[BREAKDOWN] E1-10: How does internal carbon pricing work?

ESRS E1-10: How does internal carbon pricing work and when to use it?

Last updated: 21-08-2025

1. Introduction

Internal carbon pricing (ICP) converts an organization’s emissions into a financial signal that can steer investments, budgets, and behaviors toward a low-carbon trajectory. By assigning a monetary value to each ton of CO₂ (or CO₂-equivalent), companies turn climate risk into a line item that leaders can manage.

At its core, ICP is a voluntary corporate mechanism that helps firms anticipate policy, align with climate targets, and fund decarbonization. It increasingly features in disclosure frameworks: ISSB/IFRS S2 asks companies to disclose if and how they use an internal carbon price; the EU’s CSRD and TCFD encourage transparent treatment of carbon-related risks and pricing assumptions.

By reading this piece, you will learn:

✅ The four main models of internal carbon pricing, how they work, and when to use them

✅ Why ICP matters now: regulation readiness, climate targets, risk management, and innovation

✅ A step-by-step playbook for implementation

✅ Typical pitfalls and how to avoid them

✅ Real-world case snapshots from Microsoft, Mahindra, BHP, Swiss Re, and others

You’ll come away with a better understanding of ICP, what it is, why it works, and how to design a version that influences decisions.

2. What internal carbon pricing is

Internal carbon pricing assigns a monetary value (e.g., $/tCO₂e) to company emissions so that carbon shows up in investment cases, operating budgets, product decisions, and supply-chain choices. Companies apply four main models:

A hypothetical carbon cost (e.g., $40–$80 per ton of CO₂e) applied in financial models. No money changes hands. It is mainly used to “future-proof” projects by testing how they would perform if external carbon prices rise. This approach is particularly relevant for long-lived investments (factories, infrastructure, or energy assets) and for portfolio strategy decisions.

A real financial mechanism. Business units pay a fee for each ton of emissions they generate. The collected funds go into a central pool, which finances decarbonization projects such as efficiency upgrades, renewable energy, or removals. This makes carbon a visible line in budgets and creates a direct incentive to reduce emissions, since lower emissions mean lower costs.

A backward-looking calculation of how much the company has effectively spent on emission reductions in the past. It is computed as the total spend on abatement projects or offsets divided by the tons of emissions avoided or offset. While not a tool for forward planning, it provides useful insight into actual costs of decarbonization and helps benchmark against future pricing strategies.

An intra-company trading system. Units or divisions receive emission allowances under an internal cap. If one unit reduces more than required, it can sell its surplus allowances to another. This creates a mini carbon market inside the company, encouraging reductions where they are cheapest. While powerful, this model is complex to design and administer, and therefore less commonly used.

Why companies blend approaches

Many organizations use two tools side by side: a shadow price for long-term planning and a carbon fee for daily operations.

Together, the two tools create a dual system:

The shadow price shapes strategic decisions about where to invest for long-term resilience.

The internal fee drives operational discipline and ensures money is available to actually finance decarbonization.

3. Why you should use internal carbon pricing now

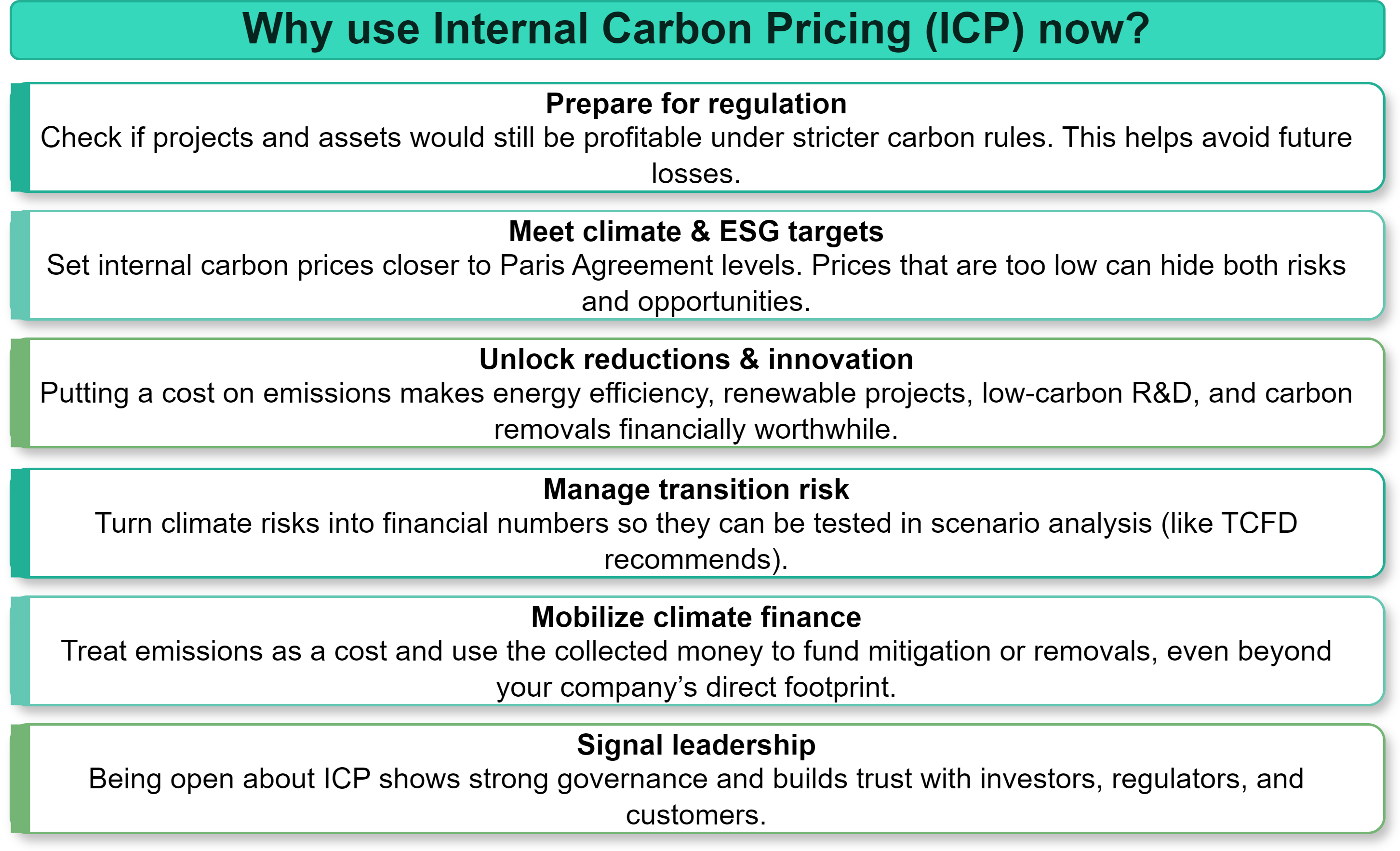

Prepare for regulation

By using an internal carbon price, companies can test whether their assets and projects would remain profitable under stricter rules and avoid locking themselves into stranded assets.

Meet climate and ESG targets

Many companies are experimenting with internal carbon pricing, but the values they set often fall below Paris-aligned levels. Research suggests that prices of $40–$80 per ton by 2020 and $50–$100 per ton by 2030 are needed to align with the Paris Agreement. In practice, most firms use much lower thresholds or none at all, meaning their current internal prices may underestimate future risks and opportunities. Recalibrating these values can close the gap between corporate ambition and climate goals.

Unlock reductions and innovation

When emissions carry a cost, more projects suddenly become financially viable. Internal fees also generate funds that can be reinvested in energy efficiency, renewable power, low-carbon R&D, or removals.

Manage transition risk

Carbon pricing translates climate risk into clear monetary terms, which finance teams can model and incorporate into scenario analysis. This strengthens resilience and aligns with frameworks like TCFD.

Mobilize climate finance

The world faces a large funding gap for mitigation. Internal carbon pricing allows companies to assign a value to their emissions and channel equivalent funds into projects such as removals, going beyond their own footprint.

Signal leadership to stakeholders

Using and disclosing an internal carbon price shows strong governance and transparency. It signals to investors, regulators, and customers that the company takes climate seriously and has integrated it into financial performance.

4. Make it change decisions: integration into business

Internal carbon pricing has the most impact when it is fully embedded in core business processes:

Capital planning and M&A – Use a shadow price in investment models (NPV/IRR) so projects are tested against future carbon costs. This steers capital toward assets that remain profitable in a low-carbon economy.

Budgeting and forecasting – Apply the carbon fee like a cost line in each unit’s budget. Business areas that cut emissions keep more funds for other priorities, creating a built-in incentive.

Product design and R&D – Include carbon costs in product P&Ls. High-emission designs become less attractive, while efficient or low-carbon innovations gain a financial edge.

Procurement and suppliers – Add carbon costs into tender processes and vendor scorecards. This pressures suppliers to lower emissions and strengthens decarbonization across the value chain.

Risk and scenarios – Stress-test strategies against higher carbon prices (e.g., $100/t by 2030). This helps companies adjust early instead of reacting late to regulation or market shifts.

Incentives and KPIs – Link bonuses, performance metrics, or unit targets to carbon-adjusted results. This ties leadership and team success directly to emissions performance.

Culture and change management – Make carbon a visible part of everyday decisions. Training, clear communication, and executive backing are crucial, since changing behaviors is often harder than setting the price itself.

5. Implementation playbook (10 steps)

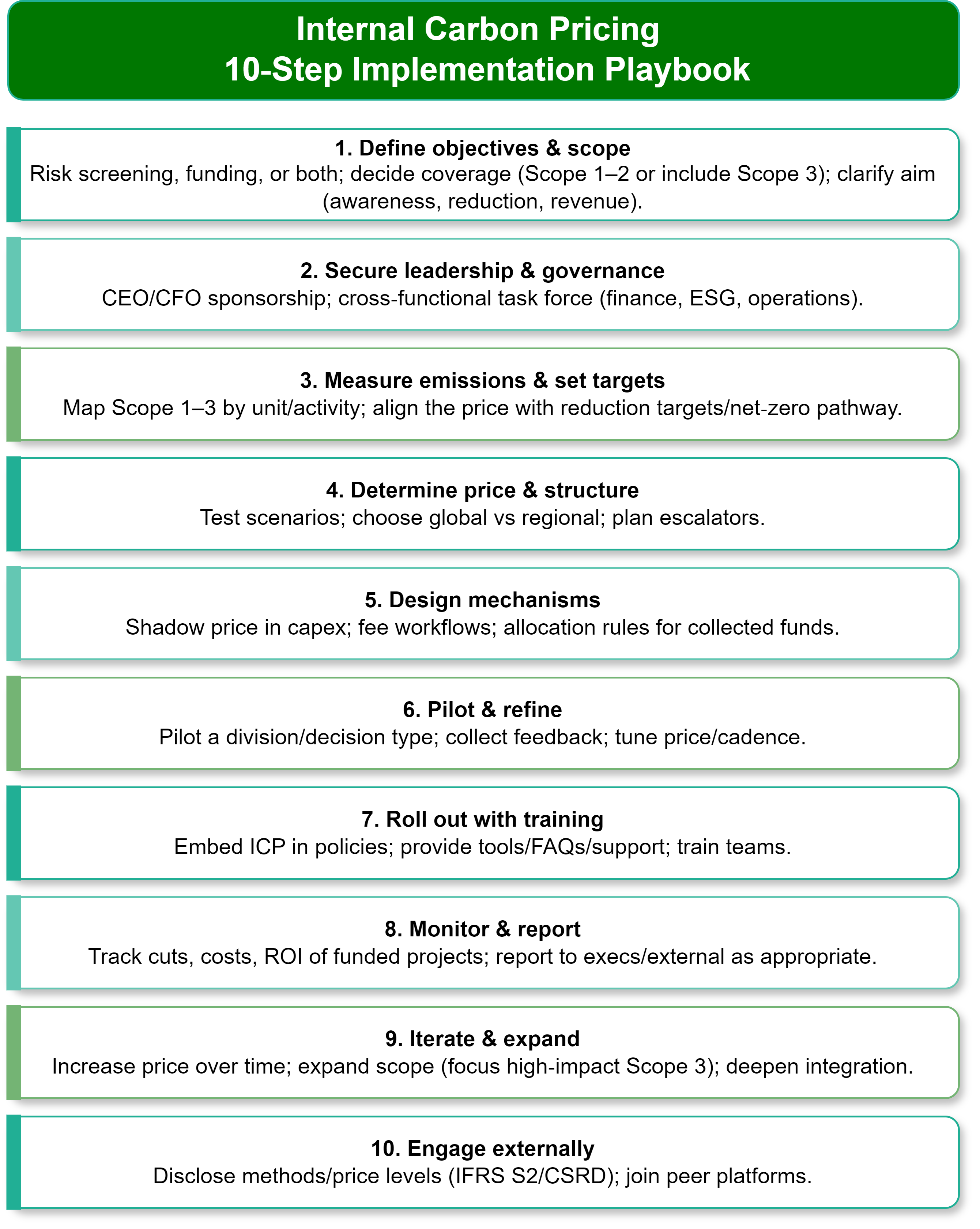

Define objectives and scope

Start by clarifying what you want ICP to achieve: is it mainly a risk screening tool (to test investments against future carbon costs), a funding mechanism (to generate money for decarbonization projects), or both? Decide which parts of the business to cover first.Decide whether to apply ICP only to company operations (Scopes 1–2) or also to supply chain and product use (Scope 3).

Define whether the goal is cost awareness, emissions reduction, or revenue for green projects.

Secure leadership and governance

Strong leadership support is critical. ICP needs champions at the top and clear governance structures to avoid being sidelined.Get CEO/CFO sponsorship to give the program credibility.

Create a cross-functional task force with finance, ESG, and operations to design and manage ICP.

Measure emissions and set targets

ICP is only as strong as the emissions data behind it. Establish a reliable baseline to calibrate your price ambition.Map emissions by unit and activity (Scope 1 = direct fuel use, Scope 2 = purchased electricity, Scope 3 = value chain).

Align the internal price with your reduction targets or net-zero pathway.

Determine price and structure

Choose the right carbon price level and how it will be applied.Test different scenarios (e.g., moderate vs. high future policy costs).

Decide between a single global price or regional variations.

Plan escalators (scheduled increases) so the price rises over time.

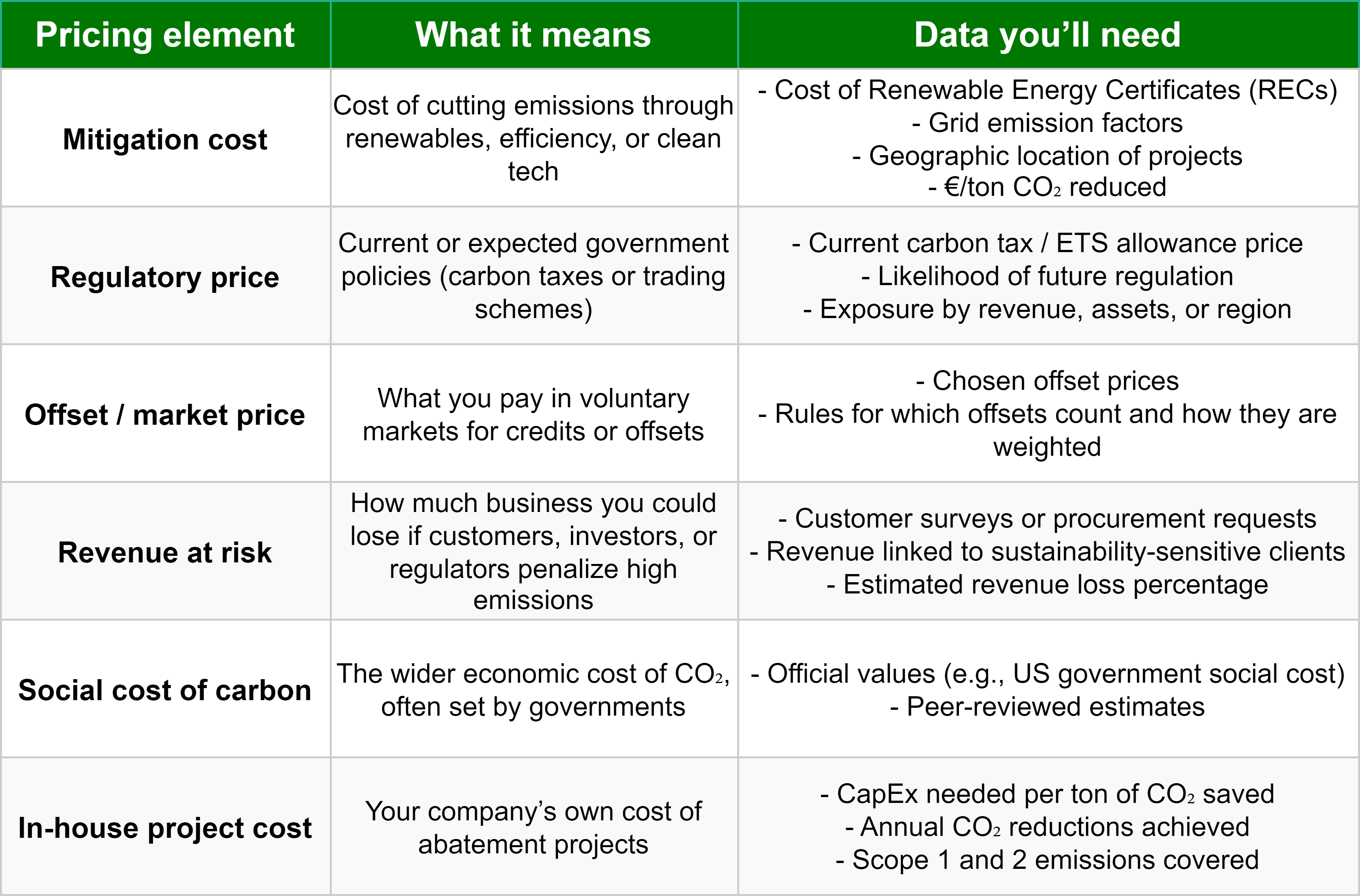

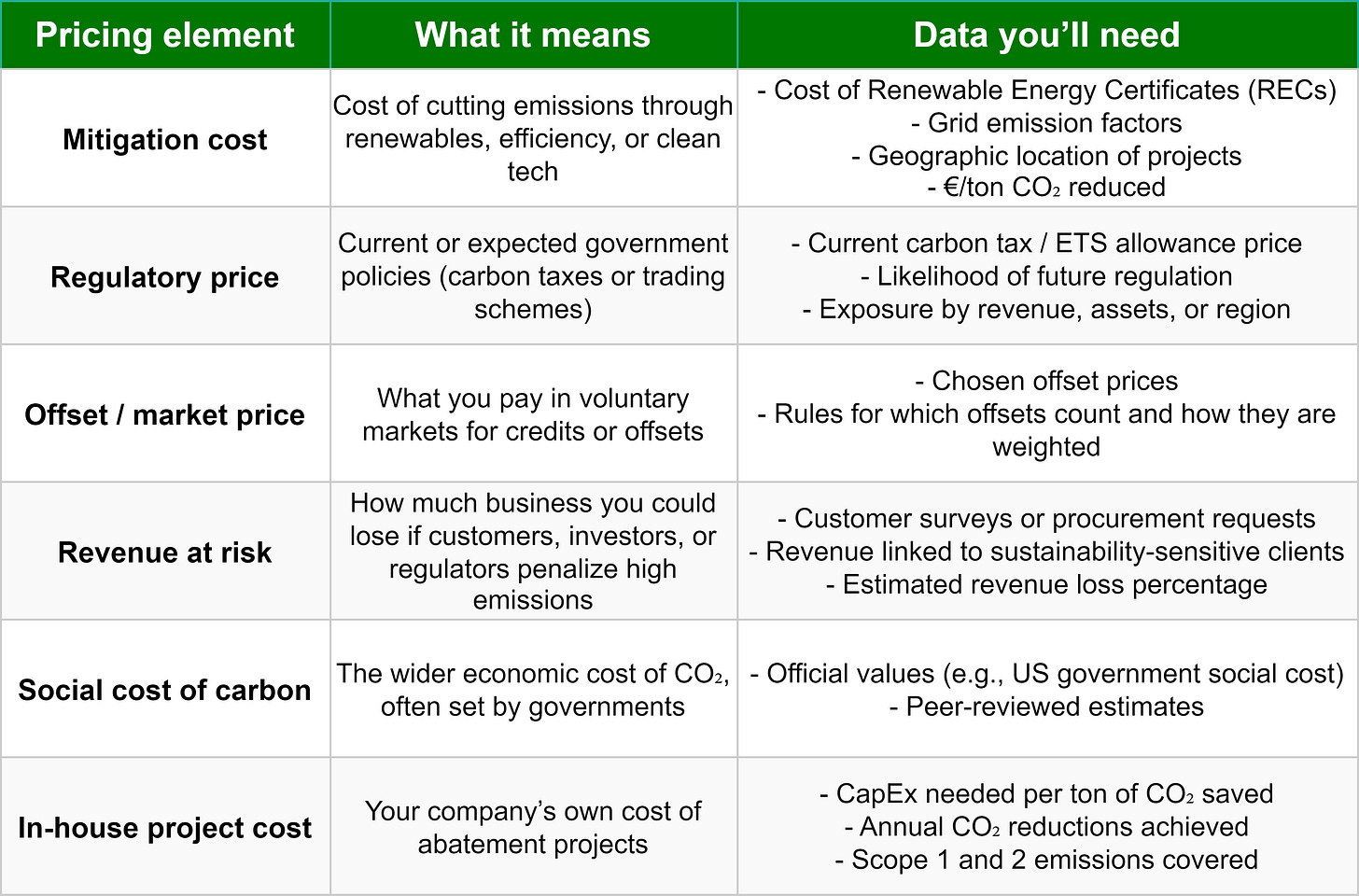

When setting an internal price, link it to credible references instead of picking a number at random. Common anchors include:

Design mechanisms

Decide how ICP will be built into day-to-day business processes.Add a shadow price (a hypothetical $/t added in financial models) to capital expenditure templates.