

(a) each pollutant listed in Annex II of Regulation (EC) No 166/2006 of the European Parliament and of the Council (European Pollutant Release and Transfer Register “E-PRTR Regulation”) emitted to air, water and soil, with the exception of emissions of GHGs which are disclosed in accordance with ESRS E1 Climate Change;

(b) microplastics generated or used by the undertaking.

29. The amounts referred in paragraph 28 shall be consolidated amounts including the emissions from those facilities over which the undertaking has financial control and those over which it has operational control. The consolidation shall include only the emissions from facilities for which the applicable threshold value specified in Annex II of Regulation (EC) No 166/2006 is exceeded.

30. The undertaking shall put its disclosure into context and describe:

(a) the changes over time,

(b) the measurement methodologies; and

(c) the process(es) to collect data for pollution-related accounting and reporting, including the type of data needed and the information sources.

31. When an inferior methodology compared to direct measurement of emissions is chosen to quantify emissions, the reasons for choosing this inferior methodology shall be outlined by the undertaking. If the undertaking uses estimates, it shall disclose the standard, sectoral study or sources which form the basis of its estimates, as well as the possible degree of uncertainty and the range of estimates reflecting the measurement uncertainty.