[CSRD] E2-2: Actions and resources related to pollution

CSRD Simplified: Disclosure Requirement E2-2: Actions and resources related to pollution

1. Introduction

If policies (E2-1) are the rules of the road, then actions are the actual driving. ESRS E2-2 asks undertakings to move beyond high-level commitments and disclose the concrete steps they are taking to tackle pollution.

This disclosure is important for credibility. It proves that a company is investing real effort and capital into managing its environmental impact. It connects the policies defined in E2-1 to the measurable results reported in E2-3 (Targets) and E2-4 (Metrics).

I will briefly explain the requirements for disclosing pollution-related actions and the resources allocated to them.

More elaborate articles are, or will become available, which can be found on: Sustainability Simplified.

2. What are pollution actions?

Pollution actions are the specific initiatives, projects, or changes in business practices implemented to manage material pollution impacts, risks, and opportunities.

According to ESRS 2 (AR 38), environmental actions should ideally be classified according to the mitigation hierarchy:

Avoidance: Preventing the pollution from happening (e.g., phasing out a Substance of Very High Concern).

Minimization: Reducing the amount or intensity of pollution (e.g., installing air scrubbers or wastewater treatment plants).

Restoration: Remediating damage already done (e.g., cleaning up a contaminated soil site).

Compensation: Offsetting residual impacts (though this is less common for pollution than for biodiversity).

Typical examples include:

Technology upgrades: Retrofitting factories with best available techniques (BAT) to reduce air emissions.

Process changes: Reformulating products to eliminate microplastics or hazardous chemicals.

Value chain engagement: Working with suppliers to reduce their water pollutant discharges.

Remediation: Projects to decontaminate soil after an accidental spill.

The ESRS defines actions as follows:

“Actions refer to:

i. actions and action plans (including transition plans) that are undertaken to ensure that the undertaking delivers against targets set and through which the undertaking seeks to address material impacts, risks and opportunities; and

ii. decisions to support these with financial, human or technological resources.

Actions can be individual actions, taken only by the undertaking, or collective actions, this is, collaborative efforts by a group of stakeholders - such as undertakings, governments, civil society, or communities - to address shared challenges or achieve common goals, particularly when those goals cannot be effectively achieved by any single actor working alone.”

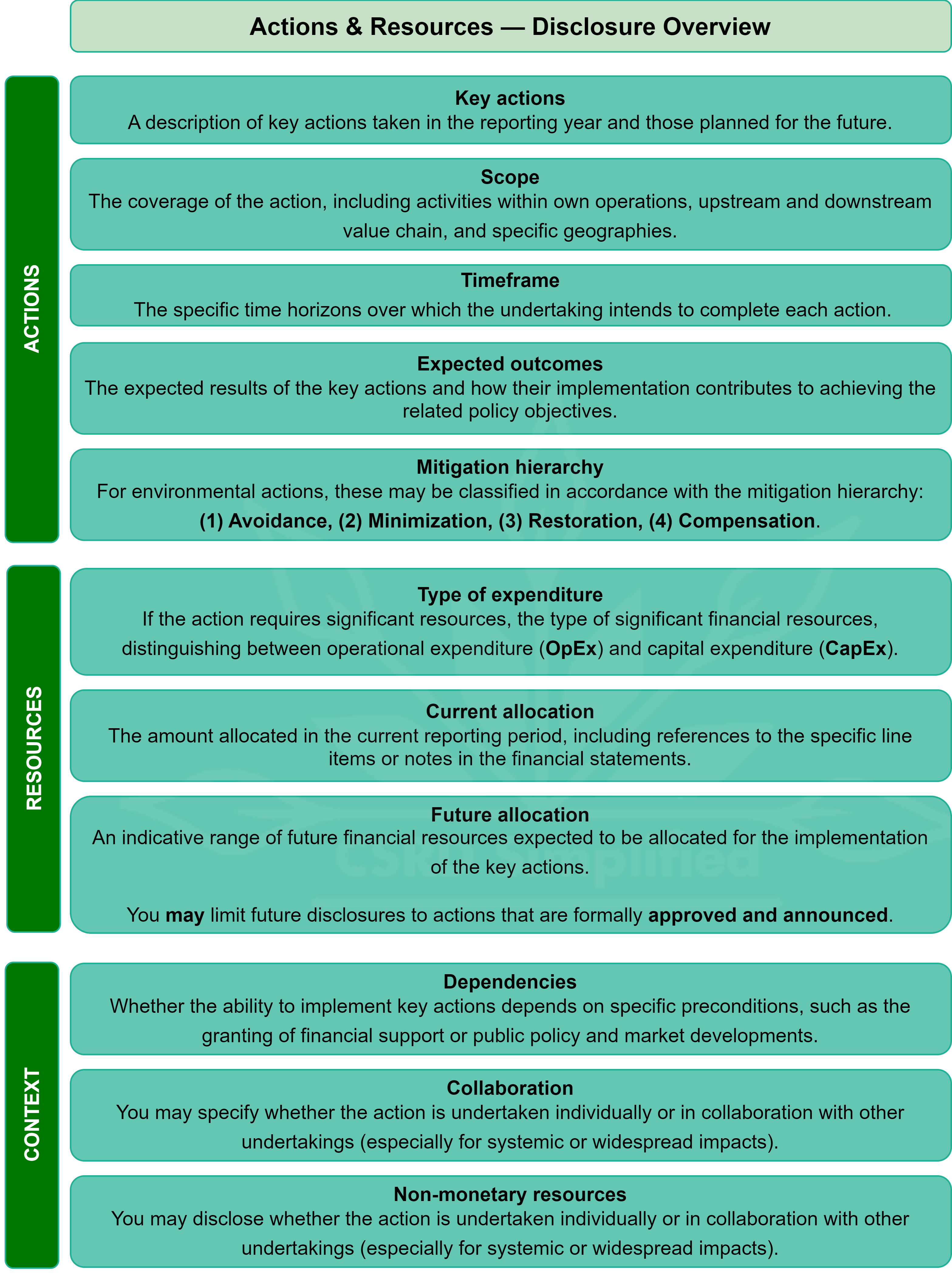

3. ESRS E2-2 at a glance

E2-2 requires that “the undertaking shall disclose its key pollution-related actions and resources allocated to the implementation of those actions in accordance with the provisions of ESRS 2 GDR-A“.

To comply with ESRS 2 GDR-A, the disclosure must include:

4. How E2-2 links to the rest of ESRS E2

The Action disclosure is the bridge between policy and performance:

E2-1 (Policy): You commit to “Zero Pollution.”

E2-2 (Action): You invest €2M in a new water filtration system (CapEx) and €100k/year in maintenance (OpEx) to achieve this.

E2-3 (Target): You aim to reduce water pollutants by 50% by 2030.

E2-4 (Metric): You report the actual tonnes of pollutants discharged this year to verify if the action is working.

The disclosure of actions and resources provides the evidence that the company is mobilizing to meet its goals.

5. Bottom line

E2-2 is where you demonstrate execution. To report effectively:

Be specific: Avoid vague statements like “we are working on it.” State what you are building, changing, or fixing.

Show the money: Investors review the resources section to ensure your budget aligns with your ambitions. If you have a massive target but zero budget allocated, it raises red flags.

Use the hierarchy: Frame your actions around avoidance and minimization first, as these are more effective than remediation.

Link to value chain: Don’t forget actions taken to address pollution upstream (suppliers) or downstream (product use).