1. Introduction

The Corporate Sustainability Reporting Directive (CSRD) is a new regulation that expands the scope of sustainability reporting for businesses operating within the European Union (EU). Its goal is to ensure that companies are transparent about their environmental, social, and governance (ESG) practices, allowing investors, consumers, and regulators to better understand their impact on society and the planet.

In this article, we'll break down the key aspects of the CSRD, who it applies to —both within and outside of the EU— and when the new reporting requirements take effect.

Here’s a summary of the reporting timeline under the CSRD:

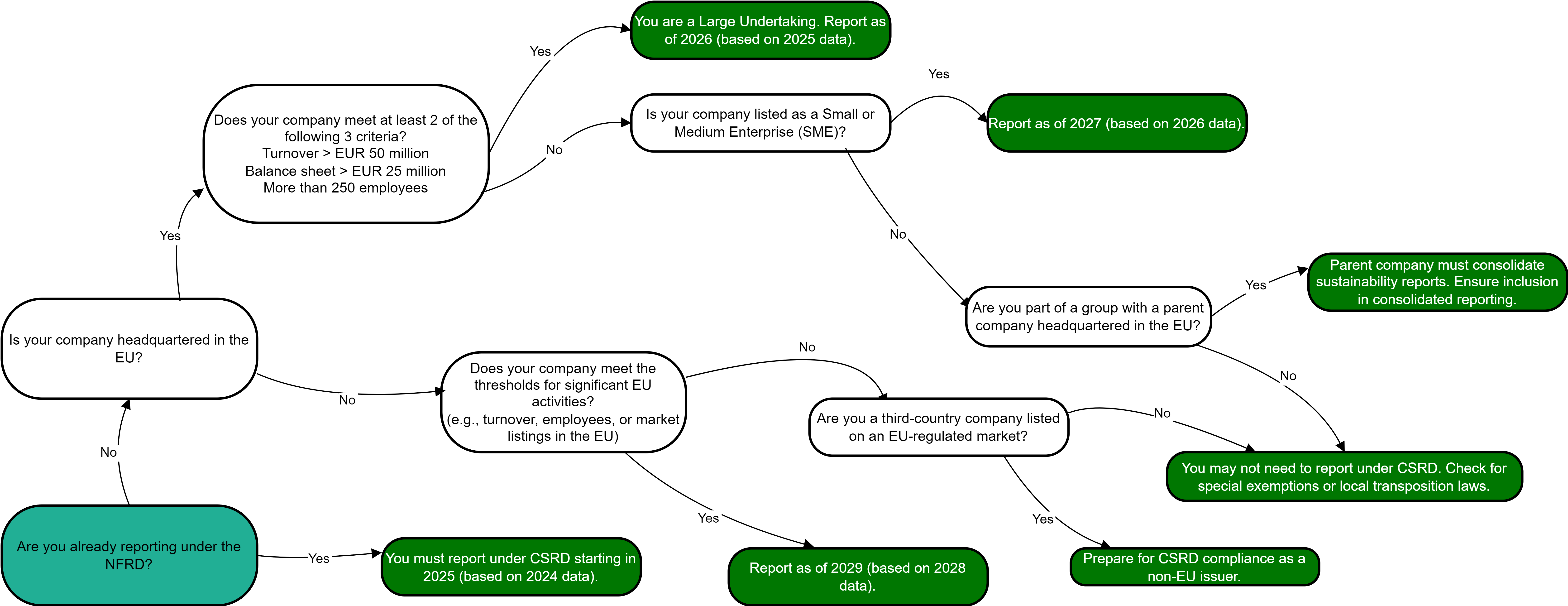

2025: Businesses already covered by the NFRD start reporting on their 2024 financial data.

2026: Large EU companies and parent companies of large groups start reporting on their 2025 financial data.

2027: Listed SMEs begin reporting based on their 2026 financial data.

2029: Third-country companies with significant EU operations need to report on their 2028 financial data.

2. Who needs to comply with the CSRD?

The CSRD applies to a wide range of businesses, both within the EU and those based outside the EU with significant operations in Europe. Here’s a breakdown of which companies will need to report, and when:

Companies already reporting under the Non-Financial Reporting Directive (NFRD): These businesses will need to comply with the CSRD starting in 2025, reporting on data from the 2024 financial year.

Large EU businesses and parent companies of large groups: They will need to begin reporting in 2026, based on 2025 financial data. To qualify as a "large" undertaking, companies must meet at least two of the following criteria for two consecutive years:

A net turnover exceeding EUR 50 million.

A balance sheet total exceeding EUR 25 million.

An average of more than 250 employees.

Listed Small and Medium-Sized Enterprises (SMEs): These will need to start reporting by 2027, covering their 2026 financial year.

Third-country companies (those based outside the EU): Businesses headquartered outside the EU but with EU subsidiaries or branches, or whose securities are traded on EU markets, will need to comply by 2029, based on 2028 financial data. More about this in the next section.

3. How does the CSRD impact third-country companies?

The CSRD isn’t limited to EU-based companies. It also applies to companies outside the EU if they have a significant presence in the EU through subsidiaries, branches, or public securities listings. There are two key ways this can happen:

EU subsidiaries or branches: If a third-country company has large EU subsidiaries (meeting the criteria for large undertakings) or listed SMEs, it will be required to produce a group-level sustainability report by 2029.

Non-EU issuers: Any non-EU company with securities listed on a regulated market within the EU must comply with the CSRD and file sustainability reports according to European standards.

These companies must adhere to the European Sustainability Reporting Standards (ESRS), which are being developed to guide sustainability reporting in the EU. Exemptions may apply if subsidiaries are already covered in the parent company’s consolidated report and that report complies with EU standards.

4. Special cases and exemptions

Certain companies may qualify for exemptions or special reporting rules under the CSRD:

Subsidiaries covered by parent company reports: EU subsidiaries may be exempt from producing their own sustainability reports if they are already included in a parent company’s consolidated report. For this exemption to apply, the parent company’s report must meet the ESRS standards or, if the parent is outside the EU, be deemed equivalent by EU authorities.

Artificial consolidation for reporting purposes: Until 2030, companies can use a simplified reporting approach by consolidating all EU subsidiaries into a single sustainability report. The largest EU subsidiary, based on turnover, would take the lead in reporting on behalf of the entire group.

5. What happens if you do not comply?

Failing to meet the CSRD’s requirements can result in serious consequences, varying across EU member states. Potential penalties include:

Fines and criminal charges: Each country will impose its own sanctions, which could involve significant fines or even criminal prosecution in some cases.

Audit issues: Non-compliance could lead to audit failures, which might affect a company’s ability to operate or maintain investor trust.

Reputational damage: Being publicly identified as non-compliant could harm your company’s reputation, leading to lost business or decreased investor confidence.

Legal liability: Non-compliant businesses could also face litigation for failing to meet their reporting obligations.

The CSRD includes a requirement for external assurance on sustainability reports. Initially, businesses will need to obtain limited assurance, meaning an auditor will confirm that no significant misstatements have been found. Over time, this will evolve into reasonable assurance, which involves a more detailed audit of the sustainability data.

6. Key actions for businesses

As the CSRD rolls out, companies—especially those with EU operations or group structures—should start preparing now. Here are some important steps to take:

7. Conclusion

The CSRD represents a significant shift in how companies must report on their sustainability practices. With deadlines approaching over the next few years, businesses—especially those with complex group structures or operations within the EU—need to start preparing now. By understanding the requirements and planning ahead, companies can avoid penalties, ensure compliance, and meet investor and societal expectations.

Relevant Standards

ESRS 1

5.1 Reporting undertaking and value chain

The sustainability statement shall be for the same reporting undertaking as the financial statements. For example, if the reporting undertaking is a parent company required to prepare consolidated financial statements, the sustainability statement will be for the group. This requirement does not apply where the reporting undertaking is not required to draw-up financial statements or where the reporting undertaking is preparing consolidated sustainability reporting pursuant to Article 48i of Directive 2013/34/EU.

The information about the reporting undertaking provided in the sustainability statement shall be extended to include information on the material impacts, risks and opportunities connected with the undertaking through its direct and indirect business relationships in the upstream and/or downstream value chain (“value chain information”). In extending the information about the reporting undertaking, the undertaking shall include material impacts, risks and opportunities connected with its upstream and downstream value chain:

following the outcome of its due diligence process and of its materiality assessment; and

in accordance with any specific requirements related to the value chain in other ESRS.

Paragraph 63 does not require information on each and every actor in the value chain , but only the inclusion of material upstream and downstream value chain information. Different sustainability matters can be material in relation to different parts of the undertaking’s upstream and downstream value chain. The information shall be extended to include value chain information only in relation to the parts of the value chain for which the matter is material.

The undertaking shall include material value chain information when this is necessary to:

allow users of sustainability statements to understand the undertaking’s material impacts, risks and opportunities ; and/or

produce a set of information that meets the qualitative characteristics of information (see Appendix B of this Standard).

When determining at which level within its own operations and its upstream and downstream value chain a material sustainability matter arises, the undertaking shall use its assessment of impacts, risks and opportunities following the double materiality principle (see chapter 3 of this Standard).

When associates or joint ventures, accounted for under the equity method or proportionally consolidated in the financial statements, are part of the undertaking’s value chain, for example as suppliers, the undertaking shall include information related to those associates or joint ventures in accordance with paragraph 63 consistent with the approach adopted for the other business relationships in the value chain. In this case, when determining impact metrics , the data of the associate or joint venture are not limited to the share of equity held, but shall be taken into account on the basis of the impacts that are connected with the undertaking’s products and services through its business relationships.

ESRS Implementation Q&A Platform – Compilation of Explanations January – May 2024

EFRAG IG 1: Materiality Assessment Implementation Guidance

DIRECTIVE (EU) 2022/2464 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

Article 19a, 29a, 40a-d