[INSIGHT] E1: EU taxonomy for sustainable activities

EU taxonomy for sustainable activities, what is it and to who does it apply?

1. Introduction

The EU taxonomy aims to channel investments towards economic activities that are essential for the transition to a sustainable economy, aligning with the European Green Deal objectives. This classification system sets out criteria for economic activities that are consistent with a net-zero trajectory by 2050 and other broader environmental goals.

The EU taxonomy plays several important roles:

Creating security for investors: By defining what is considered environmentally sustainable, it provides clarity and reduces uncertainty.

Protecting private investors from greenwashing: Ensures that investments labeled as ‘green’ are genuinely sustainable.

Helping companies become more climate-friendly: Guides businesses in aligning their operations with environmental goals.

Mitigating market fragmentation: Promotes a unified market approach across the EU.

In this article we will explain who is subject to the EU Taxonomy and what it is.

2. Who is Subject to the EU Taxonomy Regulation?

The EU Taxonomy Regulation mandates specific disclosure requirements aimed at enhancing transparency regarding the environmental performance of economic activities. This regulation primarily targets:

Large financial and non-financial companies: The regulation applies to large companies that fall under the scope of the Non-Financial Reporting Directive (NFRD). These companies are required to disclose the extent to which their activities meet the criteria set out in the EU Taxonomy. The NFRD typically covers large public-interest entities with over 500 employees, including listed companies, banks, and insurance companies.

Financial market participants: Financial market participants, such as asset managers, are also required to disclose how the activities funded by their financial products align with the EU Taxonomy criteria. This includes investment funds, pension funds, insurance-based investment products, and other financial products that are marketed as sustainable investments.

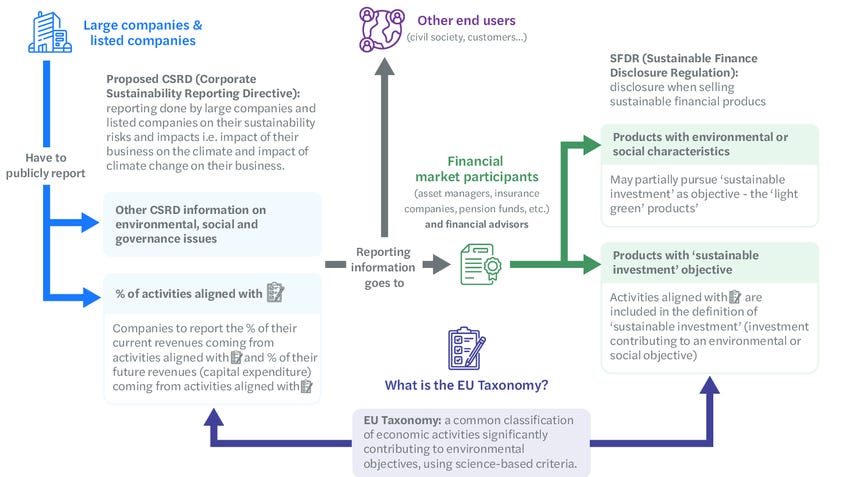

From 2024 onwards, the scope of the EU Taxonomy Regulation will be extended to include companies the fall under the Corporate Sustainability Reporting Directive (CSRD). Companies that are not required to comply with the CSRD can still choose to voluntarily disclose this information. They might do this to gain access to sustainable financing or for other business reasons.

3. What is the EU Taxonomy?

The EU Taxonomy Regulation necessitates that the covered entities provide detailed disclosures. Companies must report the extent to which their activities are Taxonomy-aligned. The EU Taxonomy itself, is a classification system for activities. This overview explains how the EU taxonomy relates to the CSRD:

How Does the Taxonomy Define Sustainable Economic Activities?

At the heart of the Taxonomy are strict criteria that define what constitutes a sustainable economic activity. For an activity to be considered taxonomy-aligned, it must:

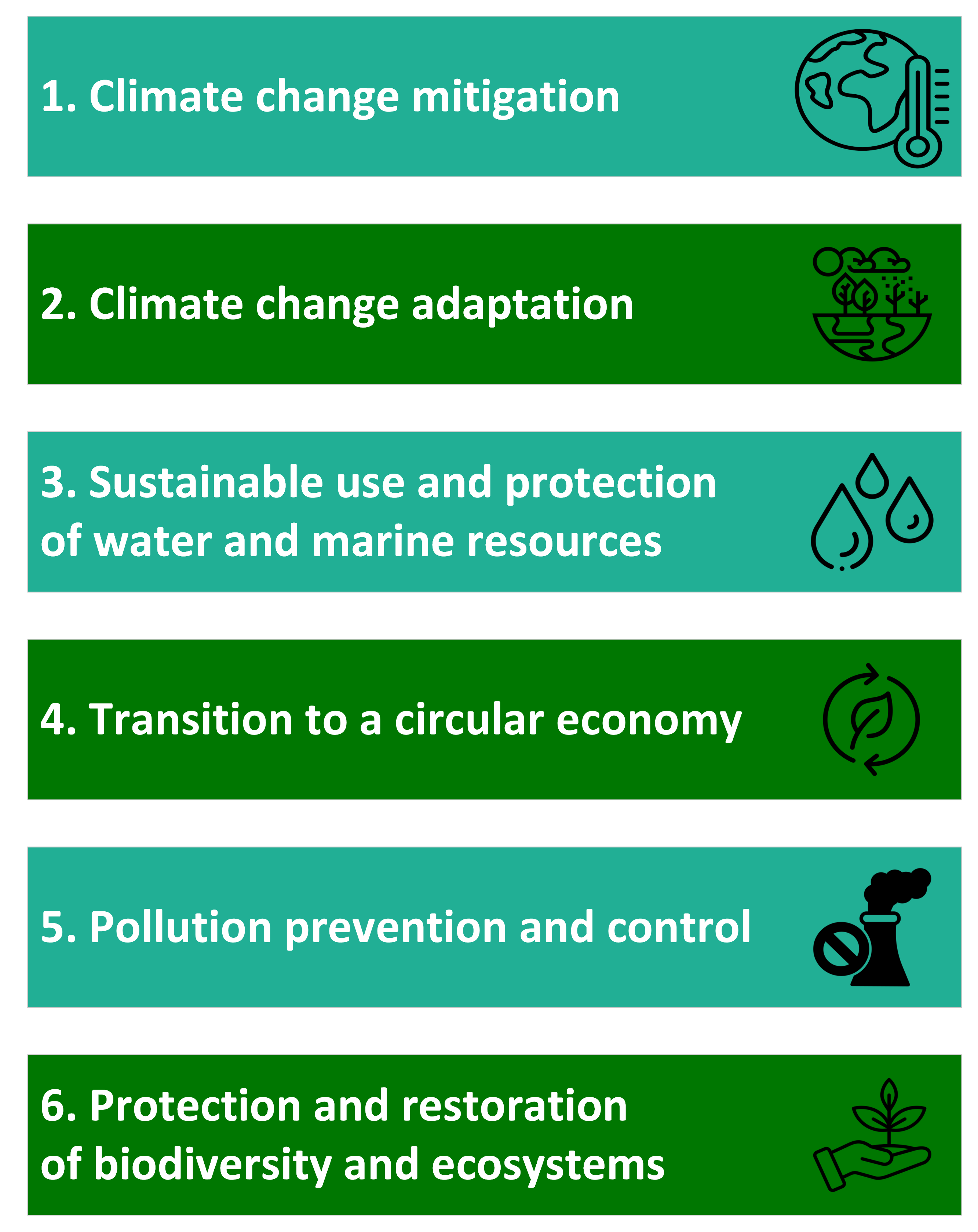

Substantially contribute to at least one of the six environmental objectives:

Do No Significant Harm (DNSH) to any of the other environmental objectives while respecting basic human rights and labor standards. The Technical Screening Criteria (TSC) lay out the specific requirements and thresholds that activities must meet to qualify as sustainable.

The European Commission is responsible for defining the actual list of sustainable activities by setting technical screening criteria for each environmental objective through delegated and implementing acts. This list can be found here.

What are Enabling and Transitional Activities?

The Taxonomy also introduces the concepts of enabling and transitional activities:

Enabling activities are those that allow other economic activities to make a significant contribution to one or more environmental objectives. However, these activities must not lead to a 'lock-in' of assets that would undermine long-term environmental goals and must have a substantial positive environmental impact throughout their lifecycle.

Transitional activities are activities that, while not fully sustainable, play a critical role in the transition to a climate-neutral economy. These activities must meet stringent criteria, including having no viable low-carbon alternatives and achieving the best environmental performance in their sector.

Specific Disclosures for Different Types of Undertakings

A full overview of the different disclosures for different types of undertakings can be found here. In general the following needs to be disclosed per type of undertaking:

Non-financial undertakings: the proportion of their turnover, capital expenditure, and operating expenditure related to taxonomy-aligned activities.

Asset managers: the proportion of investments in taxonomy-aligned activities relative to total investments managed.

Credit institutions: the Green Asset Ratio (GAR), which measures the proportion of their assets related to taxonomy-aligned activities.

Investment firms: the proportion of their assets and the revenue from services related to taxonomy-aligned activities.

Insurance/reinsurance undertakings: the proportion of their investments and non-life underwriting activities related to taxonomy-aligned activities.

The EU Taxonomy Regulation mandates disclosure requirements for large financial and non-financial companies under the Non-Financial Reporting Directive (NFRD) and financial market participants, such as asset managers, to report the alignment of their activities with sustainable economic criteria. From 2024, the scope will expand to include companies under the Corporate Sustainability Reporting Directive (CSRD), requiring them to disclose the extent to which their activities are taxonomy-aligned.

3. Conclusion

The EU Taxonomy Regulation is a landmark initiative that underscores the EU's commitment to sustainability and climate action. By providing a clear and consistent framework for identifying environmentally sustainable (taxonomy-aligned) activities, it helps to channel investments into areas that are crucial for the transition to a greener economy. As the regulation continues to be implemented, it will likely become a global benchmark for sustainable finance.

Relevant Standards

Removed or changed with the simplified ESRS standards:

ESRS E1

Disclosure Requirement E1-4 – Targets related to climate change mitigation and adaptation

30. The undertaking shall disclose the climate-related targets it has set.

31. The objective of this Disclosure Requirement is to enable an understanding of the targets the undertaking has set to support its climate change mitigation and adaptation policies and address its material climate-related impacts, risks and opportunities.

32. The disclosure of the targets required in paragraph 30 shall contain the information required in ESRS 2 MDR-T Tracking effectiveness of policies and actions through targets.

33. For the disclosure required by paragraph 30, the undertaking shall disclose whether and how it has set GHG emissions reduction targets and/or any other targets to manage material climate-related impacts, risks and opportunities, for example, renewable energy deployment, energy efficiency, climate change adaptation, and physical or transition risk mitigation.

34. If the undertaking has set GHG emission reduction targets39, ESRS 2 MDR-T and the following requirements shall apply:

(a) GHG emission reduction targets shall be disclosed in absolute value (either in tonnes of CO2eq or as a percentage of the emissions of a base year) and, where relevant, in intensity value;

(b) GHG emission reduction targets shall be disclosed for Scope 1, 2, and 3 GHG emissions, either separately or combined. The undertaking shall specify, in case of combined GHG emission reduction targets, which GHG emission Scopes (1, 2 and/or 3) are covered by the target, the share related to each respective GHG emission Scope and which GHGs are covered. The undertaking shall explain how the consistency of these targets with its GHG inventory boundaries is ensured (as required by Disclosure Requirement E1-6). The GHG emission reduction targets shall be gross targets, meaning that the undertaking shall not include GHG removals, carbon credits or avoided emissions as a means of achieving the GHG emission reduction targets;

(c) the undertaking shall disclose its current base year and baseline value, and from 2030 onwards, update the base year for its GHG emission reduction targets after every five year period thereafter. The undertaking may disclose the past progress made in meeting its targets before its current base year provided that this information is consistent with the requirements of this Standard;

(d) GHG emission reduction targets shall at least include target values for the year 2030 and, if available, for the year 2050. From 2030, target values shall be set after every 5- year period thereafter;

(e) the undertaking shall state whether the GHG emission reduction targets are science based and compatible with limiting global warming to 1.5°C. The undertaking shall state which framework and methodology has been used to determine these targets including whether they are derived using a sectoral decarbonisation pathway and what the underlying climate and policy scenarios are and whether the targets have been externally assured. As part of the critical assumptions for setting GHG emission reduction targets, the undertaking shall briefly explain how it has considered future developments (e.g., changes in sales volumes, shifts in customer preferences and demand, regulatory factors, and new technologies) and how these will potentially impact both its GHG emissions and emissions reductions; and

(f) the undertaking shall describe the expected decarbonisation levers and their overall quantitative contributions to achieve the GHG emission reduction targets (e.g., energy or material efficiency and consumption reduction, fuel switching, use of renewable energy, phase out or substitution of product and process).