1. Introduction

In the effort to combat climate change, businesses need to be transparent about the targets they set for reducing greenhouse gas (GHG) emissions and adapting to climate impacts. This includes sharing their specific goals, how they plan to achieve them, and how these targets align with global efforts to limit warming to 1.5°C. In this article, I will briefly explain the requirements for companies to disclose their climate-related targets.

More elaborate articles are available, which can be found below.

2. What is a climate target?

In general, climate targets are goals set by countries or organizations to cut greenhouse gas emissions and limit global warming (ideally to 1.5 °C). Examples include:

Short-term: cut emissions 30% by 2030

Long-term: reach net zero by 2050

Targets help governments and companies plan what changes they need to make (e.g. shifting to renewable energy, improving energy efficiency). By having a measurable goal, we can track whether actions are working or need adjustment.

The ESRSes define targets as follows:

“Measurable, outcome-oriented and time-bound goals that the undertaking aims to achieve in relation to material impacts, risks or opportunities. They may be set voluntarily by the undertaking or derive from legal requirements on the undertaking.”

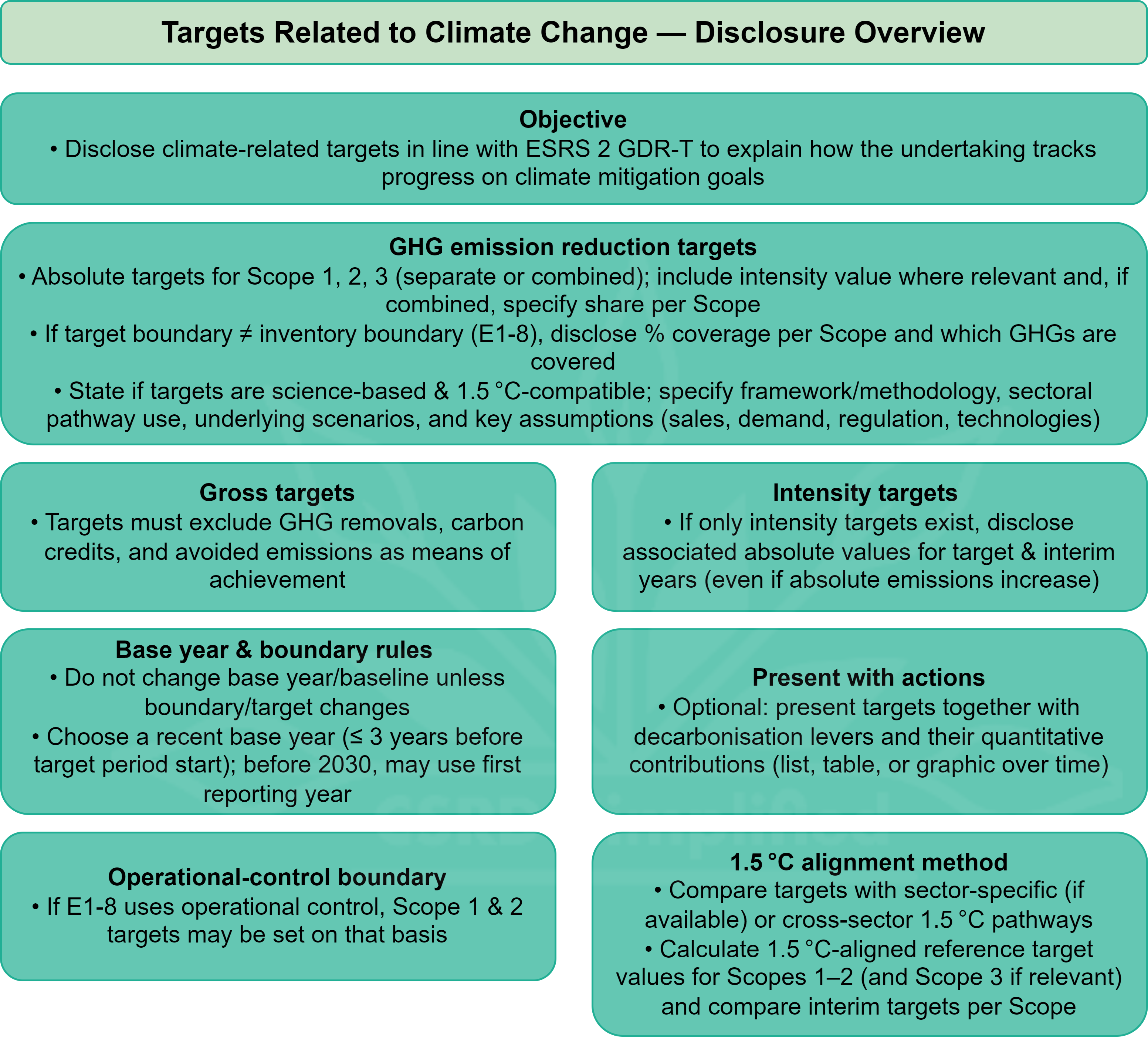

3. ESRS E1-6 at a glance

E1-6 is the disclosure on “Targets related to climate change” inside ESRS E1. It requires you to present climate targets “in accordance with ESRS 2 GDR-T,” which is the general backbone for targets (e.g., baseline, scope, target year, methodology, assumptions).

Under paragraph ESRS E1-6, you must disclose:

Read the elaborate breakdown and detailed requirements of ESRS E1-6 here.

To learn more about science-based targets read this article.

![[BREAKDOWN] E1-6: Setting climate targets](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

4. How E1-6 links to the rest of ESRS E1

E1-6 = your climate targets.

This is where you publish the actual GHG-reduction targets.

Connection of E1-6 to E1-5 (actions & resources).

Show targets and actions together so it is clear how you’ll reach your targets. List your decarbonisation levers (e.g., efficiency, fuel switch, renewables, phase-outs) and quantify their contribution to the target.

Both E1-6 and E1-5 are tied into E1-1 (the transition plan).

Your transition plan should pull the story together: targets (E1-6), actions/levers and financing (E1-5), and how the strategy is compatible with 1.5°C and the EU goal of climate neutrality by 2050. Think of E1-1 as the umbrella narrative that references the detailed disclosures instead of repeating them.

3. Bottom line

E1-6 asks you to do three things well:

declare reduction commitments

be precise about scope coverage, boundaries, baselines and milestones, and

show 1.5°C compatibility with transparent frameworks, scenarios and assumptions

If you hit each of these, your climate-target disclosure is both useful and aligned with ESRS E1.