[BREAKDOWN] E1-8: What are organizational & operational boundaries for emissions reporting?

ESRS E1: What are organizational & operational boundaries for emissions reporting? Using the GHG protocol.

Last updated: 15-08-2025

1. Introduction

When businesses report their greenhouse gas (GHG) emissions, they first need to define who and what is included in their calculations. This starts with setting organizational boundaries, which determine which parts of a company’s structure are included in its emissions reporting. Next, they define operational boundaries, which categorize emissions into Scope 1 (direct emissions), Scope 2 (indirect emissions from energy use), and Scope 3 (all other indirect emissions).

This article will help you understand:

✅ The difference between organizational and operational boundaries in GHG accounting.

✅ How companies decide whether to use equity share, financial control, or operational control methods.

✅ A guide on choosing the right organizational boundary for your company.

✅ A visual example illustrating how different approaches impact emissions reporting.

✅ What the Corporate Sustainability Reporting Directive (CSRD) requires for emissions reporting.

By the end of this article, you’ll have a clear understanding of how to define your company’s boundaries in a way that ensures compliance, transparency, and consistency in emissions reporting.

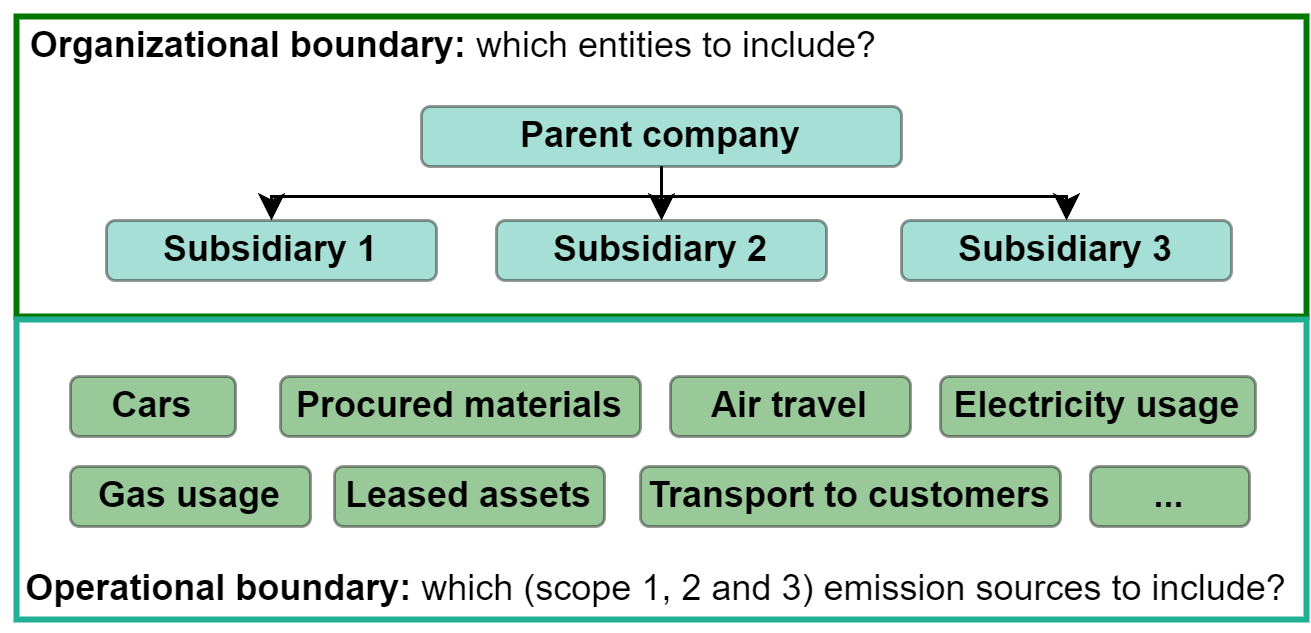

2. Understanding organizational vs. operational boundaries in GHG accounting

Organizational boundaries: who’s in and who’s out?

Think of organizational boundaries as deciding which parts of your company "count" when adding up emissions. Businesses aren’t always standalone entities, they might have subsidiaries, joint ventures, or leased operations. So, how do you decide what to include?

There are two main approaches:

Equity share approach – You account for emissions based on your ownership percentage. If your company owns 50% of a factory, you report 50% of its emissions.

Control approach – You report 100% of emissions from operations you control, even if you don’t fully own them. Control can be:

Financial control (you call the financial shots)

Operational control (you manage day-to-day operations)

Example: If your company owns 40% of a power plant but fully operates it, the control approach means you report all its emissions. The equity approach means you only report 40%.

Operational boundaries: what activities produce emissions?

Once you’ve defined who is included (organizational boundaries), you need to figure out which emissions to track (operational boundaries). These are categorized into three scopes:

Scope 1 (direct emissions) – From sources your company owns or controls (e.g., company vehicles, on-site fuel combustion).

Scope 2 (indirect emissions from energy) – From purchased electricity, steam, or heating/cooling.

Scope 3 (other indirect emissions) – All other indirect emissions (e.g., business travel, supply chain, waste disposal).

Why is this important?

Accuracy: Makes sure you’re not double-counting (or missing) emissions.

Transparency: Helps stakeholders understand your carbon footprint.

Compliance: Many reporting programs (like GHG Protocol) require clear boundary definitions.

Tip: Start by setting organizational boundaries (who’s in your reporting), then define operational boundaries (what emissions to track). In case you already want read about operational boundaries: