[CSRD] E2-4: Pollution of air, water and soil

CSRD Simplified: Disclosure Requirement E2-4: Pollution of air, water and soil

1. Introduction

We have covered the rules (E2-1), the work (E2-2), and the goals (E2-3). Now we arrive at the evidence. ESRS E2-4 asks undertakings to disclose the data on what they are releasing into the environment.

This disclosure is the proof of performance. It provides the numbers that allow stakeholders to assess your environmental footprint and verify if your actions are working.

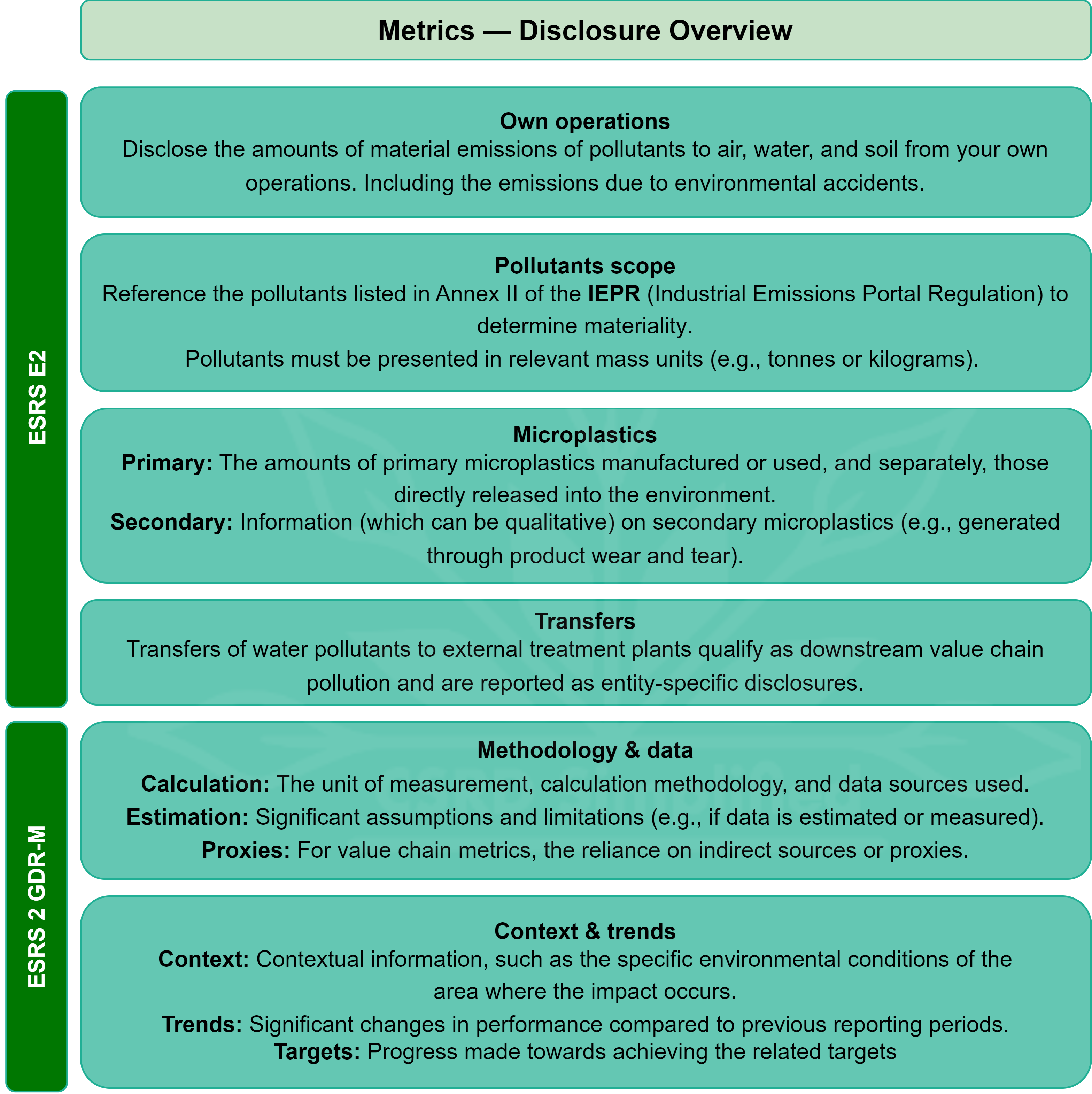

I will briefly explain the requirements for disclosing metrics on pollution of air, water, and soil.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are pollution metrics?

Pollution metrics are quantitative measurements of the specific pollutants your company releases into the environment.

The scope covers three main areas:

Air emissions: Pollutants released into the atmosphere (e.g., Nitrogen Oxides (NOx), Sulfur Oxides (SOx), Volatile Organic Compounds (VOCs)). Note: GHGs like CO2 are covered in E1, not here.

Water emissions: Pollutants discharged into freshwater or seawater (e.g., Nitrates, Phosphates, Heavy Metals).

Soil emissions: Pollutants released directly to soil (e.g., pesticides, industrial leaks).

Plus microplastics: E2-4 also specifically targets microplastics, which are tiny plastic particles that accumulate in the environment. Companies must report on both the microplastics they intentionally use (primary) and those generated as a byproduct of wear and tear (secondary).

The ESRSes define metrics as follows:

“Qualitative and quantitative indicators that the undertaking uses to measure and report on the effectiveness of the delivery of its sustainability-related policies and against its targets over time. Metrics also support the measurement of the undertaking’s results in respect of affected people, the environment and the undertaking.”

3. ESRS E2-4 at a glance

E2-4 requires that “the undertaking shall disclose the amounts of material emissions of pollutants to air, water and soil from its own operations”.

To comply, the disclosure must include:

The European Pollutant Release and Transfer Register (E-PRTR), originally established by Regulation (EC) No 166/2006, historically served as the publicly accessible database tracking key environmental data from industrial facilities across Europe. While it was amended in 2019 to streamline reporting, this framework has now been superseded. In 2024, the EU adopted the Industrial Emissions Portal Regulation (IEPR)—Regulation (EU) 2024/1244, which officially repeals and replaces the E-PRTR.

Under this updated framework, the existing register is being upgraded into a more comprehensive Industrial Emissions Portal. The regulation ensures that industrial operators continue to report their pollutant releases (to air, water, and land), off-site transfers, and resource usage annually. National authorities compile and submit this data to the European Commission, which makes it available to the public, supporting transparency and public participation in environmental decision-making.

The disclosed data must include emissions from all facilities under the company’s financial and operational control, provided they exceed the specific threshold values now detailed in Annex II of the IEPR (Regulation (EU) 2024/1244).

You can find the Annex here: Regulation - EU - 2024/1244 - EN - EUR-Lex

4. How E2-4 links to the rest of ESRS E2

E2-4 is the scorecard for your entire pollution strategy:

E2-1 (Policy): Defines your commitment to compliance and pollution reduction.

E2-2 (Action): Describes the technology (e.g., filters) installed to reduce emissions.

E2-3 (Target): Sets the goal (e.g., “keep NOx below 50 tonnes”).

E2-4 (Metric): Checks your progress. If you report 60 tonnes of NOx in E2-4, it immediately signals that you missed your E2-3 target, prompting questions about the effectiveness of your E2-2 actions.

5. Bottom line

E2-4 is often where companies face the biggest data challenges. To report effectively:

Check the list: Review Annex II of the IEPR (European Industrial Emissions Portal). If you emit it, you likely need to measure and report it.

Don’t forget water transfers: Sending dirty water to a municipal treatment plant doesn’t make the pollution disappear from your report, it just moves it to the “transfers” category.

Microplastics are new: Many companies have data on chemicals but lack data on microplastics. Start mapping where plastic particles might be shedding from your products now.

Absolute values matter: While intensity metrics (e.g., pollution per unit of revenue) are helpful for internal tracking, E2-4 demands absolute mass (tonnes/kg).

Relevant Sources

Regulation - EU - 2024/1244 - EN - EUR-Lex