Atmospheric CO₂ accumulates because every year humanity adds more than natural sinks can remove. Until that imbalance is reversed, concentrations (and therefore climate risks) will keep rising.

CSRD Simplified is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Therefore, companies are turning to greenhouse gas (GHG) removals and mitigation. But without clarity on definitions, reporting, and quality, these efforts risk being seen as greenwashing. Understanding the distinctions between removals and mitigation, and how to report them under frameworks like the CSRD, is important for credibility and compliance.

What you’ll learn:

✅ The difference between GHG removals and mitigation ✅ How to classify climate projects inside vs. outside the value chain ✅ Which projects are eligible under CSRD reporting rules (ESRS E1-9) ✅ What to disclose under the CSRD

By the end, you’ll understand how to integrate removals and mitigation into a climate strategy.

2. GHG removals and mitigation: core concepts clarified

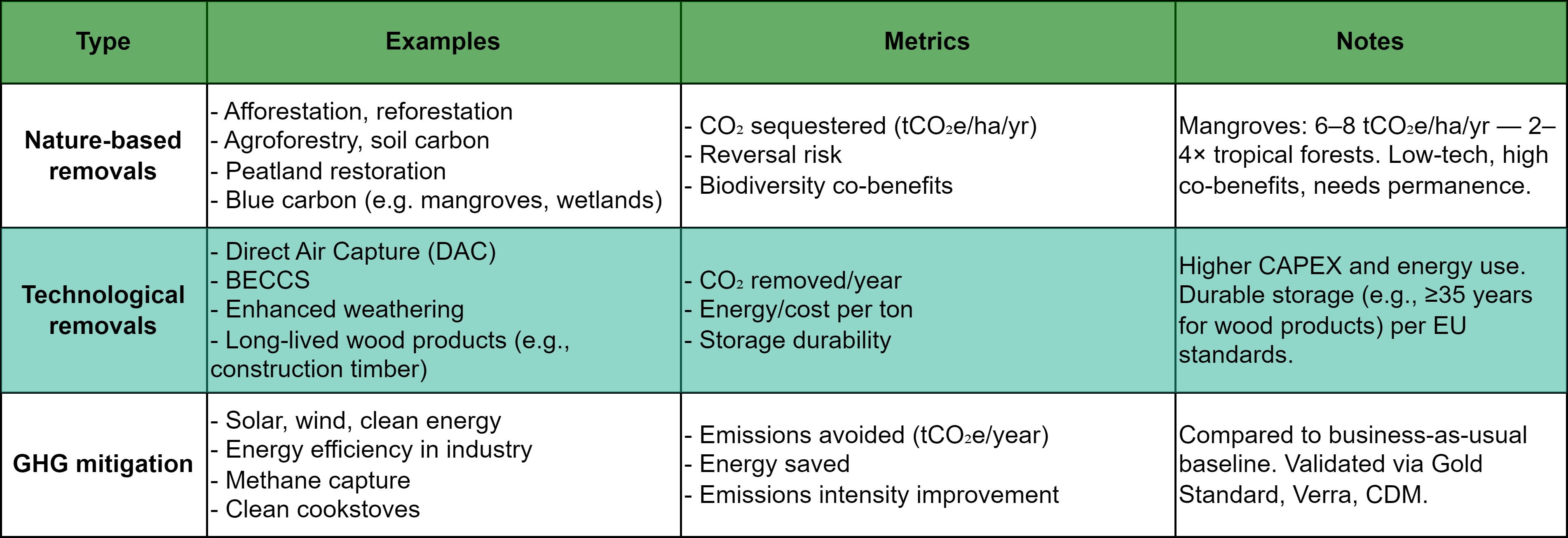

GHG removals refer to processes that permanently remove greenhouse gases from the atmosphere, such as planting forests, restoring wetlands, or using engineered technologies like Direct Air Capture (DAC). These can be either nature-based (e.g. afforestation, soil carbon projects, mangrove restoration) or technological (e.g. BECCS, enhanced mineralization, or using wood in construction if it avoids decay for ≥35 years).

GHG mitigation reduces emissions before they enter the atmosphere.

Examples include:

Installing solar or wind power

Improving energy efficiency in factories

Capturing methane from agriculture or landfills

Mitigation slows down emissions going into the atmosphere.

Removals speed up the process of taking carbon out of it.

3. Reporting under CSRD

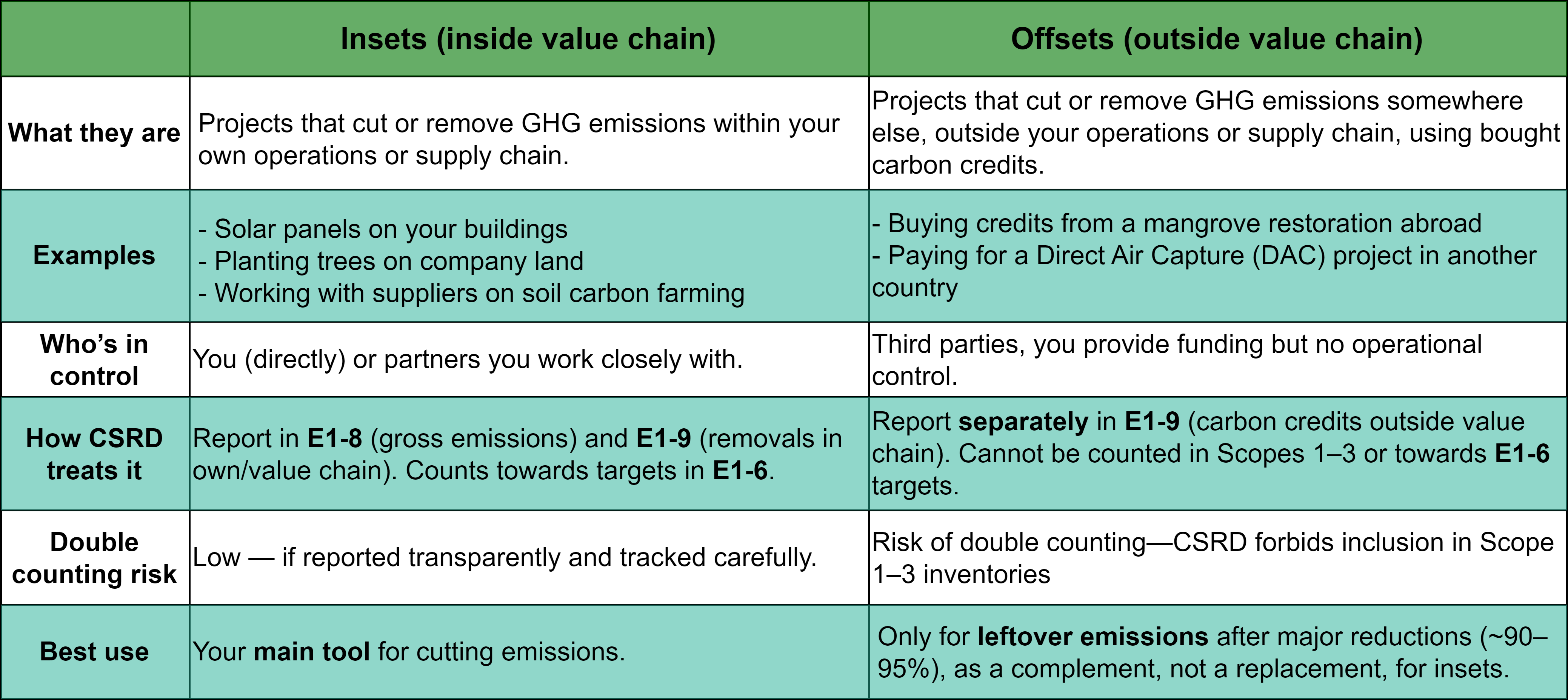

Under the amended ESRS E1, Disclosure Requirement E1-9 requires companies to clearly separate:

GHG removals and storage within own operations or value chain (insets)

Describe each removal/storage project (e.g., afforestation, soil carbon enhancement, direct air capture).

State which GHGs are involved.

Identify whether the method is biological, technological, or hybrid.

Explain how the carbon is stored and how permanence is ensured.

Disclose any reversals (in tCO₂e) during the reporting period.

Include assumptions on permanence, leakage, and risk management.

Carbon credits from projects outside own operations/value chain (offsets/mitigation)

Disclose the volume of credits verified against recognised quality standards and cancelled in the reporting year.

State the volume planned for cancellation in the future.

Explain whether projects are nature-based or technological removals.

Clarify if credits are EU-based and/or aligned with Article 6 of the Paris Agreement.

Credits from internal projects cannot be reported here to avoid double counting.

Important:

Credits cannot be included in gross GHG reduction targets under E1-6.

Use of credits should be supplementary — generally for residual emissions after deep decarbonisation (90–95% reduction), based on science-based pathway guidance.

Public claims of climate or carbon neutrality must explain how credit use does not delay or reduce own reductions, and must describe credit integrity and quality.

In practice, the first step for any company is to map where emissions are occurring, across Scopes 1, 2, and 3, and determine whether to focus on emissions reduction (mitigation) or atmospheric carbon removal.

![[BREAKDOWN] E1-8: Choosing operational boundaries for emissions reporting](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)