[CSRD] E2-3: Targets related to pollution

CSRD Simplified: Disclosure Requirement E2-3: Targets related to pollution

1. Introduction

If policies (E2-1) set the rules and actions (E2-2) describe the work, then targets define the destination. ESRS E2-3 asks undertakings to disclose the specific, measurable goals they have set to reduce or eliminate pollution.

This disclosure allows investors and stakeholders to judge whether a company’s ambition matches the urgency of its material impacts. It transforms vague promises such as “we will be cleaner” into trackable commitments such as “we will reduce NOx emissions by 40% by 2030”.

I will briefly explain the requirements for disclosing pollution-related targets.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are pollution targets?

Pollution targets are measurable, time-bound objectives that the undertaking aims to achieve in relation to its material pollution impacts.

According to ESRS 2 (AR 47), targets regarding material impacts should be outcome-oriented. This means they should focus on the actual result for the environment or people (e.g., reduce tonnes of pollutants released), rather than just a procedural output (e.g., train 50 employees).

Typical examples include:

Air: Reduce absolute SOx and NOx emissions by 50% by 2030 against a 2020 baseline.

Water: Achieve zero discharge of untreated wastewater by 2027.

Plastics: Eliminate 100% of microplastics from product formulations by 2028.

Soil: Remediate all contaminated sites to regulatory standards by 2035.

The ESRSes define targets as follows:

“Measurable, outcome-oriented and time-bound goals that the undertaking aims to achieve in relation to material impacts, risks or opportunities. They may be set voluntarily by the undertaking or derive from legal requirements on the undertaking.”

3. ESRS E2-3 at a glance

E2-3 specifically requires that “the undertaking shall disclose its pollution-related targets in accordance with the provisions of ESRS 2 GDR-T“.

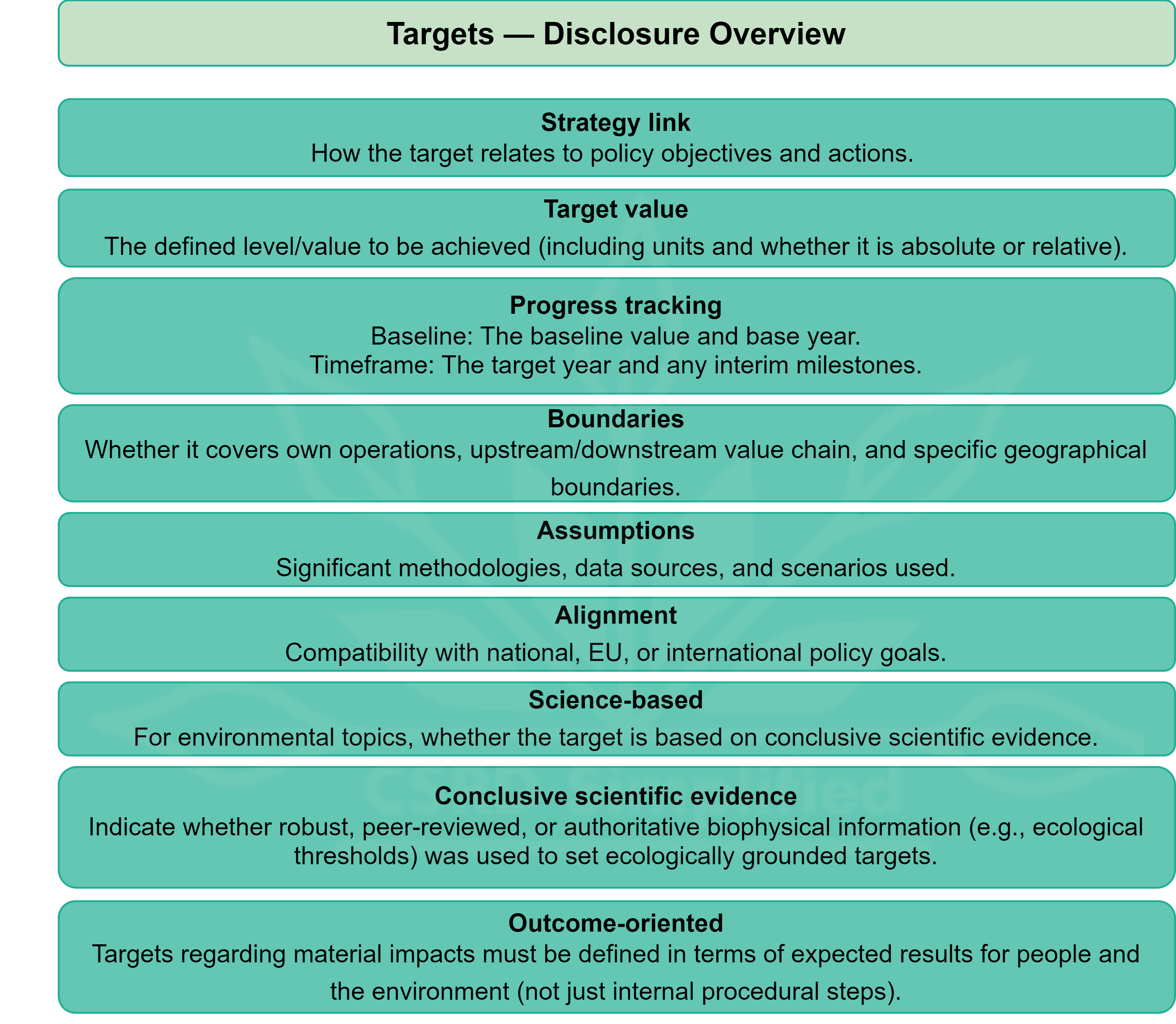

To comply with ESRS 2 GDR-T, the disclosure must include the following elements for each target:

4. How E2-3 links to the rest of ESRS E2

The target gives context to the metric. A metric is just a number, but with a target, it becomes a performance indicator.

E2-1 (Policy): “We commit to reducing air pollution.”

E2-2 (Action): “We are installing scrubbers.”

E2-3 (Target): “To achieve a 50% reduction by 2030.”

E2-4 (Metric): “This year, we emitted 1,200 tonnes, which is a 5% reduction.”

5. Bottom line

To report E2-3 effectively:

Be SMART: Ensure targets are Specific, Measurable, Achievable, Relevant, and Time-bound.

Define the baseline: A target of reducing emissions is meaningless without knowing the starting point (the baseline year and value).

Don’t hide: If you don’t have a target for a material pollution topic, you must admit it and explain how you are monitoring progress otherwise.

Look to science: Whenever possible, ground your pollution targets in scientific evidence (e.g., planetary boundaries or local ecological limits).