[BREAKDOWN] E1-7: Understanding the corporate energy mix

E1-7: Understanding the corporate energy mix

Last updated: 17-09-2025

1. Introduction

Energy has moved from a background operational cost to a central strategic issue for companies. Rising energy prices, climate regulations, and investor demands are prompting businesses to reassess their energy sourcing and consumption strategies. Companies that fail to act risk exposure to transition costs, reputational damage, and stranded assets.

The concept of an ideal energy mix offers a roadmap for balancing sustainability with financial performance. It means combining different energy sources and financing mechanisms in ways that reduce emissions, stabilize costs, and protect against regulatory and market volatility.

In this article, you will read about:

✅ Energy mix as a corporate strategy

✅ What short-term (2030) and long-term (2050) scenarios mean for corporate strategy

✅ Why carbon pricing, policy incentives, and early action shift the economics of energy strategies

2. Energy mix as a corporate strategy

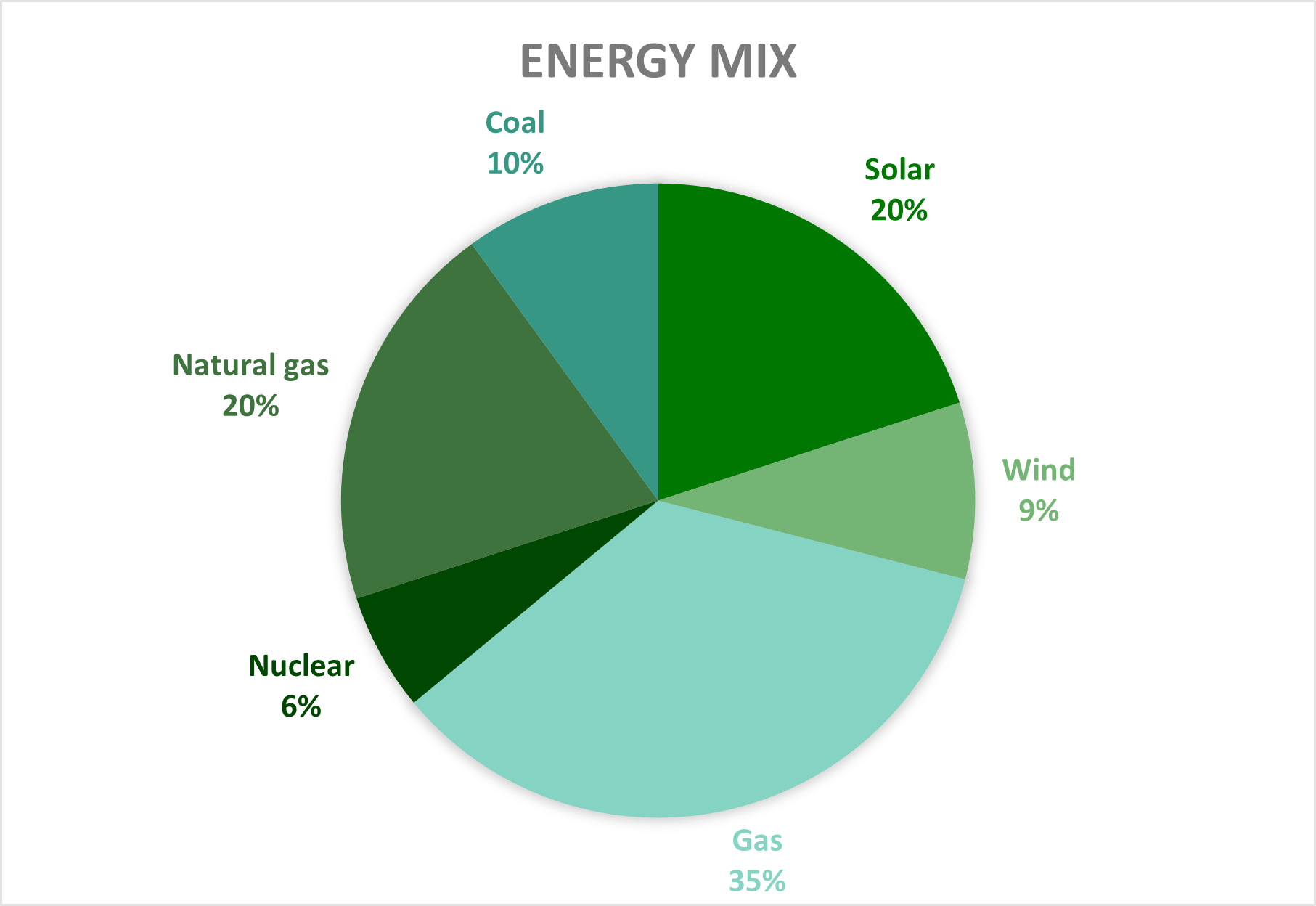

The energy mix refers to the share of electricity and heat a company sources from various technologies such as solar, wind, hydro, natural gas, nuclear, or hydrogen. What makes the concept strategic is its direct link to emissions, cost structures, and resilience.

Profitability: Renewable energy sources like wind and solar now provide some of the lowest-cost electricity globally. However, their intermittency requires companies to balance them with storage or complementary baseload supply .

Sustainability: Reducing dependence on fossil fuels cuts Scope 2 emissions (from purchased electricity) and aligns with net-zero targets.

Risk management: A diversified energy mix reduces vulnerability to price shocks and regulatory changes, particularly carbon pricing.

Thus, the “ideal” mix is not fixed but depends on corporate profile, geography, and time horizon.

You can usually find your company’s energy mix from two sources:

Supplier level: Your electricity supplier is required (in most regions) to publish an annual “fuel mix disclosure” or “energy label” showing what percentage of their electricity comes from renewables, nuclear, gas, coal, etc. This is often available on their website, in customer portals, or on your electricity bill.

National level: Governments and energy regulators regularly publish the national electricity mix, often through energy agencies (e.g., the U.S. EIA, UK BEIS, EU Eurostat). These figures show the overall grid mix.

3. 2030: Renewables reshape corporate energy

According to the IEA’s Renewables 2024 report, the world will add more than 5,500 GW of renewable capacity by 2030—equal to the current power capacity of China, the EU, India, and the United States combined. By then, renewables are expected to cover nearly half of global electricity demand.

Solar will lead this surge, accounting for 80% of new capacity, while wind is set to double its recent growth rate. Together, they are forecast to supply 30% of global electricity generation by 2030, twice today’s share.

For companies, these developments carry several strategic implications:

Prioritize solar procurement: Solar is now the cheapest option for new power plants in almost every country, making it the anchor of corporate decarbonization strategies.

Expand wind sourcing where viable: Onshore and offshore wind can provide balance to solar-heavy mixes, especially in regions with high wind potential.

Invest in flexibility and storage: Curtailment rates for renewables are already rising to around 10% in some countries. Firms should explore battery storage, demand-side management, and flexible PPAs to ensure reliable supply.

Prepare for policy-driven acceleration: Nearly 70 countries are expected to meet or exceed their current renewable ambitions by 2030, but achieving the COP28 target of tripling global capacity will require governments to further streamline permitting, expand grids, and reduce financing barriers in emerging markets.

Complementary natural gas use: While gas is a fossil fuel, its lower carbon intensity and ability to provide flexible generation make it a transitional option in certain regions.

4. 2050: Net-zero energy systems

By 2050, energy systems are expected to be deeply decarbonized, in line with global net-zero commitments. For companies, this means that energy strategies must evolve well beyond incremental efficiency measures and reflect the following structural shifts:

Dominance of renewables: Solar, wind, and hydro are projected to supply the vast majority of electricity generation. The IEA’s Net Zero by 2050 scenario shows renewables accounting for around 90% of global power by mid-century, making them the backbone of corporate electricity sourcing.

Storage and hydrogen integration: As the share of variable renewables rises, battery storage, demand-side flexibility, and green hydrogen will be critical for balancing supply and ensuring system reliability. Companies in heavy industry, transport, and chemicals will increasingly depend on hydrogen and synthetic fuels for processes that cannot be easily electrified.

Decline of unabated fossil fuels: Even natural gas, once a “transition fuel,” will need to be phased out or paired with carbon capture and storage (CCS). IPCC AR6 highlights that continued fossil use is only compatible with net zero if combined with large-scale abatement.

Emerging baseload options: Technologies such as small modular nuclear reactors (SMRs), advanced geothermal, and bioenergy with carbon capture and storage (BECCS) may provide firm, low-carbon generation to complement variable renewables. While not yet widely deployed, they are expected to play a role in regional or sector-specific mixes.

By 2050, the “ideal” energy mix will be almost entirely low-carbon, built around renewables and supported by storage, hydrogen, and next-generation baseload technologies.

5. Key strategic takeaways

Designing an energy mix requires evidence on what strategies actually pay off under different conditions. Recent studies and reports provide valuable lessons: